Tan Kim Seng is a well known Singapore investor and dealmaker who recently bought into Beng Kuang Marine during the founder&rsquo s discounted share sale. He is the co founder of private equity firm Tembusu Partners and the founder/former executive chairman of KS Energy Services, giving him strong credibility in the energy and marine sector.

📌 Profile of Tan Kim Seng

- Background: Veteran investor with decades of experience in energy, marine engineering, and private equity.

- Key Roles:

- Founder & former Executive Chairman of KS Energy Services, an oilfield services and drilling equipment provider.

- Co founder of Tembusu Partners, a Singapore‑ based private equity firm focused on growth capital and impact investments.

- Reputation: Considered a reputable, long‑ term investor with strong networks in the energy and infrastructure space.

🛠 His Involvement in Beng Kuang Marine

- Transaction: Participated in the May 2026 founder&rsquo s share sale at $0.48 per share, alongside institutional funds like Amova Asset Management and Tokio Marine Life Insurance Singapore.

- Significance: His entry adds credibility to Beng Kuang Marine shareholder base, signaling confidence in the company offshore lifecycle services and marine engineering strategy.

- Market Impact: The presence of a seasoned investor like Tan Kim Seng helps balance retail concerns about the steep discount, as institutions and reputable individuals often negotiate such terms for large block trades.

⚖ ️ Why His Stake Matters

- Investor Confidence: His participation suggests that despite the discount, he sees long term value in Beng Kuang Marine business.

- Sector Expertise: With his KS Energy background, he understands the offshore/marine cycle and may be positioning for recovery or growth in recurring service revenues.

- Signal to Market: Retail investors may feel disadvantaged, but institutional and reputable investors like Tan Kim Seng often set the tone for future confidence in the stock.

✅

Takeaway for you: Tan Kim Seng is not just a random buyer, he is a seasoned energy and private equity player. His entry into Beng Kuang Marine at a discounted block price signals institutional grade confidence, even if retail investors feel short changed by the steep discount.

Would you like me to

map out a scenario table showing how his entry (alongside Amova and Tokio Marine) could influence Beng Kuang Marine&rsquo s share price trajectory in the short vs. medium term? That would give you a clearer calibration for trading decisions.

BKM 1Q26: Revenue up 7.7% YoY to S$25.7m, net profit S$2.8m (&darr 12.7% YoY, &uarr 9% QoQ)

FPSO remains anchor with S$27.6m secured, shipbuilding ramps at Batam

all eyes on May EGM for ASOM consolidation.

https://links.sgx.com/1.0.0/corporate-announcements/JV7BFFNT0R2OMNIU/887608_BKM%201Q2026%20Business%20Update.pdf

Beng Kuang Marine (BKM) delivered a steady 1Q2026 with revenue up 7.7% YoY to S$25.7m, though margins compressed due to a heavier shipbuilding mix. Net profit came in at S$2.8m, down 12.7% YoY but up 9% QoQ, supported by lower admin costs and recurring FPSO work anchoring the business.

📊 Key Financial Highlights (1Q2026)

Revenue: S$25.7m (+7.7% YoY, +20.3% QoQ)

Gross Profit: S$6.8m (&darr 21.5% YoY, &darr 10.7% QoQ)

Gross Margin: 26.5% (&darr 9.9pp YoY)

PBT: S$3.0m (&darr 28.1% YoY, +4.6% QoQ)

Net Profit: S$2.8m (&darr 12.7% YoY, +9% QoQ)

Admin Costs: 13% lower YoY

👉 Margins dipped because shipbuilding and early-stage work contributed more this quarter, compared to higher-margin FPSO services.

📦 Order Book & Secured Revenue

Total Order Book (as of 31 Mar 2026): S$55.9m

FY2026 Revenue Already Secured: ~S$51.2m (by week 13)

FPSO lifecycle services (ASOM): ~S$27.6m (54%)

Shipbuilding (Batam yard, NEI): S$15.8m (31%)

Deck equipment & cranes (IOE): ~S$7.8m (15%)

🔑 Segment Performance

FPSO (ASOM): Core recurring engine 19 vessels across 7 countries, ~S$27.6m secured for FY2026.

Shipbuilding (NEI): Ramp-up at Batam yard with 4 projects order book S$15.8m.

Deck Equipment (IOE): Lumpy revenue recognition ~S$12.5m order book extending to FY2028.

Corrosion Prevention: S$3.09m revenue (&darr 9.1% YoY, &darr 20.9% QoQ) steady demand from Singapore & Batam shipyards.

🧭 CEO Commentary (Yong Jiunn Run)

Performance reflects

work mix, not demand weakness.

FPSO remains the

anchor business, providing repeat work.

Proposed

acquisition of remaining ASOM stake to fully consolidate FPSO operations under BKM.

Focus remains on

execution, cost discipline, and cash management.

Shareholders to vote on ASOM acquisition at

EGM in May 2026.

⚠ ️ Risks & Considerations

Margin pressure from shipbuilding mix could persist if FPSO contributions taper.

Lumpy deck equipment revenue may cause quarterly volatility.

Execution risk in Batam yard projects and FPSO lifecycle renewals (especially West Africa).

ASOM acquisition outcome at EGM will be pivotal for FPSO consolidation.

📌 Takeaway for Investors

BKM 1Q2026 shows resilience with revenue growth and recurring FPSO work anchoring operations, but profitability is sensitive to project mix. The

ASOM acquisition vote in May is a key catalyst - if approved, it strengthens FPSO dominance and stabilizes margins longer term.

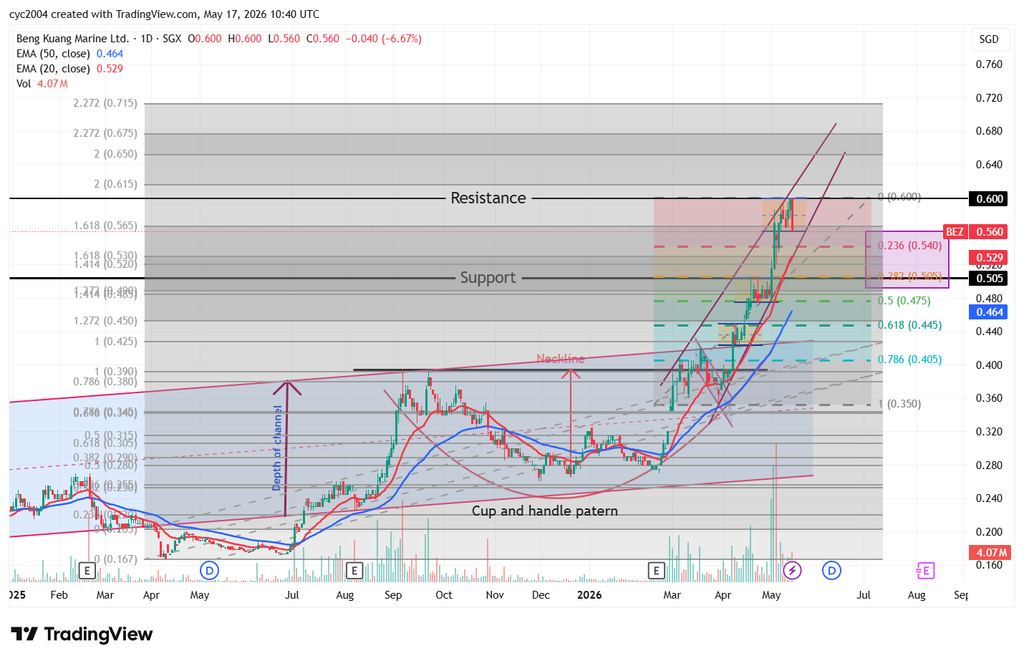

Picked up 15 lots at $0.485 today. The next test will be whether tonight press release can spark further upside in the share price.

JurongW ( Date: 21-Apr-2026 14:37) Posted:

The share price did not decline as feared following yesterday shooting star. It is now trading above yesterday candlestick at 49/49.5.

Support likely came from UOBKH new target price of 64 cents released today. The counter remains above the 5EMA, and I will monitor price action before deciding whether to reenter.

Together with L& T target of 53.5 cents, the average target price works out to ~59 cents.

|

|

The share price did not decline as feared following yesterday shooting star. It is now trading above yesterday candlestick at 49/49.5.

Support likely came from UOBKH new target price of 64 cents released today. The counter remains above the 5EMA, and I will monitor price action before deciding whether to reenter.

Together with L& T target of 53.5 cents, the average target price works out to ~59 cents.