Pain relief for GI Joes, giant leap for iX Biopharma

You might expect a pharmaceutical company founder to have a background in science or medicine. Instead, Catalist-listed iX Biopharma (SGX:42C) was founded by Eddy Lee, who spent most of his career in unrelated fields, from hospitality to telecommunications.

Instead of a formal education in science or something related, Lee earned his business degree from Australia&rsquo s Curtin University. Over the years, Lee, the chairman and CEO of iX Biopharma, held management roles at companies, including Genting Group in Malaysia, CDL Hotel International in Hong Kong, Star Cruises in Singapore and Amcon Telecommunications in Australia.

Lee recalls that after retiring from the corporate world, he was living in Perth when a group of Australian scientists approached him for support for a small study on fentanyl, a pain relief medication commonly used during labour and delivery.

He was drawn further in and soon asked to support an expanded study aimed at developing a more efficient drug delivery method than injections or drips: sublingual medication that dissolves under the tongue.

Lee, presumably aware of the challenges but also recognising the commercial potential, agreed and soon after, the company was founded in 2008. &ldquo That&rsquo s how I got started in the pharmaceutical space,&rdquo he says in an interview with The Edge Singapore.

Since pharmaceutical companies entered capital markets, the journey for upstarts in this space can be brutal. Companies could spend years on capital-intensive, multi-phase product development and clinical trials before receiving the necessary approvals to sell their products. The lucky few would become so-called &ldquo blockbusters,&rdquo resulting in epic paybacks others would soon find newer, more effective competitors in the pipeline. Along the way, there will be ups and downs, and investors&rsquo patience will be tested more than once.

For years, iX Biopharma&rsquo s share price languished well below its 2015 IPO level of 46 cents, as it endured a series of setbacks and continued losses. After reaching as high as 62 cents on its trading debut day, the company&rsquo s share price dipped to as low as 1.5 cents last year.

Yet, since early this year, things are finally looking up for iX Biopharma, with the US military coming in to help carry its product, Wafermine, used for pain relief, through to the later stages of development, which in turn, attracted new funding from enthusiastic investors eager to catch the ride up. In the past year, iX Biopharma&rsquo s share price has gained 1,700% to close at 36 cents on June 3, valuing the company at $375.64 million, making it one of the better-performing companies on the Singapore Exchange (SGX).

Lee has a ready answer for the share price&rsquo s lacklustre movements following the listing: a mismatch in expectations. &ldquo First, institutions were not interested and are not in their DNA to invest in biotech companies. Second, we told the market that we would take three to four years to get our flagship drug, Wafermine, to complete the Phase 2 studies and then we would out-license our drug, but the timeline got delayed.&rdquo

When the timeline was not met, the share price naturally came off. Meanwhile, to restore market confidence, iX Biopharma committed to the development of two additional products in addition to Wafermine: Wafersil and Wafernyl.

&ldquo Wafersil is a man&rsquo s Viagra-equivalent medical product, which is actually superior to Viagra. We did not focus too much on commercialisation, but we still developed it mainly to secure more knowledge of how the drug is developed and to get it registered with Australia&rsquo s Therapeutic Goods Administration (TGA),&rdquo Lee says.

&ldquo Wafernyl is a good, effective pain reliever, but it contains morphine, which is a potent opioid medication, and the US Food and Drug Administration (FDA) advised us not to pursue it,&rdquo Lee adds. Subsequently, amid the US opioid crisis, the company discontinued the development of Wafernyl.

Industry risks abound, and while iX Biopharma has encountered some, it has also avoided others. In the US, Purdue Pharma, owned by the Sackler family, the billionaire owners of the company long associated with the opioid crisis, produced the opioid OxyContin, a painkiller similar in use to Wafernyl.

Purdue Pharma&rsquo s aggressive marketing, which downplayed addiction risks, led to widespread abuse, thousands of lawsuits and ultimately its bankruptcy filing in 2019.

For iX Biopharma&rsquo s flagship product, Wafermine, Lee says it was more or less ready as early as 2017. &ldquo Once we completed Phase 2, we had a good meeting with the FDA in 2019, and they see the drug is good for acute pain, especially in pain involved in post-operations. &ldquo Back then, there was no non-opioid drug,&rdquo adds Lee.

However, Lee did not push ahead to bring Wafermine to the subsequent Phase 3 and then commercialisation &mdash an endeavour which he figures would cost US$30 million ($38.4 million) that iX Biopharma, with its share price at around 20 cents and a market cap of just $150 million then, did not have.

The typical drug development cycle consists of four phases. The third phase &mdash following which FDA&rsquo s formal approval is sought &mdash is typically the most costly, as it involves enrolling up to 3,000 patients to confirm efficacy. &ldquo Raising that sum of money will crush our share price, and our market won&rsquo t give it to me,&rdquo Lee reasons.

Instead, Lee signed an exclusive licensing agreement with then-Nasdaq-listed Seelos Therapeutics Inc in November 2021. Under the agreement, Seelos was to fund all future development, manufacturing and commercialisation of Wafermine.

According to Lee, there were other potential partners, but he was won over by Seelos&rsquo chief medical officer, who he says was very knowledgeable about ketamine and shared his values.

However, things took a turn when Seelos was unable to advance development, as its broader drug pipeline encountered difficulties. The company was eventually delisted from Nasdaq and, in 2024, effectively became defunct. According to Lee, iX Biopharma&rsquo s chief commercial officer Eva Tan then spent six months working to reclaim Wafermine after the deal with Seelos fell through in 2024.

JV with Orion Specialty Labs

Despite the setback, Lee and his team pressed on. In November, iX Biopharma signed a non-binding term sheet with US-based Orion Specialty Labs, whose shareholder is investment firm GLD Partners, to establish a manufacturing and commercialisation base in the United States. Under the proposed joint venture, iX Biopharma will hold a 75% stake, with Orion holding the remaining 25%.

In the same interview, Tan shares that before the non-binding term sheet with Orion, iX Biopharma was still relatively unknown in the US. &ldquo For some reason, there was a lot of interest in our longevity products from the pharmaceutical companies. They shared that the products are not available anywhere in the US, and they are excited to see this, especially Orion,&rdquo says Tan.

&ldquo Orion believes that with the growth of telehealth, we will be able to supply various telehealth companies such as Hims & Hers and Ro, and that will be a big differentiator,&rdquo she adds.

Under the arrangement with Orion, the US company is offering its FDA-registered facility to iX Bioparma, which has the approvals and capabilities to do compounded drugs in bulk. For Orion&rsquo s part, it will spend US$10 million in capex to support the production. A US-based manufacturing facility, of course, will not be subject to tariffs imposed by the US on products made elsewhere.

&ldquo With the products and infrastructure in place, we are now ready to pursue the compounding pharmacy pathway in the US,&rdquo says Tan, adding that by early 2027, iX Biopharma will be ready to launch its own direct-to-consumer business model.

On May 11, iX Biopharma announced that it will restructure its consumer business by consolidating its Australia and Hong Kong subsidiaries and the proposed WaferiX direct-to-consumer (DTC) telehealth platform currently under development into a newly incorporated holding company to be known as Ligo Pharma. By doing so, the company aims to unlock value and preserve flexibility for future corporate action, including a spin-off listing on SGX or Nasdaq.

At the same time, iX Biopharma is in advanced talks with GLD to set up a joint venture that would incorporate Orion into the Ligo structure. &ldquo The proposed joint venture, if concluded, would represent a significant deepening of the relationship between the parties,&rdquo iX Biopharma says.

US defence contractor

Besides this deal with Orion, iX Biopharma was in the news recently for a bigger reason. In February, the US Department of War awarded US$41 million to fund the development of Wafermine &mdash the product Lee tried to push through with Seelos. SGX-listed companies routinely receive Singapore government contracts, but securing funding and potentially generating revenue from the Pentagon is presumably not common.

The funding was provided through the Defence Health Agency Contracting Activity (DHACA). The funds will be used to support Wafermine&rsquo s Phase 3 clinical development and a subsequent bid to secure FDA approval for the Department of War to use this drug over three years under an arrangement called Emergency Use Authorization (EUA).

Lee recalls that in 2016 and 2017, the US military was seeking a battlefield painkiller, with iX Biopharma&rsquo s Wafermine competing against &ldquo the best in the US&rdquo . However, the company lacked sufficient clinical data at the time and could not advance to later stages of clinical trials.

How iX Biopharma' s Wafermine stacks up against similar products / Photo: iX Biopharma

As a result, iX Biopharma did not take part in the bidding, despite what Lee describes as strong interest from the US military. &ldquo We were very close, but we just do not have the data to back us up.&rdquo

However, the US military did not forget about iX Biopharma. In May last year, the company was approached about collaborating on the registration of Wafermine for post-operative pain relief. By September, the Department of War was reportedly satisfied with the technology and data and confident that Wafermine had a strong chance of succeeding in Phase 3 trials.

Under the subsequent agreement, the Department of War will fork out US$41 million to fund iX Biopharma&rsquo s labour and project costs associated with the programme through a combination of fixed monthly payments and cost reimbursements of actual costs incurred. Meanwhile, the EUA mechanism permits the use of products that have not yet been approved by the FDA when the known benefits outweigh the potential risks and no approved alternative exists.

According to iX Biopharma, in a recent presentation, Wafermine may be included as a standard-issue item in US military medical kits. In addition, the Department of War may consider Wafermine for veterans.

The market goes beyond the men and women in uniform. According to the company, citing a report from Delve Insight, the total addressable market for acute, moderate-to-severe pain in key US markets was worth US$44.5 billion in 20205 and is expected to grow at a CAGR of 13% to reach US$14 billion by 2034.

Meanwhile, in the near term, come next January, once the EUA takes effect, the company will generate cash by supplying Wafermine to the US military. &ldquo This will be the future for iX Biopharma,&rdquo says Lee.

Department of War backing fuels surge

The company&rsquo s share price has since recovered sharply. It hovered around two cents for the first nine months of 2025 before beginning a strong rebound in late September and crossing the 10-cent level by late October.

The higher share price helped create a more conducive environment for iX Biopharma to tap the market for new capital. Last October, the company announced a placement to raise proceeds of just below $5 million. However, due to strong investor demand, the placement was upsized by a third to $6.7 million. Institutional investors such as Lion Global Investors and Ginko-AGT Global Growth Fund together subscribed for 67 million new shares at 10 cents each.

After nearly two decades leading the company through difficult periods, Lee moved quickly to seize the momentum. Just four months after the October 2025 placement and the Department of War contract win on Feb 13, iX Biopharma returned to the market with another placement to raise at least $6 million.

Again, investor demand was strong, despite iX Biopharma selling the shares this time round at a much higher price. As in the previous round, the placement was upsized, even though book-building took place during what is typically a quiet Chinese New Year period for markets.

A total of $15 million was eventually raised by issuing 75.8 million new shares at 19.8 cents each, 150% above the initial plan. Of this amount raised, $13 million is for interim funding to fulfil the Department of War contract, and the remaining $2 million is for debt repayment. &ldquo We are now fully funded,&rdquo says Lee.

Interestingly, the market took some time to appreciate the significance of the Department of War contract, as reflected in iX Biopharma&rsquo s share price movement. That timing, however, worked in Lee&rsquo s favour. For listed companies managing capital carefully, when and how they raise funds can make a significant difference. In this sense, the Department of War contract provided a form of non-dilutive funding at a critical stage in Wafermine&rsquo s development.

&ldquo When we announced the Department of War contract, internally, we believe that the value we created for the company is far greater than what is currently being reflected in the market,&rdquo says Tan, pointing out that the company&rsquo s share price moved only &ldquo marginally&rdquo .

&ldquo We got really lucky to be able to raise $15 million with our share price near the 20-cent mark. Imagine the same $15 million raised at the 10 cents mark the dilution impact will be much greater,&rdquo adds Lee, who holds a stake of 22.5% in the company following the two rounds of placement.

While some investors have responded to recent developments, the surge in iX Biopharma&rsquo s share price has been linked in part to a single call by Paul Chew of PhillipCapital. Chew previously covered the stock during its deal with Seelos, which eventually fell through, and faced criticism for his earlier coverage. On April 10, following the Department of War deal, he re-initiated coverage with a &ldquo buy&rdquo call and a $1 target price.

Following Chew&rsquo s call, iX Biopharma&rsquo s share price gained 65% on the same day, with 130 million shares changing hands. &ldquo The US government is not only funding you but also buying from you and for military use,&rdquo says Chew.

In effect, the Pentagon is backing iX Biopharma as it moves to clear the FDA&rsquo s regulatory hoops. &ldquo Imagine you are meeting the FDA, and there&rsquo s a US colonel or general behind you &mdash is the FDA going to say no?&rdquo says Chew at a recent presentation. In addition, the company does not necessarily need to manufacture the drugs itself. It can either license manufacturing to other pharmaceutical companies to produce it or sell the IP to competitors, he adds.

Potential Nasdaq dual listing

iX Biopharma&rsquo s turnaround comes amid improving sentiment in the local stock market, supported by measures such as the Equity Market Development Programme (EQDP), which have drawn greater attention to small- and mid-cap companies in Singapore.

Lee agrees that the measures are providing small- and mid-cap companies like iX Biopharma with good exposure to market participants. &ldquo Without these measures, nobody wants to talk to us at one point of course, right now we have reached a level where we attract some interest,&rdquo he says.

&ldquo As SGX has shared, since the launch of the EQDP, the benefit has really flowed through to the small and mid-cap companies and has made the most impact. Because of that, the interest has since spread outside of Singapore,&rdquo adds Tan.

iX Biopharma recently took part in a roadshow organised by SGX in Kuala Lumpur, and the exchange brought along a handful of much larger companies. According to Tan&rsquo s observation, the company actually garnered much more interest.

At its most recent AGM last October, the company told shareholders it is considering a dual listing on Nasdaq within the next 12 to 18 months and Lee says the company is almost ready for a US listing. After all, the recent Department of War deal, which also makes iX Biopharma a US defence contractor, will be a good pitch for US investors.

&ldquo Right now, within the US biopharma space, you start to see a slight change in attitude as they will want to acquire your drugs quickly. You look at Eli Lilly, which recently bought out Nimbus&rsquo oral obesity drug and Novo Nordisk, which acquired clinical-stage biotech company Akero Therapeutics,&rdquo Lee says.

Lee adds that once the drug is found to be viable and effective, biopharmaceutical companies will pay top dollar to acquire iX Biopharma. &ldquo So, we believe that might happen to us and therefore we want to push forward our plans for the dual listing.&rdquo

Meanwhile, the company is in a better financial shape, as shown by the most recent financial results. For the nine months to March, gross margin improved to 30%, up from 24% a year ago, driven by a more favourable sales mix and cost management. At the same time, it reduced its net loss by 65% y-o-y to $2.97 million from $8.44 million a year ago, supported by favourable forex movements.

For Lee, the company&rsquo s toughest period is over. He is now &ldquo probably&rdquo less worried and more upbeat about the prospects ahead. &ldquo Our game plan is very clear for the rest of 2026. First, we will try to secure the EUA, which means we will be profitable by next January. In the next few months, we will finalise our contractual relationship with Orion and transfer our 30 assets to it. So I think it could be a better year ahead for us.&rdquo

Good to be aware of the risk. Not everyone has such risk appetite.

All good...Not to worry.

Trendline is in a similar situation.

Many have lost money but again that is because investment timeline is off.

Incubation needs time and 1 of their startup Phytolon is accelerating towards a final exit as it commences commercial production of naturnal dyes.

But again patience is needed

Trendline is in a similar situation.

Many have lost money but again that is because investment timeline is off.

Incubation needs time and 1 of their startup Phytolon is accelerating towards a final exit as it commences commercial production of naturnal dyes.

But again patience is needed

ahberngh ( Date: 05-Jun-2026 16:31) Posted:

|

Perhaps you misunderstand me  .

.

No offence to anyone, huat to all believers.

.No offence to anyone, huat to all believers.

SmallSmall ( Date: 05-Jun-2026 15:48) Posted:

|

That is because you are looking at the past.

Suggest you read up the article in The Edge.

Provides an indepth into what is forward looking.

Not saying it will happen but if they execute it nicely......It will be a different story.

Not suggesting a Buy or Sell just for reading pleasure

Suggest you read up the article in The Edge.

Provides an indepth into what is forward looking.

Not saying it will happen but if they execute it nicely......It will be a different story.

Not suggesting a Buy or Sell just for reading pleasure

ahberngh ( Date: 05-Jun-2026 14:35) Posted:

|

If one wants to look at profit, cash flow, nav, cash in hand, PE, debt

to equity ratio, etc and all the meaningful indicators, one must not

invest in this stock.

From the time I first invested (2020) until today, it is cash burn, burn, burn,...

In fact, for the last 2 years or so, the auditors have flagged them as

a going concern issue. They were desperate for capital....

Just my opinion, please dyodd.

to equity ratio, etc and all the meaningful indicators, one must not

invest in this stock.

From the time I first invested (2020) until today, it is cash burn, burn, burn,...

In fact, for the last 2 years or so, the auditors have flagged them as

a going concern issue. They were desperate for capital....

Just my opinion, please dyodd.

stockpicker ( Date: 05-Jun-2026 08:42) Posted:

|

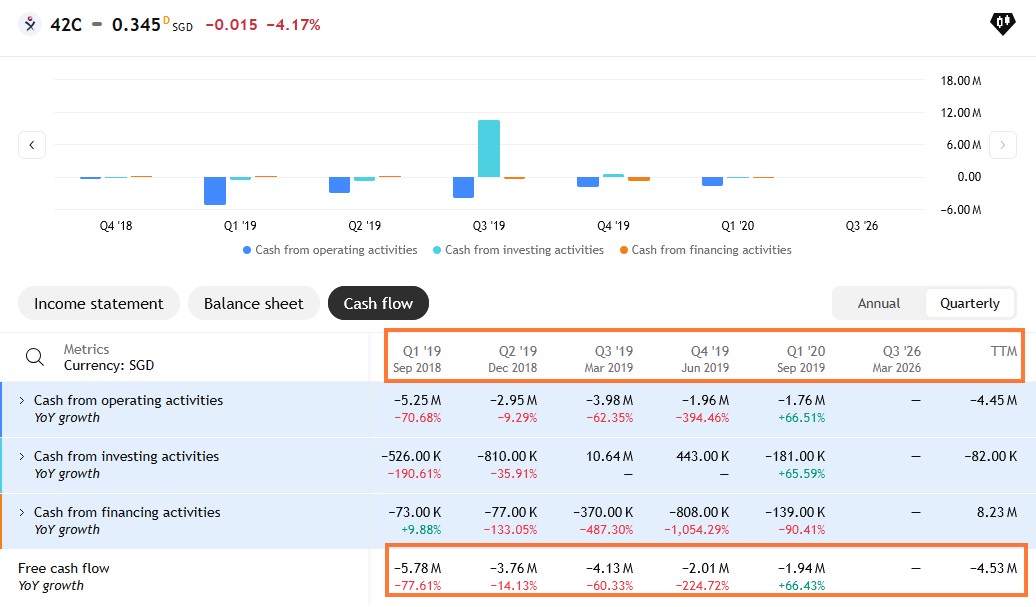

Hard to judge if they are fundamentally sound as the TV' s record is incomplete with many quarterly figures missing. The Annual fighres shows that this counter has negative Net Income and Free Cash Flow most of the time, which does not sound good.

Share price now touching the trendline support as well as 0.5 fibo level at 35 cents.

Short term (5, 10, 20 EMA) - down, long term (50, 100, 200 EMA) - up

If price continue dropping, 50 EMA should provide firm support as evidenced from the prior pull back.

Short term (5, 10, 20 EMA) - down, long term (50, 100, 200 EMA) - up

If price continue dropping, 50 EMA should provide firm support as evidenced from the prior pull back.

So the result is will drop further?

ahberngh ( Date: 03-Jun-2026 16:45) Posted:

|

Yes, no need to worry, just look at the 100d and 200d

moving averages, the price action and the volmes.

2 black candles with high volumes, 2 red candles with lower volumes.

Just my opinion, please dyodd.

moving averages, the price action and the volmes.

2 black candles with high volumes, 2 red candles with lower volumes.

Just my opinion, please dyodd.

JurongW ( Date: 03-Jun-2026 16:25) Posted:

|