| Latest Forum Topics / Wheelock Prop |

|

|

More than 75% controlled by hongkong

|

|||||

|

alexchew

Master |

27-Feb-2018 18:56

|

||||

|

x 0

x 0 Alert Admin |

time for WL to comeback tomorrow.. excellent results and super cash cow... the potential with HPL not taken into account yet. downside, divdends still stingy..

|

||||

| Useful To Me Not Useful To Me | |||||

|

n3wbie

Elite |

28-Nov-2017 17:15

|

||||

|

x 0

x 0 Alert Admin |

anyone else followed this? noticed that volume yesterday and today are almost double that of average. at the HK side, believe that Wharf has previously announced plans to spin off and create a REIT with the commercial assets. potential for this to be included with its two crown jewel assets in SG? | ||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

lifeisgood

Supreme |

06-Oct-2017 12:27

|

||||

|

x 0

x 0 Alert Admin |

Over the last few year (starting from like 6+ years ago), this company did not have a CEO. Ex CEO died in 2012. Ever since , the company was managed by the Board of Directors. Needless to say, BOD always looked at balance sheet, instead of day to day running of the business. The company then promptly wrote off value of the China Fuyang city project, as well as the Ang Mo Kio Panorama. As those projects turned out to be very profitable, it is high time the BOD wrote back values of those 2 projects (plus others as well). (I suspect why they wrote off the value is also to reduce the NAV of the share, to facilitate a cheaper takeout by the major shareholders). The excuse used is always " PRUDENCE" . |

||||

| Useful To Me Not Useful To Me | |||||

|

lifeisgood

Supreme |

06-Oct-2017 11:04

|

||||

|

x 0

x 0 Alert Admin |

Recently Mandarin Oriental tried to sell the Excelsior Hotel in HK Causeway Bay for between USD 3.1 to USD 3.8 billion, and the share price of Mandarin Oriental went through the roof. Lets see if Wheelock can pull off something like that for say, the Wheelock Place, which is also multi billiond dollars, judging from the valuation of ION Orchard across the street. |

||||

| Useful To Me Not Useful To Me | |||||

|

lifeisgood

Supreme |

06-Oct-2017 10:34

|

||||

|

x 0

x 0 Alert Admin |

Today the shortsellers from Kin Eng at 915 probably kena toasted, I bought some from KE today.

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

lifeisgood

Supreme |

06-Oct-2017 10:27

|

||||

|

x 0

x 0 Alert Admin |

For the past SEVEN (7) years, chng kays controlled the price around and below the $2.00 level. Lets see this round whether it can succeed to break through or not. Power !!!

|

||||

| Useful To Me Not Useful To Me | |||||

|

lifeisgood

Supreme |

06-Oct-2017 10:16

|

||||

|

x 0

x 0 Alert Admin |

JP Morgan and Morgan Stanley for the past many days have been doing controlled suppression/accumulation of the shares, I guess it is for accumulation and preventing price for surging too fast, as I expect a privatisation offer is in the works. |

||||

| Useful To Me Not Useful To Me | |||||

|

lifeisgood

Supreme |

06-Oct-2017 10:13

|

||||

|

x 0

x 0 Alert Admin |

This one on the verge of bursting up !

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

paul1688

Veteran |

18-Sep-2017 15:00

|

||||

|

x 0

x 0 Alert Admin |

UOBKH Update Comments We foresee the nascent recovery spreading to the mid-range and high-end segments in the next wave, driven by replacement demand from enblocers and a pick-up homebuying interest from foreigners. We expect Singapore property prices to rise by 5-10% next year after bottoming out this year. Our top picks are Wing Tai, GuocoLand and Wheelock. WHAT&rsquo S NEW Enbloc fever is picking up, and we believe we are still in the early cycle of the recovery. Historically, spikes in enbloc sales have preceded property sector price recovery in the past cycles in 2007 and 2011. The levelling of taxation costs and cooling measures are also building up the relative appeal of Singapore real estate to foreign buyers. ACTION Maintain OVERWEIGHT. We foresee the nascent recovery spreading to the mid-high end segment in the next wave, driven by replacement demand from enblocers and a pick-up in foreign homebuying interest from foreigners. We expect Singapore property prices to rise by 5-10% next year after bottoming out this year (12-15% correction from peak). Our top picks are Wing Tai, GuocoLand, and Wheelock. Disclaimer : Just sharing. DYODD. Not a suggestion to Buy or Act.

|

||||

| Useful To Me Not Useful To Me | |||||

|

n3wbie

Elite |

06-Sep-2017 09:03

|

||||

|

x 0

x 0 Alert Admin |

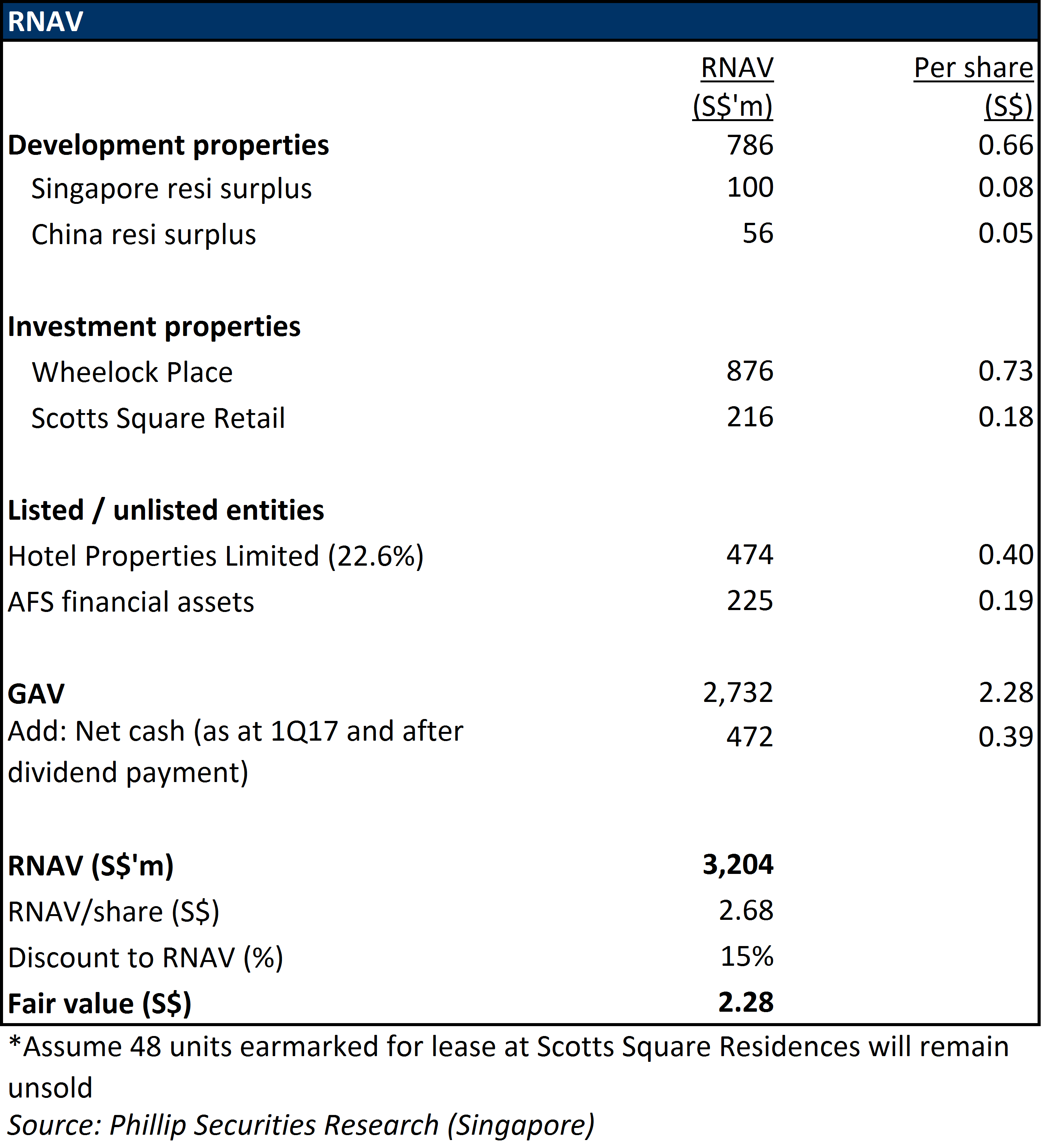

UOB initiated with TP of $2.33. Wheelock Properties (WP SP) Ready To Pounce We see good value in Wheelock that is trading at a deep 33% discount to its RNAV of S$2.74, despite its net cash position with S$448m in the coffers and no outstanding debt. It is a key beneficiary of the property sector turnaround and rotational interest, deriving over 80% of its value from Singapore. It offers a stable dividend yield of 3.3% supported by a strong recurring income stream from its investment properties. Resume coverage with a BUY and a target price of S$2.33. Deployment of S$2b in acquisition headroom will be a key re-rating catalyst. WHAT&rsquo S NEW We met up with Wheelock Properties&rsquo (Wheelock) management recently to get an update on its projects. Wheelock&rsquo s ytd share price performance (+24.7% ytd) lags its peers&rsquo (+27.6%) and is significantly behind that of City Developments (+41.4%). We see good value in Wheelock that is trading at a deep 33% discount to its RNAV of S$2.74, despite S$447.7m in cash coffers and no outstanding debt. STOCK IMPACT Deployment of S$2b in acquisition headroom. Wheelock is the only developer in a net cash position within our coverage with S$447.7m in cash coffers and no outstanding debt. This positions it well to deploy its sizeable acquisition headroom of S$2b (assuming comfortable net gearing level of 50%). Management noted that the stiff competition for sites has made it tough for acquisitions but they are on active lookout. Their focus remains on the high-end segment and a likely acquisition may come from an en bloc sale. Stable dividend yield supported by recurring income. We estimate that Wheelock Place and Scotts Square contribute over S$40m in pre-tax earnings annually for Wheelock, providing a stable recurring income stream from investment properties. We forecast a healthy 3.3% dividend yield, underpinned by its investment properties (accounting for 40-50% of its earnings). Beneficiary of property sector turnaround and rotational interest. Wheelock is well positioned to ride the property upturn as it derives over 80% of its value from Singapore. It is also a beneficiary of the expected privatisation of Global Logistics Properties which has led to strong interest from fund managers in developer names as it could replace the gap in their portfolios. |

||||

| Useful To Me Not Useful To Me | |||||

|

n3wbie

Elite |

05-Sep-2017 09:00

|

||||

|

x 0

x 0 Alert Admin |

fundamentally sound company with strong balance sheet - only developer and property manager with 0 borrowings and more than $400m cash. good analysis from phillip' s research report. also trading at just 0.7x pb. in addition, they will be added to FTSE ST Large and Mid Cap indices as of closing next Friday, could we perhaps see some buying/accumulation from funds to have this stock included in their portfolio? |

||||

| Useful To Me Not Useful To Me | |||||

|

AttasBoss

Elite |

28-Jul-2017 09:13

|

||||

|

x 0

x 0 Alert Admin |

https://www.stocksbnb.com/reports/wheelock-properties-singapore-prime-privatisation-candidate/

Wheelock Properties Singapore &ndash Prime privatisation candidateJune 2, 2017Recommendation: TRADING BUY // Target Price: S$2.28

Privatisation thesis is still valid but what&rsquo s different this time round?

Our rationale for a privatisation is based on

Potential upside even without a privatisation

Investment Action Given its valuation of 0.7x PB and a recent rally in share price, WPSG is still undervalued compared to its peers (0.9x PB). The current valuation also prices the Group&rsquo s S$1.1 billion of investment properties (Wheelock Place and Scotts Square) for free. With multiple catalysts that involve revenue recognition from development properties in the next 12 months and possibly a privatisation, the current valuation is undeservedly cheap. We have initiate with a Trading Buy and a target price of S$2.28 based on our full-year FY17 RNAV estimates. Company Background Wheelock Properties (Singapore) (WPSG), formerly known as Marco Polo Developments Limited, was listed on SGX-ST in 1981. The Group&rsquo s principal activities are property investment and property development with a focus on luxury developments. WPSG is a 76.2% subsidiary of Wheelock and Company (BB code: 20 HK).

Case for privatisation remains unchanged

We opine that Wheelock and Co could adopt a similar move for WPSG as shares of WPSG are thinly traded and has been trading at a significant discount to its NAV (40%). Additionally, the Group has not sought for funds from the equity market for more than 11 years since 2006.

Our rationale for a privatisation is based on:

Potential upside even without a privatisation

Valuations

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Lepin888

Veteran |

21-Jan-2017 10:46

|

||||

|

x 0

x 0 Alert Admin |

Parent... | ||||

| Useful To Me Not Useful To Me | |||||