Tuan Sing

Last:0.315

-

Tuan Sing Soaring Beyond $1

Post Reply

1-20 of 1120

Post Reply

1-20 of 1120

The Call to Divest GulTech at Tuan Sing&rsquo s AGM and the CEO' s Reply

Leong Chan Teik

04 May 2026

While Tuan Sing Holdings is recognised as a regional real estate group, one of its most valuable holdings is rooted in its 44.5% equity interest in Gul Technologies Singapore (GulTech), a printed circuit board (PCB) manufacturer.

Tuan Sing has a long association with GulTech which, at some point in the future, will be divested.

Tuan Sing' s CEO, William Liem, at the recent AGM said as much -- to no one' s surprise -- reiterating its position that GulTech is a non-core asset to be divested. Tuan Sing' s CEO, William Liem, at the recent AGM said as much -- to no one' s surprise -- reiterating its position that GulTech is a non-core asset to be divested.

" The asset is doing well, but of course, for us, it' s still a non-core asset. At some point, if we are able to, we would consider to divest and focus on real estate and as a result be able to deploy capital better," he said.

|

The Story of a Failed IPO

In 2021, it was announced that Gultech Jiangsu was exploring a potential IPO in China. Unfortunately it was eventually aborted.

Tuan Sing' s CEO acknowledged shareholder feedback regarding the need to unlock its value.

He assured investors that the board is " working hard" and actively exploring various strategic options to monetize this asset.

| Favourable condition |

" Today' s condition looks very favourable. And then we have all along been telling the market that this is a non-core investment... So now, taking advantage of this window, we quickly do a deal to divest off our stake so that we can bring down our debt meaningfully."

-- Shareholder at AGM |

" It' s been taking time, but I think at the end of the day, as you rightly pointed out, the markets are quite strong at this point in time for that particular asset, that asset class, and there' s a lot of interest in it. And we are, as a board, trying to explore different ways to monetize that," he said in reply to a shareholder.

GulTech caters to a diverse range of industries, including the automotive, computer peripheral, consumer electronics, and healthcare sectors.

It currently operates two plants in Suzhou, Wuxi and Jiangsu, and has just set up a fourth facility in Kedah, Malaysia.

| What valuation? |

" Based on GulTech&rsquo s current earnings profile, what valuation range does the board ascribe to this investment under different scenarios, and how does this compare with its carrying value on the balance sheet?."

-- SIAS' pre-AGM submitted question. Tuan Sing did not respond to the part about valuation range. |

GulTech' s Profitability and the PCB Market Boom

The timing for such a divestment could not be better, as GulTech is currently riding the wave of an industry upswing.

GulTech recorded a net profit of S$65.82 million on a 100% basis for FY 2025.

This success is underpinned by increased global demand for printed circuit boards.

Furthermore, the broader PCB market is experiencing a boom, largely driven by the growth of AI applications.

Financials of GulTech and its subsidiaries on a 100% are shown in the table below:

Year

|

Revenue (S$' 000)

|

Net Profit (S$' 000)

|

2022

|

624,931

|

62,086

|

2023

|

506,606

|

71,181

|

2024

|

430,495

|

59,032

|

2025

|

470,498

|

65,817

|

Source: Tuan Sing annual reports

|

A shareholder cited Victory Giant, which surged post-listing in April 2026 on HKSE, and trades at ~50X PE, a premium due to its PCB products targeting AI usage for AI clients, especially Nvidia.

Even if GulTech' s PE is, say, 20X, given its exposure is to automotive and other sectors, the valuation of S$1.3 billion translates to S$580 million attributable to Tuan Sing' s stake.

This alone is higher than Tuan Sing' s current market cap of S$412 million (stock price: 33 cents).

Currently, Tuan Sing' s equity interest in GulTech is carried on its balance sheet at S$177.69 million.

| Value of a Complete Divestment |

If Tuan Sing successfully executes a complete divestment of GulTech, the windfall could be transformative for the group.

Stock price

|

$0.33

|

52-week range

|

$0.23-$0.37

|

Market cap

|

S$412 m

|

PE (ttm)

|

11

|

Dividend yield

|

2.1%

|

P/B

|

0.34

|

Source: Yahoo!

|

Completely monetising this asset would bring immense value by allowing Tuan Sing to meaningfully pay down its S$1.39 billion in total borrowings.

Ultimately, it would also provide extra fuel for Tuan Sing' s real estate ambitions and enhance overall shareholder returns. |

Hmmmmm

linbei ( Date: 17-Apr-2026 08:15) Posted:

| War over . Everything back to normal |

|

War over . Everything back to normal

30c coming

Why are they not able to make money?

Assets getting revalued but they can' t extract profits from it? What' s the point of having those assets then? Sell them and realize the gains.

Tuan Sing FY2025 earnings up more than 12 times to $32.1m, proposes final dividend of 0.7 cents per share

The significant jump in net profit attributable to shareholders was due to the $51.2 million in value uplift across its Singapore and Australian portfolio.

The value uplift came from the completion of enhancement works at Dunearn Village in Singapore and revaluation of its Melbourne property at 121-131 Collins Street, which houses the 550-room Grand Hyatt Melbourne.

Earnings per share for FY2025 was 2.58 cents, as compared to 0.19 cents for FY2024.

However, revenue in FY2025 decreased by 24% y-o-y to $146.0 million, largely due to lower revenue contribution from real estate development and real estate investment segments, while partly offset by higher revenue from hospitality segment.

Tuan Sing&rsquo s total adjusted earnings before interest and tax (EBIT) were higher by 11% y-o-y to $45.3 million, driven by real estate development, hospitality and other investments segment, partially offset by lower adjusted EBIT from real estate investment segment.

Learn More

See also: IHH Healthcare' s FY2025 earnings down 21% on stronger ringgit

Tuan Sing&rsquo s board of directors has proposed an unchanged final dividend of 0.7 cents per share. The scrip dividend scheme will be applicable to this proposed dividend.

&ldquo The Group will stay focused on disciplined execution, strengthening recurring income streams, and pursuing value-accretive opportunities while maintaining a prudent balance sheet,&rdquo says William Liem, CEO of Tuan Sing.

This Is TUAN SING&rsquo s Catalyst: Associate GulTech' s Future IPO To Unlock Value

23 February 2026

A reader contributed this article

A compelling opportunity can be found in the " sum-of-the-parts" discount of Tuan Sing Holdings.

That opportunity: GulTech, a grossly undervalued associate in the booming printed circuit board industry.

A recent Tuan Sing corporate update reveals a massive valuation gap.

Source: Tuan Sing' s January 2026 corporate presentation Source: Tuan Sing' s January 2026 corporate presentation

The RMB1.83bn (&asymp S$327m) figure likely refers to the carrying value of Tuan Sing' s 44.5% stake in GulTech, rather than 100% of the company.

With GulTech' s profit on a 100% basis estimated at around S$60&ndash 70m per year, the implied trailing P/E at carrying value appears closer to 10&ndash 12× .

Even at this level, GulTech would still be trading at a meaningful discount to listed printed circuit board peers, which typically trade in the mid-teens to 30× range during a normal cycle.

|

GulTech Net Profit (100% basis)

Year

|

Net Profit

(S$$ ' 000)

|

Revenue

(S$' 000)

|

YoY Change

(Net Profit)

|

FY2024

|

59,032

|

430,495

|

-17%

|

FY2023

|

71,181

|

506,606

|

&mdash

|

Source: annual report

Tuan Sing Group

Year

|

Profit Attributable to Shareholders

(S $$' 000)

|

FY2024

|

2,344

|

FY2023

|

4,836

|

Understanding Tuan Sing

To appreciate the GulTech story, one must first look at the conglomerate that holds it.

Tuan Sing Holdings is no longer just a " property player" it is a diversified regional investment holding company with operations across four pillars:

&bull Real Estate Investment & Development: The bedrock of the company, featuring premium Singapore assets like 18 Robinson and Link@896, alongside a massive township project, Opus Bay in Batam.

&bull Hospitality: A growing segment including the Grand Hyatt Melbourne and the newly acquired Fraser Residence River Promenade in Singapore.

&bull Industrial & Other Investments: This is where GulTech (44.5% stake) resides.

For years, it was viewed as a non-core legacy holding, but today it has become the group' s hidden gem. |

GulTech: Prepping for IPO

Founded in 1988, it was actually listed on the SGX Mainboard until 2013, when Tuan Sing and its partners took it private.

In 2021, Tuan Sing sold a 13% stake to high-profile Chinese private equity firms (Yonghua Capital and Wens Capital) at a valuation of ~S$685 million.

This was a clear signal: GulTech was being groomed for a re-listing.

While a China IPO in 2023/2024 was assessed to be not favourable, the business has only grown stronger since.

Assuming GulTech generates annual net profit of approximately S$60&ndash 70m (does not factor in future growth yet) and is valued at 25× earnings at IPO, the implied equity value would be around S$1.5&ndash 1.75bn.

Tuan Sing' s 44.5% stake would therefore be worth roughly S$670&ndash 780m, compared with the current carrying value of about S$327m.

This implies a revaluation gain of approximately S$340&ndash 450m at the associate level.

Spread across Tuan Sing' s 1.25bn shares, this translates into an estimated NAV uplift of about 27&ndash 36 cents per share, which would be highly material relative to the current share price and highlights the significance of GulTech as a potential value-unlocking catalyst.

The global Printed Circuit Board market has been in a solid recovery and growth phase since late 2024, accelerating in 2025 and carrying strong momentum into 2026 &mdash largely thanks to the AI boom, EV/automotive electronics, and 5G/infrastructure demand.

GulTech is a top-tier manufacturer of printed circuit boards &mdash the fundamental " nerve system" of modern electronics.

They specialize in high-reliability boards for:

-

Automotive: Engine controls and telematics.

-

Data Storage: SSDs and networking modules.

-

Healthcare: Infusion pumps and glucose monitors.

The growth of AI is driving a sustained increase in demand for data storage, as AI systems require large datasets, frequent data access, and reliable long-term storage.

This, in turn, supports demand for enterprise-grade storage hardware such as SSDs and storage systems, which rely on more complex and reliable printed circuit boards.

GulTech' s exposure to data-storage and infrastructure-related printed circuit boards positions it to benefit from this trend, helping to underpin more stable and resilient earnings over time, even if growth is gradual rather than abrupt.

| Potential NAV uplit of 27-36 cents/share |

Even applying a modest 25x multiple to GulTech&rsquo s earnings implies an equity value of S$670 m &ndash 780 m attributable to Tuan Sing shareholders.

Stock price

|

$0.35

|

52-week range

|

$0.21-$0.36

|

Market cap

|

S$431 m

|

PE (ttm)

|

18

|

Dividend yield

|

2%

|

P/B

|

0.36

|

Source: Yahoo!

|

This translates into a potential NAV uplift of S$0.27&ndash 0.36 per share.

When you consider Tuan Sing&rsquo s current share price is roughly S$0.35, the " hidden" value in the GulTech stake alone is worth almost the entire market cap of the company today.

There is a " China+1" bonus: GulTech is building a new plant in Malaysia, diversifying its supply chain away from China risks&mdash a move that usually attracts a significant valuation premium in today&rsquo s market.

While execution, timing, and discount risks remain, the valuation gap is sufficiently wide that any IPO or partial divestment of GulTech would be a meaningful and quantifiable NAV catalyst, not a weak one.

|

Unusual break out today.

Hit 375 so far oh oh

sengkang ( Date: 28-Jan-2026 17:51) Posted:

Today hit 360, same as the recent high of 360 on 28-10-2025.

Volume traded 3.088m shares |

|

Today hit 360, same as the recent high of 360 on 28-10-2025.

Volume traded 3.088m shares

I think better let DBS digest Gul Tech numbers instead.

superstartup ( Date: 20-Jan-2026 11:56) Posted:

Adding slowly over here again.

|

|

Adding slowly over here again.

Let' s have Gul Tech listing.

superstartup ( Date: 13-Jan-2026 17:50) Posted:

Tuan Sing Management finally woke up.

Today provided a corporate update presentation slides. 1st time in many years, if not in history.

From today slides, page 16, for easy reference:

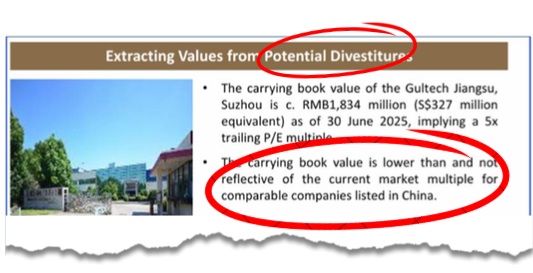

" Extracting Values from Potential Divestitures

- The carrying book value of the Gultech Jiangsu, Suzhou is c. RMB1,834 million (S$327 million equivalent) as of 30 June 2025, implying a 5x trailing P/E multiple.

- The carrying book value is lower than and not reflective of the current market multiple for comparable companies listed in China."

From today slides, page 45, for easy reference:

" - As part of its China + 1 strategy, Gultech is expanding outside of China a third plant at the Kulim Hi-Tech Park in Kedah Malaysia is under construction and is expected to be operational in 2026.

- In line with our focus on the real estate business, the Group is not averse to considering options and opportunities to divest, develop, streamline, restructure and/or reorganise its non-real estate investment and business when opportunities arise with the view to potential value maximization."

Did a quick check on DBS past comment, dated 5 May 2021 on Tuan Sing Gul Tech' s Peers:

" .... GulTech' s peers in China are however trading at a historical P/E of between 20x and 43x (average 29x) ...."

[ As usual, please perform your own DD ]

superstartup ( Date: 13-Jan-2026 16:44) Posted:

China Techs real hot now.

Not sure how much is Gul Tech valuation now |

|

|

|

Based on the latest slides, Gultech is currently carried at ~RMB1.83bn (&asymp S$327m), implying a very low ~5x trailing P/E. If we reverse-engineer this, Gultech is earning ~RMB367m, and applying even a conservative listed-peer multiple of 15&ndash 20x (vs China peers historically at 20&ndash 40x) would value Gultech at ~RMB5.5&ndash 7.3bn (&asymp S$1.0&ndash 1.3bn). That implies a revaluation uplift of ~S$660&ndash 980m over book value. Spread across ~1.25bn Tuan Sing shares, this translates to roughly S$0.53&ndash 0.78 per share of potential value uplift, versus the current share price of around S$0.33. Even after allowing for execution risk and discounts, the gap between Gultech&rsquo s carrying value and market-comparable multiples is clearly material and explains why any IPO or divestment could be a meaningful NAV catalyst.

Many thanks for uploading the updates'

superstartup ( Date: 13-Jan-2026 17:50) Posted:

Tuan Sing Management finally woke up.

Today provided a corporate update presentation slides. 1st time in many years, if not in history.

From today slides, page 16, for easy reference:

" Extracting Values from Potential Divestitures

- The carrying book value of the Gultech Jiangsu, Suzhou is c. RMB1,834 million (S$327 million equivalent) as of 30 June 2025, implying a 5x trailing P/E multiple.

- The carrying book value is lower than and not reflective of the current market multiple for comparable companies listed in China."

From today slides, page 45, for easy reference:

" - As part of its China + 1 strategy, Gultech is expanding outside of China a third plant at the Kulim Hi-Tech Park in Kedah Malaysia is under construction and is expected to be operational in 2026.

- In line with our focus on the real estate business, the Group is not averse to considering options and opportunities to divest, develop, streamline, restructure and/or reorganise its non-real estate investment and business when opportunities arise with the view to potential value maximization."

Did a quick check on DBS past comment, dated 5 May 2021 on Tuan Sing Gul Tech' s Peers:

" .... GulTech' s peers in China are however trading at a historical P/E of between 20x and 43x (average 29x) ...."

[ As usual, please perform your own DD ]

superstartup ( Date: 13-Jan-2026 16:44) Posted:

China Techs real hot now.

Not sure how much is Gul Tech valuation now |

|

|

|

Tuan Sing Management finally woke up.

Today provided a corporate update presentation slides. 1st time in many years, if not in history.

From today slides, page 16, for easy reference:

" Extracting Values from Potential Divestitures

- The carrying book value of the Gultech Jiangsu, Suzhou is c. RMB1,834 million (S$327 million equivalent) as of 30 June 2025, implying a 5x trailing P/E multiple.

- The carrying book value is lower than and not reflective of the current market multiple for comparable companies listed in China."

From today slides, page 45, for easy reference:

" - As part of its China + 1 strategy, Gultech is expanding outside of China a third plant at the Kulim Hi-Tech Park in Kedah Malaysia is under construction and is expected to be operational in 2026.

- In line with our focus on the real estate business, the Group is not averse to considering options and opportunities to divest, develop, streamline, restructure and/or reorganise its non-real estate investment and business when opportunities arise with the view to potential value maximization."

Did a quick check on DBS past comment, dated 5 May 2021 on Tuan Sing Gul Tech' s Peers:

" .... GulTech' s peers in China are however trading at a historical P/E of between 20x and 43x (average 29x) ...."

[ As usual, please perform your own DD ]superstartup ( Date: 13-Jan-2026 16:44) Posted:

China Techs real hot now.

Not sure how much is Gul Tech valuation now.

superstartup ( Date: 13-Jan-2026 14:02) Posted:

Tuan Sing now relative Low Base compared to the general market.

On watch for any corporate news while slowly accumulate. |

|

|

|

China Techs real hot now.

Not sure how much is Gul Tech valuation now.

superstartup ( Date: 13-Jan-2026 14:02) Posted:

Tuan Sing now relative Low Base compared to the general market.

On watch for any corporate news while slowly accumulate. |

|

Hopefully today Company Share BuyBack.

Tuan Sing now relative Low Base compared to the general market.

On watch for any corporate news while slowly accumulate.

Tuan Sing secures permit to redevelop flagship Melbourne property with Grand Hyatt hotel asset

The works are planned to commence in early 2026

[SINGAPORE] Tuan Sing : T24 -1.54% is set to proceed with the redevelopment of its flagship property at 121 to 131 Collins Street in Melbourne, Australia, following the grant of a planning permit from the city council.

The real estate investment group on Wednesday (Dec 3) announced that it had received the official permit for the site, which houses the 550-room Grand Hyatt hotel and various retail spaces.

The approval follows the town planning application submitted by Grand Hotel Group, a wholly owned subsidiary of Tuan Sing, last November.

With the regulatory green light, the group intends to commence redevelopment works early next year.

The revamp will introduce a &ldquo luxury retail podium spanning over three levels and featuring flagship duplexes&rdquo .

A major portion of the plan also involves revitalising the property&rsquo s facade to enhance the streetscape and boost engagement.

Tuan Sing said in a press release: &ldquo Through adaptive reuse and sustainable design, the project aims to inject new energy into the precinct while ensuring &lsquo business as usual&rsquo for the hotel and existing tenants throughout construction.&rdquo

William Liem, the group&rsquo s chief executive officer, noted that the project represents &ldquo re-imagining rather than rebuilding&rdquo and embraces an inherently sustainable path.

Redeveloping &ldquo one of the most iconic buildings in Melbourne into a high-value, mixed-use asset&rdquo will enhance the city&rsquo s urban landscape and deliver long-term returns for stakeholders, he added.

Tuan Sing plans to fund the project using a combination of bank financing and internal resources. Upon completion, the revitalised property is expected to command higher face rents, boost cash flow and obtain a stronger valuation, the company said.