Post Reply

1-20 of 385

Post Reply

1-20 of 385

oil price is collapsing!tangsookiam1947 ( Date: 30-May-2026 13:57) Posted:

| will Bumitama drop back below $1? better run now? |

|

will Bumitama drop back below $1? better run now?

RHB upgrades Bumitama Agri to ' neutral' after 15% share price retreat

RHB Bank Singapore has upgraded Bumitama Agri from " sell" to " neutral" with an unchanged target price of $1.70, implying a downside of 6.6% to its share price of $1.82 as at its report dated May 13. Shares in the agri company had retreated 15% over the past two weeks. The bank' s FY2026 dividend yield estimate of 5.6% is seen providing support at current levels, says the Singapore research team.

On May 12, Bumitama reported a core profit of IDR755 billion ($54.9 billion) for the 1QFY2026 ended March 31, down 26% q-o-q but 42.4% up y-o-y, making up 21%&ndash 24% of RHB' s and consensus full-year estimates and broadly within RHB&rsquo s expectations. The quarter is typically the weakest in terms of seasonal output, notes the RHB team.

Nucleus fresh fruit bunches (FFB) output rose 8.2% y-o-y in 1QFY2026, above both RHB' s 3% projection and management' s own full-year guidance of 0%&ndash 5%. The report notes that while Bumitama expects FFB growth to pick up in the second quarter and peak in the third, management is keeping its full-year guidance unchanged (at 0%&ndash 5%) given an anticipated moderation in 4QFY2026. Crude palm oil (CPO) sales volume jumped 25% y-o-y on inventory drawdowns. RHB maintains its 2%&ndash 4% FFB growth forecast for FY2026&ndash FY2027.

On costs, the report points out that management now guides for unit costs to rise approximately 10% y-o-y in FY2026, up from its previous guidance of 5%&ndash 10%, &ldquo on the back of higher fertiliser and logistics costs&rdquo . Bumitama has already tendered for almost 100% of its FY2026 fertiliser requirements at prices 6%&ndash 7% higher y-o-y. RHB thus makes no changes to its own cost assumptions, having already pencilled in a 10% rise.

Bumitama also raised its dividend payout range to 60%&ndash 75% from 40%&ndash 60%, in line with its 75% payout in FY2025. RHB has lifted its payout assumption to 65%&ndash 70% from 60%&ndash 65% accordingly.

At 12 times its FY2026 P/E, which is the highest end of its peer range of 7 times &ndash 12 times and well above its historical average of 6 times, the report considers &ldquo valuations are fairer now&rdquo following the recent correction. The target price is based on 12 times Bumitama&rsquo s FY2026 P/E with a 10% ESG discount.

Shares in Bumitama Agri closed 5 cents higher or 2.67% up at $1.95 on May 14.

Wow 😳 ATH!

Bumitama Agri net positive on oil hikes as palm oil prices move in tandem with crude

Palm oil is a key feedstock in biofuel, whose demand tends to rise when crude oil prices surge

[SINGAPORE] Rising energy prices as a result of the Iran war are unlikely to negatively affect palm oil producer Bumitama Agri : P8Z 0% and could even provide an overall boost to its business, it said, even as it noted cost pressures.

The Indonesia-focused company published its response to a shareholder in a regulatory filing on Wednesday (Apr 22), stating that fuel and fertiliser costs have historically accounted for about 10 per cent of total production costs on average.

Palm oil prices tend to be positively correlated with energy prices, said Bumitama Agri, noting that it is also a key feedstock in biofuel production. Higher fossil fuel prices usually &ldquo support increased biodiesel production volume&rdquo , particularly for major producers such as Indonesia and the US.

That and higher structural demand over time from the energy sector could also &ndash in certain scenarios &ndash be &ldquo net supportive&rdquo to the mainboard-listed company&rsquo s performance. About 25 per cent of global palm oil production in 2025 was intended for energy-related uses, up from 15 per cent a decade ago, added Bumitama Agri.

In response to questions from the Securities Investors Association (Singapore), the company said it does not actively hedge using financial derivatives such as commodity futures. Instead, it prefers to manage the pricing risk through a &ldquo disciplined and selective forward sales strategy&rdquo and relies on physical forward contracts &ldquo where appropriate&rdquo .

Forward sales are capped at a maximum of 40 per cent of nucleus crude palm oil production and for a maximum of six months, added Bumitama Agri. Nucleus crude palm oil refers to crude palm oil produced from plantations directly owned, managed and operated by a palm oil company like Bumitama Agri itself.

This &ldquo balanced&rdquo approach provides a certain level of price visibility &ldquo while retaining sufficient exposure to spot market movements&rdquo , the company said. It noted that in 2025, it refrained from signing forward contracts as forward pricing was not deemed &ldquo sufficiently attractive&rdquo compared to spot prices.

This allows Bumitama Agri to &ldquo remain disciplined and opportunistic, balancing downside protection with participation in favourable price environments&rdquo .

Shares of the company closed at S$1.93 on Tuesday, up 2.1 per cent or S$0.04.

If you put Iran first, it becomes an Iran-US war. And if the US cannot win, it literally means I-ran over US.

Mon, Bumitama, First Resource will start to cheong again after US-Iran war cease fire negotiation broke down

DBS raises target price for Bumitama Agri to $2.30

William Simadiputra of DBS Group Research has raised his target price for Bumitama Agri from $1.90 to $2.30, on expectations of better earnings this year from steady palm oil prices and a bigger production volume.

In his April 7 note, Simadiputra, who has kept his " buy" call, points out that crude palm oil prices gained 14% y-o-y in 2025 to US$1,000 per metric tonne, and he expects prices to remain at around US$950 this year.

Bumitama' s FY2025 earnings beat Simadiputra' s forecast and he expects the company' s bottom line to ease somewhat by 6.1% to 2.6 trillion rupiah this year.

" However, with limited export levies and taxes implemented so far, we see upside risk to our selling price and earnings forecasts," says Simadiputra.

" Earnings should trend higher in 2026, mainly on a decent palm oil price and higher output trend. Bumitama has been paying good dividends we see room to sustain said dividend and offer a decent yield of 5-6% to investors," he adds.

" If Bumitama pursues inorganic growth to expand its production volumes, it may become a key catalyst. As of now, Bumitama can maximise margins through cost efficiencies on its nucleus estates or by increasing mill utilisation to above 75% via external fruit purchases," he adds.

From his perspective, Bumitama' s share price, even having gained 40.74% year to date to $1.90 at close of April 6, might see further upside given the positive market outlook.

His revised target price of $2.30 is based on 20.4x FY2026 earnings - a valuation multiple that is above Bumitama' s historical PE level but is deemed justified due to " persistently high" crude palm oil prices and the company&rsquo s capability to maintain margin performance despite its reliance on external fruit purchases.

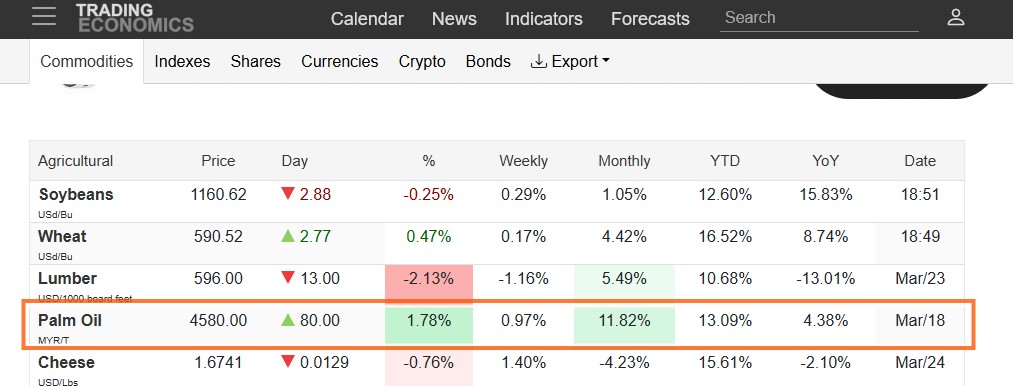

Palm oil price likely to rise to MRY 5,100 or another 6-8%/ The price is driven by strong export data, tightening supply expectations, and firm energy prices. Prices are expected to remain supported in the first half of 2026 due to Indonesia' s biofuel mandate, but could moderate in the second half.

Malaysian palm oil futures jumped about 1.5% to above MYR 4,800 per tonne, rebounding from earlier losses. Strength in Chicago soyoil and firmer crude oil prices, which improved biodiesel margins, underpinned the rally. Energy markets were supported after U.S. President Donald Trump, in a national address, pledged continued pressure on Iran&rsquo s energy sector without a clear timeline for resolution. On the demand side, cargo surveyors estimated that March palm oil exports surged between 44% and 57% from February, providing near-term support. However, gains were capped by a stronger ringgit and softer demand from top buyer India, with imports expected to ease to around 680,000 tonnes in March from 847,689 tonnes a month earlier. In Indonesia, the world&rsquo s largest producer, an industry association noted that biodiesel feedstock demand may reach 15 million tonnes this year, up 2 million tonnes, driven by the B50 rollout scheduled for July.

https://tradingeconomics.com/commodity/palm-oil

Last:1.86  +0.16

+0.16

very beautiful rallytrader1970 ( Date: 30-Mar-2026 09:04) Posted:

Otw to 200 as Palm oil is rising as alternate fuel to Oil... WATCH :)

ozone2002 ( Date: 27-Mar-2026 11:39) Posted:

Last:1.69 +0.1

great performance |

|

|

|

Otw to 200 as Palm oil is rising as alternate fuel to Oil... WATCH :)

ozone2002 ( Date: 27-Mar-2026 11:39) Posted:

Last:1.69 +0.1

great performance

ozone2002 ( Date: 19-Feb-2026 12:39) Posted:

Last:1.51 +0.04

not far from target 🎯 |

|

|

|

Last:1.69 +0.1

great performanceozone2002 ( Date: 19-Feb-2026 12:39) Posted:

Last:1.51 +0.04

not far from target 🎯

ozone2002 ( Date: 09-Feb-2026 12:22) Posted:

KGI Research

|

|

|

|

Shortists get squeezed and. It has cleared the resistance for more upsides

trader1970 ( Date: 27-Mar-2026 09:59) Posted:

Record profit i believe for the coming quarterly FY announcement.. BO 173 ll fly towards 180...

stockpicker ( Date: 16-Mar-2026 11:26) Posted:

Price breakout today. Waiting for volume and ADX to move up. Seen shortsellers shorting this stock regularly. Good luck to them

|

|

|

|

Record profit i believe for the coming quarterly FY announcement.. BO 173 ll fly towards 180...

stockpicker ( Date: 16-Mar-2026 11:26) Posted:

Price breakout today. Waiting for volume and ADX to move up. Seen shortsellers shorting this stock regularly. Good luck to them

|

|

A &ldquo hidden winner&rdquo of the Iran war

Bumitama Agri stands out as a

pure upstream levered play to rising crude palm oil (CPO) prices &mdash making it a structural beneficiary of geopolitical-driven energy shocks such as the ongoing Iran conflict.

It is a

&ldquo shining gem&rdquo because it sits at the intersection of:

- Energy crisis (oil-linked upside)

- Food security (inelastic demand)

- Policy support (Indonesia biodiesel mandates)

In a prolonged Iran conflict scenario, it is one of the

cleanest, highest-beta beneficiaries on SGX.

Palm oil price rising steadily

Price taking off... Did you buy?

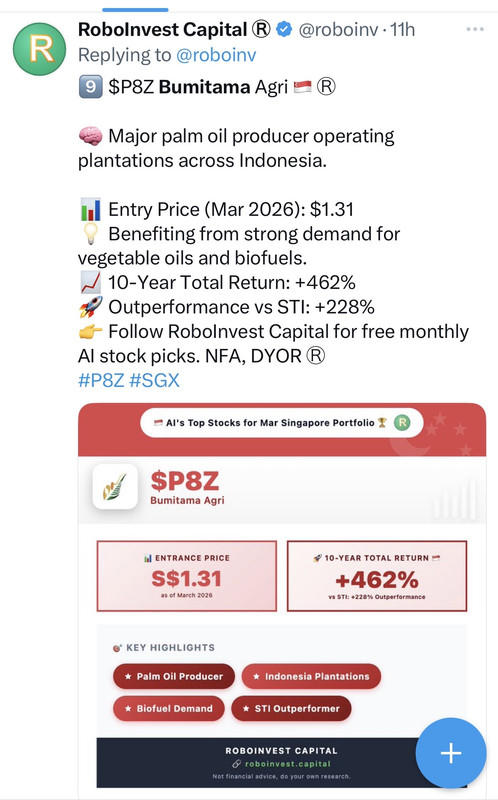

Roboinvest Capital pick Bumitama in their portfolio

Price breakout today. Waiting for volume and ADX to move up. Seen shortsellers shorting this stock regularly. Good luck to them

Palm oil is a leading, high-yield vegetable oil feedstock for biodiesel and hydrotreated vegetable oil (HVO) production, particularly in Indonesia and Malaysia. It is converted into biofuel via transesterification or refining. This is today' s bipfuel price