Post Reply

1-20 of 7131

Post Reply

1-20 of 7131

ComfortDelGro has not officially announced its Q2/1H 2026 results date on its investor calendar yet.

However, market data providers are currently indicating an expected earnings release

around 13 ~19 August 2026, with 13 August 2026 appearing on some financial calendar

price will be stagnant unless some catalyst events happen

JurongW ( Date: 01-Jun-2026 15:14) Posted:

Now a fight between the Bull and Bears for CDG

|

|

Now a fight between the Bull and Bears for CDG

drop towards 50 cents is a real possibility too?

Guzman ( Date: 30-May-2026 20:46) Posted:

The STI is breaking out. Banking shares are breaking all time highs. Even with 80% PATMI paid out as dividends, can cover for the share price drop.

Comfortdelgro and its management are pathetic. Results for coming quarters will be worst. Going below $1 is a real possibility. Bail out now, |

|

The STI is breaking out. Banking shares are breaking all time highs. Even with 80% PATMI paid out as dividends, can cover for the share price drop.

Comfortdelgro and its management are pathetic. Results for coming quarters will be worst. Going below $1 is a real possibility. Bail out now,

They don' t believe in TA

tangsookiam1947 ( Date: 27-May-2026 19:26) Posted:

why is insider buying?

ComfortDelGro' s largest shareholder tops up stake with open market buying at average of $1.29

JurongW ( Date: 27-May-2026 13:53) Posted:

Being a monthly chart, price progression could take years if results fail to improve.

Suitable for short‑ term trades (long or short), but not compelling for long term hold purely for a 5 to 6% dividend yield.

Over the long run, the dividends collected may not offset the cost of investment, leaving limited upside for patient holders.

|

|

|

|

why is insider buying?

ComfortDelGro' s largest shareholder tops up stake with open market buying at average of $1.29JurongW ( Date: 27-May-2026 13:53) Posted:

Being a monthly chart, price progression could take years if results fail to improve.

Suitable for short‑ term trades (long or short), but not compelling for long term hold purely for a 5 to 6% dividend yield.

Over the long run, the dividends collected may not offset the cost of investment, leaving limited upside for patient holders.

tangsookiam1947 ( Date: 27-May-2026 13:03) Posted:

| then better short this stock to the max? |

|

|

|

Being a monthly chart, price progression could take years if results fail to improve.

Suitable for short‑ term trades (long or short), but not compelling for long term hold purely for a 5 to 6% dividend yield.

Over the long run, the dividends collected may not offset the cost of investment, leaving limited upside for patient holders.

tangsookiam1947 ( Date: 27-May-2026 13:03) Posted:

then better short this stock to the max??

JurongW ( Date: 27-May-2026 02:12) Posted:

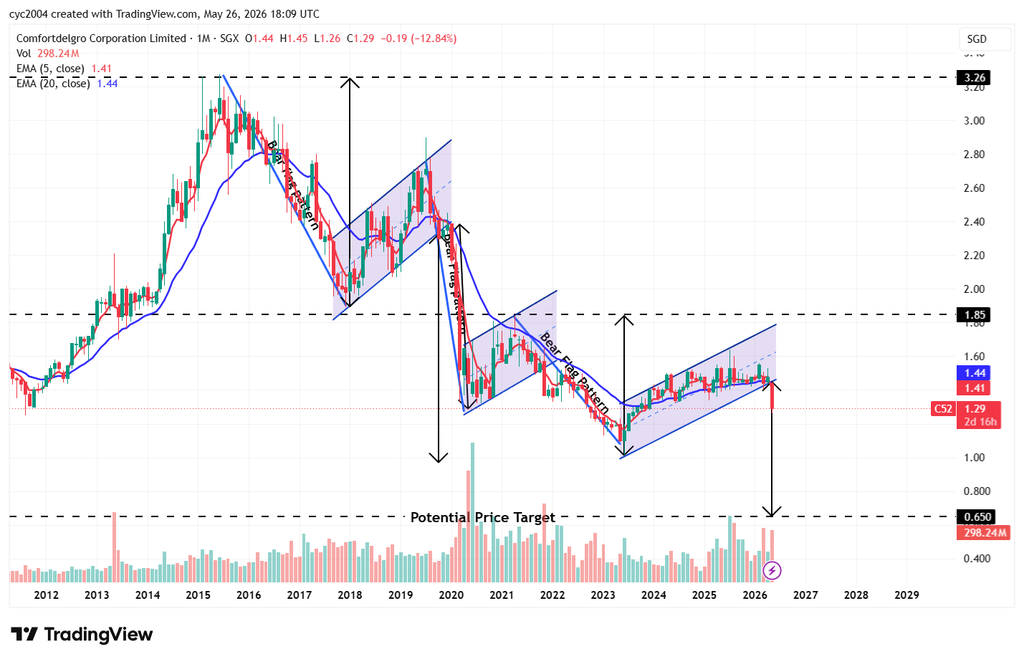

If you understand this chart, CDG has the potential to reach $0.65 over the long term !!!

|

|

|

|

then better short this stock to the max??

JurongW ( Date: 27-May-2026 02:12) Posted:

If you understand this chart, CDG has the potential to reach $0.65 over the long term !!!

|

|

If you understand this chart, CDG has the potential to reach $0.65 over the long term !!!

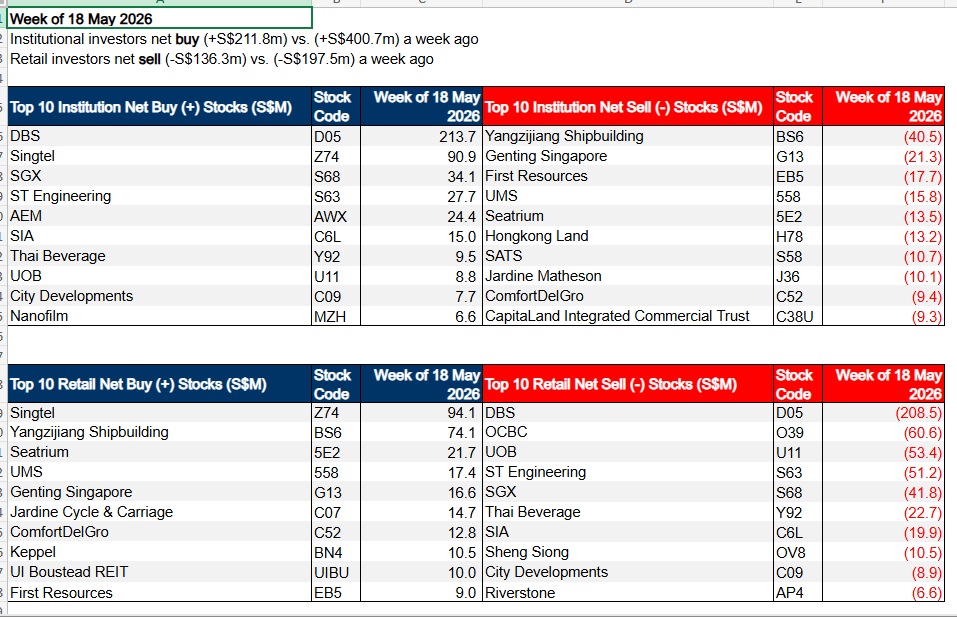

Institution investors were still selling CDG last week.

buy at under 1.10

- Overseas revenue contributed 55.3% of total group revenue in FY2025, up from 49.1% in FY2024.

- Overseas operating profit contribution rose to 44.7%, versus 34.9% previously.

They spent so much on acquisitions overseas. Where are the synergies?

ComfortDelGro is still in a manageable balance-sheet position overall. It is not in a dangerous net debt situation yet, but it is no longer sitting on a huge net cash pile like before its overseas expansion phase.

Recent figures show:

- Cash & equivalents around S$873m

- Total debt around S$1.69b

- Net gearing around 19.7% in FY2025, up from 6.7% previously due to acquisitions and expansion spending.

So technically:

- Gross debt > cash

- Therefore it is in a net debt position now, not net cash.

- But leverage is still considered moderate for a transport/infrastructure group.

The key question is whether dividends are sustainable.

Current situation:

- FY2025 payout ratio: 80%

- Total dividend: 8.5 cents

- PATMI: S$230.3m

- Yield around 5.5% ~ 6% depending on share price.

An 80% payout ratio is high, but not extreme for a mature transport company with stable cash flow. Many income stocks operate around 70 ~ 85%.

Why it still looks sustainable for now:

- Earnings are still growing

- FY2025 PATMI rose 9.4%

- Revenue exceeded S$5b for the first time.

- Cash-generating businesses

- Public transport, taxis, buses and rail are recurring-cashflow businesses.

- Overseas operations now contribute more than half of revenue.

- Debt still manageable

- Net gearing below 20% is not alarming.

- Management said their internal comfort benchmark is around 30%

CGD used to be net cash, and now it has become net debt...current dividend payout is not sustainable at the current rate!

Look at boustead. Super net cash at $0.65 to $0.70, and yet so conservative with their dividends. If boustead follows CDG, it would be like paying out 10 to 15 cents easily per annum (excluding one off gain...)spore1 ( Date: 24-May-2026 15:21) Posted:

Public Transport business is like that. Don't expect a higher ROE or Profit Margin. Their business is stable and resilient.

tangsookiam1947 ( Date: 23-May-2026 23:33) Posted:

| just a low ROE business....dying trades... |

|

|

|

Who is ah gong in this case?

Speediman ( Date: 23-May-2026 11:32) Posted:

| sell some more....ah Gong from overseas happily buy more.

I wouldn't be surprised they want to buy alot more to be a controlling shareholder |

|

Public Transport business is like that. Don't expect a higher ROE or Profit Margin. Their business is stable and resilient.

tangsookiam1947 ( Date: 23-May-2026 23:33) Posted:

just a low ROE business....dying trades...

spore1 ( Date: 23-May-2026 14:34) Posted:

| Just quietly grab some and keep. Pls dyodd |

|

|

|

Management is under the gun to deliver a good performance for the mid-year results in August.