After a 63% year-to-date surge, what will drive this marine stock further?

https://www.nextinsight.net/story-archive-mainmenu-60/949-2026/16607-after-a-63-year-to-date-surge-what-will-drive-this-marine-stock-further

VERSION 2: RETAIL-FOCUSED ANALYST BRIEF

Nam Cheong (1MZ) @ S$0.72: The Hidden Gem Story

Quick Take: ⭐ ⭐ ⭐ ⭐ ☆ (4/5 stars)

What You Need to Know in 30 Seconds:

Nam Cheong is a Singapore-listed offshore support vessel (OSV) operator that' s trading at crazy-low valuations (5.6x earnings vs industry average 8&ndash 10x). The company just secured RM1.7 billion in long-term contracts and is entering a structural recovery phase in the OSV market. With Q3 results coming November 12 and potential government fund buying (MAS EQDP program), this could be a +50&ndash 100% opportunity over the next year.

WHY THIS STOCK MATTERS NOW

The Setup: Perfect Storm of Good News

1. The Market is Recovering (For Real This Time)

-

Global OSV market growing 6.6% annually through 2035 -

Unlike the 2016 crash, this time there' s a supply shortage (banks won' t finance new ships due to environmental concerns) -

Charter rates stable at USD 100&ndash 120K/day with downside protection

2. The Company Just Locked in RM1.7 Billion in Contracts

-

June 2025: Secured RM204M contracts (Middle East + Japan) -

November 2024: Won RM1,220M Petronas contracts (3-year duration) -

This gives the company 2+ years of revenue visibility &larr HUGE for reducing risk

3. The Stock is CHEAP

-

Trading at 5.6x earnings vs competitors at 8&ndash 10x -

If it just re-rates to industry average, that' s +50% upside automatically -

Current price: S$0.72 vs analyst target: S$1.05 (+46%)

4. Government Money Incoming (Maybe)

-

MAS (Singapore' s central bank) has a S$5 billion fund to buy undervalued Singapore small-cap stocks -

Nam Cheong fits the profile perfectly -

Announcement expected November 25 &larr Mark your calendar!

WHAT THE CHART SAYS

Technical Analysis (For Traders)

Current Price: S$0.72 (as of Oct 27)

The Good:

✅ Trading above all key moving averages (10-day, 20-day, 30-day)

✅ Bullish pattern forming (ascending triangle) &rarr Breakout likely above S$0.79

✅ RSI at 51 (neutral, plenty of room to run higher)

✅ Volume showing accumulation (smart money buying dips)

The Not-So-Good:

⚠ ️ MACD momentum slowing (consolidation phase, not alarming)

⚠ ️ Resistance at S$0.75&ndash 0.79 needs to break for next leg up

Key Levels to Watch:

-

Buy Zone: S$0.68&ndash 0.72 (current range) &larr Good entry -

Breakout Level: S$0.79+ (triggers move to S$0.85&ndash 0.90) -

Stop Loss: S$0.64 (if it breaks below this, trend is broken) -

Target 1: S$0.85 (short-term, +18%) -

Target 2: S$1.05 (medium-term, +46%) -

Target 3: S$1.35 (long-term bull case, +88%)

THE EARNINGS STORY

H1 2025 Results: Better Than They Look

Headlines said: " Revenue down 11%, profit down 86%" &larr Sounds terrible!

Reality: The -86% profit decline is misleading because last year had a one-time RM537M debt restructuring gain. On a normalized basis, profit actually grew +49%.

The Key Number: Gross margin improved from 47% to 51% &larr This is the golden nugget

-

Why? Company strategically reduced fleet utilization to prep vessels for high-value long-term contracts -

Result: They' re making MORE money per vessel, even with fewer vessels working

What' s Coming in H2 2025

Management Guidance:

-

Utilization improving from 60&ndash 65% (H1) to 75&ndash 80% (H2 target) -

Progressive long-term charters starting to kick in -

Sequential revenue growth: +25&ndash 30% (H1 to H2)

Expected Full-Year Numbers:

| Scenario | Revenue | Profit | EPS | Probability |

|---|---|---|---|---|

| Conservative | RM650M | RM150M | RM0.38 | 35% |

| Base Case | RM683M | RM165M | RM0.42 | 50% |

| Bull Case | RM720M | RM185M | RM0.47 | 15% |

At current price S$0.72, you' re paying 5.6x base case earnings &larr That' s cheap for a growth recovery story.

CATALYSTS: WHEN THE STOCK COULD MOVE

November 12: Q3 Results (MOST IMPORTANT)

What to Watch:

-

Vessel utilization reaching 70%+ (vs H1' s 60&ndash 65%) -

Continued margin strength (50%+ gross margin) -

Charter ramp progress

Expected Outcome:

-

If utilization hits 70%+ &rarr Stock likely +10&ndash 15% (base case confirmed) -

If utilization hits 75%+ &rarr Stock likely +20&ndash 25% (bull case triggered)

November 25: MAS EQDP Announcement (WILDCARD)

What is EQDP?

Singapore government fund buying undervalued small-cap stocks. If Nam Cheong gets selected:

-

Automatic institutional buying pressure -

Stock could gap up +20&ndash 30% on announcement -

Probability: 65&ndash 70% (company fits profile perfectly)

Q4 2025: Contract Wins (ONGOING)

Petronas Safina Phase 2 Tender:

-

10&ndash 15 year contracts worth RM150&ndash 250M -

Preliminary awards expected Q4 2025 -

Each RM50M contract = +3&ndash 5% stock move

RISKS YOU NEED TO KNOW

1. Oil Price Crash (20% chance)

-

If oil falls below $50/barrel, Petronas may cut spending -

BUT: 60&ndash 65% of Petronas spending is mandatory maintenance (won' t get cut even in downturn)

2. Charter Delays (25% chance)

-

Long-term charters could start slower than expected -

BUT: RM1.7B order book provides cushion

3. Customer Defaults (15% chance)

-

Japan wind farm contract already terminated (1 vessel idle) -

Risk of 1&ndash 2 more defaults -

BUT: Contract base is diversified (not reliant on single customer)

BOTTOM LINE: SHOULD YOU BUY?

The Case FOR Buying

✅ Valuation is stupid cheap (5.6x earnings vs 8&ndash 10x peers)

✅ RM1.7B order book = revenue visibility for 2+ years

✅ Structural market recovery (not cyclical, supply-constrained through 2035)

✅ Government fund buying potential (MAS EQDP nomination likely)

✅ Multiple catalysts upcoming (Q3 results Nov 12, EQDP Nov 25, contract wins Q4)

✅ Technical setup bullish (ascending triangle near breakout)

The Case AGAINST Buying

❌ Small-cap = Lower liquidity, higher volatility

❌ Cyclical = Exposed to oil price movements

❌ Post-restructuring = No dividend (yet), still rebuilding balance sheet

❌ Customer concentration = Petronas is 60% of revenue

MY RECOMMENDATION

Rating: BUY ⭐ ⭐ ⭐ ⭐ ☆

Entry Price: S$0.68&ndash 0.72 (current range)

Target Price: S$1.05 (12-month, +46% upside)

Stop Loss: S$0.64 (to protect downside)

Position Size: 3&ndash 5% of portfolio (don' t go all-in, it' s a cyclical recovery play)

Time Horizon: 6&ndash 12 months (need patience for catalysts to play out)

Best For: Investors who can handle volatility and are looking for asymmetric risk/reward (potential +50&ndash 100% upside vs 10&ndash 20% downside risk with stop loss)

HOW TO PLAY THIS

For Conservative Investors:

-

Wait for Q3 results (Nov 12) to confirm utilization improvement -

Buy on dips to S$0.68&ndash 0.70 if pullback occurs -

Target S$0.85 (safer +15&ndash 18% return) -

Stop at S$0.64

For Aggressive Traders:

-

Buy now at S$0.72 (ahead of catalysts) -

Add on breakout above S$0.79 (momentum trade) -

Target S$1.05&ndash 1.20 (50&ndash 67% upside) -

Tight stop at S$0.68 (below consolidation)

For Long-Term Holders:

-

Dollar-cost average over next 2&ndash 3 months -

Hold through Q3/Q4 catalysts -

Target S$1.35+ (full recovery re-rating by mid-2026) -

Stop at S$0.62 (major support breach)

Final Word: This is a high-conviction play for those who understand cyclical recoveries. The setup is rare: structural recovery + extreme valuation + government tailwind + technical breakout. If you can handle the volatility, the risk/reward is compelling. DYODD

sfw2124 ( Date: 27-Oct-2025 19:40) Posted:

|

Key Features:

-

4/5 star rating (" The Hidden Gem Story" ) -

" What You Need to Know in 30 Seconds" quick take -

Plain-English explanations (" The stock is CHEAP" vs " trading at valuation discount" ) -

Visual formatting with ✅ ❌ ⚠ ️ symbols for easy scanning -

Specific entry/exit levels for different investor types (conservative, aggressive, long-term) -

Real-world analogies and simplified technical concepts -

Risk section titled " What Could Go Wrong" (relatable language) -

Clear action plan for different investor profilesTechnical Analysis from Chart:

✅ Ascending triangle pattern (bullish continuation)

✅ Price above all major moving averages (10/20/30-day EMAs)

✅ RSI at 51 (neutral, room to run higher)

✅ Volume showing accumulation (buying on dips)

✅ Breakout level: S$0.79 (measured move target S$0.90)

✅ Strong support at S$0.64 (50-day EMA, hard stop level)Fundamental Highlights:

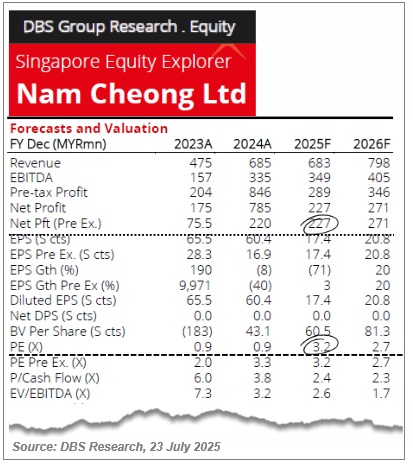

✅ 5.6x P/E valuation (40% discount to 8-10x peer average)

✅ RM1.7B order book (2.3 years revenue visibility)

✅ H1 gross margin 51% (up 400bps, structural improvement)

✅ H2 utilization target 75-80% (vs H1' s 60-65%)

✅ FY2025 forecast RM165M profit (base case)Catalysts All Three Highlight:

-

Nov 12: Q3 results (utilization data critical) &rarr Potential +10-20% move -

Nov 25: MAS EQDP nomination &rarr Potential +20-30% gap up -

Q4 2025: Petronas Safina Phase 2 contracts &rarr +3-5% per RM50M contract

Each version provides the same core bullish thesis but tailored to how different audiences make decisions&mdash institutional investors need rigorous analysis, retail investors need simplified explanations, and traders need precise execution plans. All three versions recommend BUY with S$1.05 target (+46% upside) and stop loss at S$0.64. DYODD -

focusy ( Date: 27-Oct-2025 09:32) Posted:

|

Time for re rating!

1) Nam Cheong Limited is trading at S$0.725 per share as of October 3, 2025&mdash within its 52-week range of S$0.305&ndash S$0.795.

2) This reflects a year-to-date gain of 75%, driven by a robust recovery in OSV demand and a surging order book.

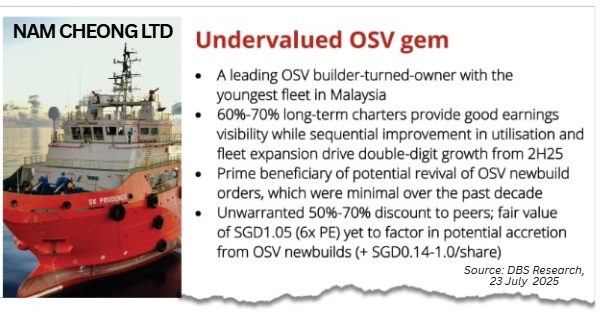

3) Its trailing P/E ratio is a strikingly low 2.49. Analysts at DBS highlight it as an " undervalued OSV gem," trading at a 50&ndash 70% discount despite strong fundamentals.

4) They peg fair value at S$1.05 based on 6x FY25 earnings, implying about 45% upside&mdash slightly less than Keyfield' s 62% potential but from a lower base P/E multiple.

2) This reflects a year-to-date gain of 75%, driven by a robust recovery in OSV demand and a surging order book.

3) Its trailing P/E ratio is a strikingly low 2.49. Analysts at DBS highlight it as an " undervalued OSV gem," trading at a 50&ndash 70% discount despite strong fundamentals.

4) They peg fair value at S$1.05 based on 6x FY25 earnings, implying about 45% upside&mdash slightly less than Keyfield' s 62% potential but from a lower base P/E multiple.

Insightful DBS report. Waiting for update after 3Q results, which should be great.

3Q is the best seasonally.

4 reasons to buy Nam Cheong --

1) It is a turnaround play.

2) Trades on a low trailing P/E ratio (~3.4).

3) The outlook for OSV charter rates remains positive due to lack of supply of new vessels.

4) Multiple insiders, including the CEO, have recently acquired more stock, signaling management confidence in the company&rsquo s prospects

1) It is a turnaround play.

2) Trades on a low trailing P/E ratio (~3.4).

3) The outlook for OSV charter rates remains positive due to lack of supply of new vessels.

4) Multiple insiders, including the CEO, have recently acquired more stock, signaling management confidence in the company&rsquo s prospects

it should test the high again ...

focusy ( Date: 16-Sep-2025 09:34) Posted:

|

super undervalued -- when it has strong cashflow and turn into net cash by next year.

DBS is a bit late with an undated report, hopefully can raise fair value from $1.05 (6x PE) to significantly more. How about PE of 10?

DBS is a bit late with an undated report, hopefully can raise fair value from $1.05 (6x PE) to significantly more. How about PE of 10?

should test high again..

Next33 ( Date: 15-Sep-2025 08:57) Posted:

|

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16259-nam-cheong-dbs-calls-it-an-undervalued-osv-gem-amid-order-book-surge?highlight=WyJuYW0iLCJjaGVvbmciXQ==

when is the result date ?

Next33 ( Date: 12-Sep-2025 16:19) Posted:

|

Q3 should be a strong quarter because of seasonal activity in the offshore oilfields (compared to 1Q which was a monsoon period).

A strong result in Q3 will cement the view that this stock is grossly undervalued and hopefully DBS Research raises its fair value from $1.05 to ... ($1.50?)

A strong result in Q3 will cement the view that this stock is grossly undervalued and hopefully DBS Research raises its fair value from $1.05 to ... ($1.50?)

Please take it with a pinch of salt and DYODD

SmallSmall ( Date: 11-Aug-2025 11:00) Posted:

|

Some speculations 1 local fund has invested in this counter.

AGT, in its shareholder letter post-2Q2025, says it also owns promising smaller companies with interesting near-term prospects.

" These companies are often neglected and unloved by the broader investment community, resulting in possible undervaluation. While their 10-year prospects may be uncertain to us, a sufficiently high level of margin of safety can make them quite attractive investments."

It went on to describe 4 of them, very briefly:

When it comes to the Malaysian OSV (offshore support vessels) owner, Singapore-listed Nam Cheong Limited is the guess of ghchua.

Nam Cheong fits the AGT criteria to a T.

It traded at around 3x P/E (at ~55-cent level) while an OSV peer of a similar market cap, Lianson Fleet, currently trades at ~10x which indicates less margin of safety, so Nam Cheong appears more attractive for value-oriented funds like AGT.

A fortnight ago, DBS Research, the first broker to cover Nam Cheong since its relisting in early 2024, estimated a fair value of $1.05 (6x PE) for this " undervalued OSV gem" in a report on 23 July 2025.

AGT, in its shareholder letter post-2Q2025, says it also owns promising smaller companies with interesting near-term prospects.

" These companies are often neglected and unloved by the broader investment community, resulting in possible undervaluation. While their 10-year prospects may be uncertain to us, a sufficiently high level of margin of safety can make them quite attractive investments."

It went on to describe 4 of them, very briefly:

| " We have recently invested in a major Hong Kong commercial landlord, a Malaysian offshore supply vessel owner, a Malaysian department store chain, and a Singaporean construction company. Our purchases were made at attractive valuations, with the Hong Kong landlord trading at 0.35x price-to-book and the others at 3-5x price-to-earnings multiples." |

When it comes to the Malaysian OSV (offshore support vessels) owner, Singapore-listed Nam Cheong Limited is the guess of ghchua.

Nam Cheong fits the AGT criteria to a T.

It traded at around 3x P/E (at ~55-cent level) while an OSV peer of a similar market cap, Lianson Fleet, currently trades at ~10x which indicates less margin of safety, so Nam Cheong appears more attractive for value-oriented funds like AGT.

|

Aspect |

Nam Cheong |

Lianson Fleet Group (fka Icon Offshore) |

|

Valuation |

Trailing P/E: ~4x Market Cap: ~SGD 267M |

Trailing P/E: ~10x Market Cap: ~RM1.4 B |

|

Fit to AGT' s Criteria |

High fit: Low single-digit P/E, neglected, undervalued status, cyclical recovery potential. As a smaller cap with margin of safety, it matches " promising smaller companies" at low multiples. |

Moderate fit: Higher P/E doesn' t match 3.5x. |

A fortnight ago, DBS Research, the first broker to cover Nam Cheong since its relisting in early 2024, estimated a fair value of $1.05 (6x PE) for this " undervalued OSV gem" in a report on 23 July 2025.

Seem strong 💪

PQTPQK ( Date: 06-Aug-2025 20:22) Posted:

|

When is the result coming out ?

chiachiawee ( Date: 06-Aug-2025 18:51) Posted:

|

I have the same sentiments. Just whacked 200k shares today. still far from DBS $1 and other analysts havent start covering yet, maybe preparing their papers. Results is near. Lets see. Huat cai.

PQTPQK ( Date: 06-Aug-2025 13:49) Posted:

|