Post Reply

10161-10180 of 10239

Post Reply

10161-10180 of 10239

Just realised NAV per share can decrease if market price of div scrip share is lower than the NAV per share. This means a DRP is good for all parties only if market price is generally higher than NAV per share. We will have to wait a long time for that for YZJFH. 😆

GoldenPig ( Date: 02-Oct-2022 09:52) Posted:

On further thought, yes, a DRP will have dilution effect in that the number of public shares will increase. But the NAV per share would be about the same, right? So no dilution of ownership by shareholders?

GoldenPig ( Date: 02-Oct-2022 08:53) Posted:

DRP should not have a dilution effect as cash that would be distributed as dividends is retained by the company. It is equivalent to an injection of capital into the company, without incurring fund-raising cost.

But as price of div scrip shares is pegged to market price, it would be more beneficial to use treasury shares for a DRP when market price of its shares is much much higher. |

|

|

|

On further thought, yes, a DRP will have dilution effect in that the number of public shares will increase. But the NAV per share would be about the same, right? So no dilution of ownership by shareholders?

GoldenPig ( Date: 02-Oct-2022 08:53) Posted:

DRP should not have a dilution effect as cash that would be distributed as dividends is retained by the company. It is equivalent to an injection of capital into the company, without incurring fund-raising cost.

But as price of div scrip shares is pegged to market price, it would be more beneficial to use treasury shares for a DRP when market price of its shares is much much higher.

volvo125 ( Date: 02-Oct-2022 02:17) Posted:

Yes ... that could be an option to deploy the Treasury shares but this DRP plan will have dilution effect becuase unlike M& A or investment projects, public sharesholders do not produce revenue and income streams to neutralise the dilution effect due to the re-admission of shares back into the float.

YFH immediate challenge is not so much on how or what or when to deploy the Treasury shares to maximize mileage. Cancellation ( in part ) could emerge down the road as an unavoidable option (due to SGX 10% limit) if the capital flights situatuion has gotten so severe and protracted that the full 395m could not adquately sort out all the huge excess shares dumped by the Angmoh funds that are haunting YFH share price |

|

|

|

DRP should not have a dilution effect as cash that would be distributed as dividends is retained by the company. It is equivalent to an injection of capital into the company, without incurring fund-raising cost.

But as price of div scrip shares is pegged to market price, it would be more beneficial to use treasury shares for a DRP when market price of its shares is much much higher.

volvo125 ( Date: 02-Oct-2022 02:17) Posted:

Yes ... that could be an option to deploy the Treasury shares but this DRP plan will have dilution effect becuase unlike M& A or investment projects, public sharesholders do not produce revenue and income streams to neutralise the dilution effect due to the re-admission of shares back into the float.

YFH immediate challenge is not so much on how or what or when to deploy the Treasury shares to maximize mileage. Cancellation ( in part ) could emerge down the road as an unavoidable option (due to SGX 10% limit) if the capital flights situatuion has gotten so severe and protracted that the full 395m could not adquately sort out all the huge excess shares dumped by the Angmoh funds that are haunting YFH share price.

GoldenPig ( Date: 01-Oct-2022 21:47) Posted:

| Besides share cancellation, another good use of buyback shares is to start a Dividend Reinvestment Plan. Company can issue buyback shares to investors who opt for the DRP. Should be a win-win-win situation for the company, for investors who opt for div shares and for investors who opt for cash div. |

|

|

|

Yes ... that could be an option to deploy the Treasury shares but this DRP plan will have dilution effect becuase unlike M& A or investment projects, public sharesholders do not produce revenue and income streams to neutralise the dilution effect due to the re-admission of shares back into the float.

YFH immediate challenge is not so much on how or what or when to deploy the Treasury shares to maximize mileage. Cancellation ( in part ) could emerge down the road as an unavoidable option (due to SGX 10% limit) if the capital flights situatuion has gotten so severe and protracted that the full 395m could not adquately sort out all the huge excess shares dumped by the Angmoh funds that are haunting YFH share price.

GoldenPig ( Date: 01-Oct-2022 21:47) Posted:

| Besides share cancellation, another good use of buyback shares is to start a Dividend Reinvestment Plan. Company can issue buyback shares to investors who opt for the DRP. Should be a win-win-win situation for the company, for investors who opt for div shares and for investors who opt for cash div. |

|

Greeting to you too, @pastime. EPS (earning per share) and DPS (dividend per share) will increase accordingly to the amount of shares being purchased and put back into the Treasury, regardless if these shares continue to remain lock-up in the treasury for future deployment or they are being cancelled in part or in full. However, cancellation of the Treasury shares will permanently eliminate the shares from the float and hence guarrantee a permanent one off sustained EPS and DPS increase.

The indicative FY22 $220m npat (net profit after tax) will give a dps of 0.022, with a boost to 0.025 (round off) with the SBB 395m max fully implemented regardless if the Treasury shares are being cancelled or not. If YFH get back to the previous steady state $340m npat by FY23 (or may be FY24) as projected by cimb, the boosted dps will hit 0.038.

Based on the latest SBB filing last Friday with 206m or 5.2% now locked up in the Treasury, the indicative FY22 $220m npat will give out a minimum boosted DPS of ~0.024 (round off), meaning shareholders will get 5.2% more dividend.

Under normal circumstances, I do not think Listco will go the cancellation path because Treasury shares are almost equivalent to liquid hard cash at market values that could be used to fund strategic projects and investments on a major basis or employee benefits on a minor basis .... etc. The redeployment of Treasury shares for future attractive M& A may not necessarily lead to dilution because such strategically appraised M& A projects will highly likely have their own revenues and incomes streams that should match the overall target ROE objectives.

In YFH case, Treasury shares cancellation may likely happen ( at least in part(s) in order to overcome the SGX 10% limit and restore a new SBB mandate to continue the mopping ) if the 1st SBB 395m could not adequately sort out the huge amount of excess shares if Vanguard and Blackrock are also exiting. The capital flights situations are very real now globally due to the significant and continuous appreciation of USD in a rising rates environment. USD are frantically flighting back to the USA.

pasttime ( Date: 01-Oct-2022 18:07) Posted:

volvo125, greetings. good thinking and write up.

if the buy back shares do get cancelled out it will also meant the dividend pay out to remaining shares is higher for the same earning and same 40% payout.

have a good week end. |

|

I will stick to my plan for the time being. No further buying till 1st FY unless the price revisit 35 cents, then I may pick up a bit more.

HVRRVH ( Date: 22-Sep-2022 14:14) Posted:

| Reluctantly added a while ago @ 39 cents, counter party ABN. They have been my counter party almost all my purchased shares at 36.5, 37.5 and 38.5 cents! Really so many shares they are holding?? Whatever, my stage 1 operation completed with intended position size fulfilled. Next stage will be after the 1st FY results. |

|

Besides share cancellation, another good use of buyback shares is to start a Dividend Reinvestment Plan. Company can issue buyback shares to investors who opt for the DRP. Should be a win-win-win situation for the company, for investors who opt for div shares and for investors who opt for cash div.

Volvo 125

volvo125 ( Date: 30-Sep-2022 14:48) Posted:

I believe many Long investors are beginning to harbour rising doubts if the current SBB mandate can indeed sort out the deep excesses and ultimately lift the price up to a more reasonable level, especially now when even after 202m SBB and yet the price is still being badly suppressed at 0.37. It is still too early to tell until the TR 295m are progressively and could be fully absorbed in the weeks ahead, and then a further 100m till the 395m max to see the full effect. We just have to be patience to see how the situation will roll out.

The current SBB mandate still has 193m to go until 395m max. Mopping up a further 193m from the market is a big deal (Yes, big deal as it will cost ~$75~80m instant hard cash) to take out the severe excesses that are still haunting YFH due to TR exit dumping. 395m is 100m more than TR 295m estimated dumping so we should really likely see the excess condition to improve significantly or even sorted out and hence the share price should improve too ... unless the Capital Flight situation is also happening to the other 2 big Angmoh funds (Vanguard 93m and Blackrock 32m dated 31 Aug 2022 as shown in Simplywall.st) due to USD appreciation as a result of the ongoing continuous steep rate hikes. In view of the past few days severe and persistent selldown happening yet again, I' m not surprised Vanguard and Blackrock are also selling off to bring the USD back to US.

Meanwhile, Long shareholders should know that the current SBB will benefit them handsomely in the long term as the coy is paying only ~0.40 to buy back a 1.07 asset and reaping a 167% ROE on this SBB exercise. EPS and DPS will improve accordingly to the amount of shares being eliminated from the market (which is now ~5% at 202m).

In case you are also wondering where this 167% ROE came from in the SBB .... assuming the ave price to SBB all the 395m (1.07nav) at 0.40 ave purchased price, so 1.07 minus 0.4 = 0.67 gain, 0.67/0.4 = 167%. Yfh steady state ROE in the past 3 years before spin off were 8~8.5% pa. This SBB reaps a stunning 167% ROE. .... where to find such good arbitrage deal ?

A final point to note here is under SGX ruling, treasury has a limit at 10% of the float. If, in the worst scenario at 395m max and yet the excess shares in the market are still severe and the price still being deeply suppressed (eg, Vanguard or Blackrock or both were also exiting), I would believe YFH under Uncle Ren chairmanship will highly likely take the step to cancel part or fully the treasury shares held and then call a EGM (or in the coming FY23 AGM) to authorise a 2nd SBB. YFH is ultra cash rich and CIMB expected YFH to have ~sgd1.9b cash by end 2022 from the maturing DI, so calling a 2nd SBB is really not a issue to YFH provided the 10% cap is satisfied.

Example, YFH could choose to cancel in part, such as 100m of the 395m treasury shares. The new total float including treasury shares will be 3.950b minus 100m = 3.850b. The new 10% cap would be 385m. YFH treasury now only left 295m in the treasury after the 100m cancellation. YFH can then continue to SBB a further 90m shares (385m max minus 295m existing treasury). Repeat again when the 90m is used up.

Cancellation of treasury shares has financial and accounting implications. YFH can deploy treasury shares at market value for strategic corporate actions such as M& A (mergers & acquisitions) ..etc to expand the coy portfolio revenues and income streams in the future, and cancellation of treasury shares in parts or in full will deny YFH this option in part or in full. This denied option, I believe, is a con to the coy.

Cancellation of Treasury shares will see a reduction in YFH net asset accordingly due to a reduction in the float. However in YFH case, the NAV per share will increase noticeably because YFH is buying back shares at ultra steep discount ~0.40. Assuming YFH SBB all the 395m at 0.4 ave, the total cost of purchase will be ~$158m. Assuming YFH opted to fully retired the whole 395m for example, the balance sheet net effect will see a giant realised gain when both the 395m shares and the cost of purchase ($158m) are eliminated. The current net asset is 1.07*3950 = $4.226b. The new net asset would be $4.226 minus $158m = $4.069b. The new float will be 3950 minus 395 = 3555m. The NAV per share will increase to 4069/3555 = 1.145 (from 1.07 now). Long sharesholders will benefit tremendously from this significant one time permanent NAV appreciation, EPS and DPS permanent increase, and a permanent elimination of the 395m from the market.

This is my reading on Yfh going forward .... any CPA (certified public accountant) may wish to correct me on the accounting implications that i cited. Else please ignore this post if you think I' m talking nonsense.

|

|

I believe treasury shares are not entitled to dividends. So payout to each remaining share will increase even if the buyback shares are not cancelled. That' s why share buyback is good for investors. 😊

An interesting point volvo125 highlighted is that because the shares are bought back at such a big discount to NAV, cancelling the shares results in increased NAV per remaining share, due to a smaller reduction in net assets spread over a larger reduction in floating shares. That is a big leg up in compounding returns. Hope YZJFH does some share cancellations.

pasttime ( Date: 01-Oct-2022 18:07) Posted:

volvo125, greetings. good thinking and write up.

if the buy back shares do get cancelled out it will also meant the dividend pay out to remaining shares is higher for the same earning and same 40% payout.

have a good week end. |

|

volvo125, greetings. good thinking and write up.

if the buy back shares do get cancelled out it will also meant the dividend pay out to remaining shares is higher for the same earning and same 40% payout.

have a good week end.

I believe many Long investors are beginning to harbour rising doubts if the current SBB mandate can indeed sort out the deep excesses and ultimately lift the price up to a more reasonable level, especially now when even after 202m SBB and yet the price is still being badly suppressed at 0.37. It is still too early to tell until the TR 295m are progressively and could be fully absorbed in the weeks ahead, and then a further 100m till the 395m max to see the full effect. We just have to be patience to see how the situation will roll out.

The current SBB mandate still has 193m to go until 395m max. Mopping up a further 193m from the market is a big deal (Yes, big deal as it will cost ~$75~80m instant hard cash) to take out the severe excesses that are still haunting YFH due to TR exit dumping. 395m is 100m more than TR 295m estimated dumping so we should really likely see the excess condition to improve significantly or even sorted out and hence the share price should improve too ... unless the Capital Flight situation is also happening to the other 2 big Angmoh funds (Vanguard 93m and Blackrock 32m dated 31 Aug 2022 as shown in Simplywall.st) due to USD appreciation as a result of the ongoing continuous steep rate hikes. In view of the past few days severe and persistent selldown happening yet again, I' m not surprised Vanguard and Blackrock are also selling off to bring the USD back to US.

Meanwhile, Long shareholders should know that the current SBB will benefit them handsomely in the long term as the coy is paying only ~0.40 to buy back a 1.07 asset and reaping a 167% ROE on this SBB exercise. EPS and DPS will improve accordingly to the amount of shares being eliminated from the market (which is now ~5% at 202m).

In case you are also wondering where this 167% ROE came from in the SBB .... assuming the ave price to SBB all the 395m (1.07nav) at 0.40 ave purchased price, so 1.07 minus 0.4 = 0.67 gain, 0.67/0.4 = 167%. Yfh steady state ROE in the past 3 years before spin off were 8~8.5% pa. This SBB reaps a stunning 167% ROE. .... where to find such good arbitrage deal ?

A final point to note here is under SGX ruling, treasury has a limit at 10% of the float. If, in the worst scenario at 395m max and yet the excess shares in the market are still severe and the price still being deeply suppressed (eg, Vanguard or Blackrock or both were also exiting), I would believe YFH under Uncle Ren chairmanship will highly likely take the step to cancel part or fully the treasury shares held and then call a EGM (or in the coming FY23 AGM) to authorise a 2nd SBB. YFH is ultra cash rich and CIMB expected YFH to have ~sgd1.9b cash by end 2022 from the maturing DI, so calling a 2nd SBB is really not a issue to YFH provided the 10% cap is satisfied.

Example, YFH could choose to cancel in part, such as 100m of the 395m treasury shares. The new total float including treasury shares will be 3.950b minus 100m = 3.850b. The new 10% cap would be 385m. YFH treasury now only left 295m in the treasury after the 100m cancellation. YFH can then continue to SBB a further 90m shares (385m max minus 295m existing treasury). Repeat again when the 90m is used up.

Cancellation of treasury shares has financial and accounting implications. YFH can deploy treasury shares at market value for strategic corporate actions such as M& A (mergers & acquisitions) ..etc to expand the coy portfolio revenues and income streams in the future, and cancellation of treasury shares in parts or in full will deny YFH this option in part or in full. This denied option, I believe, is a con to the coy.

Cancellation of Treasury shares will see a reduction in YFH net asset accordingly due to a reduction in the float. However in YFH case, the NAV per share will increase noticeably because YFH is buying back shares at ultra steep discount ~0.40. Assuming YFH SBB all the 395m at 0.4 ave, the total cost of purchase will be ~$158m. Assuming YFH opted to fully retired the whole 395m for example, the balance sheet net effect will see a giant realised gain when both the 395m shares and the cost of purchase ($158m) are eliminated. The current net asset is 1.07*3950 = $4.226b. The new net asset would be $4.226 minus $158m = $4.069b. The new float will be 3950 minus 395 = 3555m. The NAV per share will increase to 4069/3555 = 1.145 (from 1.07 now). Long sharesholders will benefit tremendously from this significant one time permanent NAV appreciation, EPS and DPS permanent increase, and a permanent elimination of the 395m from the market.

This is my reading on Yfh going forward .... any CPA (certified public accountant) may wish to correct me on the accounting implications that i cited. Else please ignore this post if you think I' m talking nonsense.

BB same old trick. Cannot clear 405 drop back...

HVRRVH ( Date: 23-Sep-2022 11:54) Posted:

| Same old same old, from the technical point of view, encountered resistance at 41/41.5. It fell below 40 cents promptly exactly 2 Monday ago after touching 40.5 cents. Since then, it has trend sideway and slowly inching up while global equities market took a tumber. Strong move in weak market. Let' s see if this is the sign that it wants to say good bye to below 40 cents. |

|

Same old same old, from the technical point of view, encountered resistance at 41/41.5. It fell below 40 cents promptly exactly 2 Monday ago after touching 40.5 cents. Since then, it has trend sideway and slowly inching up while global equities market took a tumber. Strong move in weak market. Let' s see if this is the sign that it wants to say good bye to below 40 cents.

B/ Millionaires can make use of this opportunity to buy up too...

Rocket just started....

The big wave up!

Jandec ( Date: 20-Sep-2022 21:08) Posted:

| Great info on the buyback. Longists got in because they can see potential in a stock, no worries as this company is not saddled with debt, the management and staff looks great - ready to make a killing in this market. Where there is volatility, opportunity abounds for the informed. I feel like I am investing in an investment bank start up with an impressive line up. Shortists always have to keep on their toes - its' bad for health - as the tide changes without warning and one can get swept away with no rescue. But for longists I think the safety is in waiting. Price has settled at a low level for the stock to be extremely attractive for nibbling. |

|

Can break 405 convincingly this time and stay at 4 series?....

Reluctantly added a while ago @ 39 cents, counter party ABN. They have been my counter party almost all my purchased shares at 36.5, 37.5 and 38.5 cents! Really so many shares they are holding?? Whatever, my stage 1 operation completed with intended position size fulfilled. Next stage will be after the 1st FY results.

The Independent Diretor, Mr Chew has just added another 188,000 shares and brought his total holding to 888,000 shares. Well, it has been a while and this move signify that he felt the share price is undervalued. I expect more buy back by company' s insiders if the price continue to stay at this level. After all, they have started buying since around 57 cents.

Jandec ( Date: 20-Sep-2022 21:08) Posted:

| Great info on the buyback. Longists got in because they can see potential in a stock, no worries as this company is not saddled with debt, the management and staff looks great - ready to make a killing in this market. Where there is volatility, opportunity abounds for the informed. I feel like I am investing in an investment bank start up with an impressive line up. Shortists always have to keep on their toes - its' bad for health - as the tide changes without warning and one can get swept away with no rescue. But for longists I think the safety is in waiting. Price has settled at a low level for the stock to be extremely attractive for nibbling. |

|

Great info on the buyback. Longists got in because they can see potential in a stock, no worries as this company is not saddled with debt, the management and staff looks great - ready to make a killing in this market. Where there is volatility, opportunity abounds for the informed. I feel like I am investing in an investment bank start up with an impressive line up. Shortists always have to keep on their toes - its' bad for health - as the tide changes without warning and one can get swept away with no rescue. But for longists I think the safety is in waiting. Price has settled at a low level for the stock to be extremely attractive for nibbling.

Written by The NextInsight Team

Published: 17 September 2022

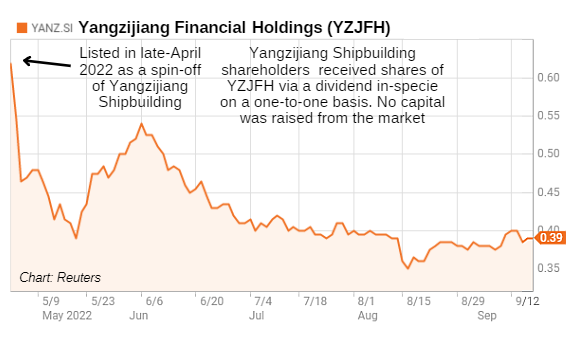

Going into its sixth month as a listed entity, Yangzijiang Financial, as the chart shows, hasn' t won many investors over.

And this is despite some strong buybacks that the company has done:

Announcement date

|

Amount of shares

|

Total value (S$)

|

Average price (S$)

|

| |

June 9, 2022

|

1,000,000

|

510,491.13

|

0.51

|

June 10, 2022

|

1,500,000

|

748,219.84

|

0.5

|

June 13, 2022

|

1,800,000

|

873,840.71

|

0.49

|

June 14, 2022

|

1,000,000

|

482,964.65

|

0.48

|

June 23, 2022

|

2,000,000

|

870,837.84

|

0.44

|

July 6, 2022

|

2,000,000

|

800,770.40

|

0.4

|

August 12, 2022

|

4,037,300

|

1,552,544.64

|

0.38

|

August 17, 2022

|

6,000,000

|

2,172,289.91

|

0.36

|

August 22, 2022

|

2,000,000

|

750,722.25

|

0.38

|

August 23, 2022

|

3,907,400

|

1,476,072.85

|

0.38

|

August 24, 2022

|

463,300

|

178,542.28

|

0.39

|

September 5, 2022

|

3,000,000

|

1,150,106.50

|

0.38

|

September 6, 2022

|

8,527,100

|

3,241,447.54

|

0.38

|

| |

37,235,100

|

14,808,850.54

|

0.40

|

*including stamp duties and clearing charges

|

Ren Yuanlin, executive chairman of Yangzijiang Financial.

Ren Yuanlin, executive chairman of Yangzijiang Financial.

NextInsight file photoThere' s more firepower that Yangzijiang Financial will unleash, given that it has announced a share buyback program of up to S$200 million, which is certainly a signal of confidence.

There were shareholder questions around it and the dividend policy in a filing on the SGX a fortnight ago. Yangzijiang Financial also outlined its investment strategies.

Q: Has the Group allocated SGD200 million of funds for share buyback or is it still subjected to the company&rsquo s future plans?

A: The Group has allocated up to SGD200 million of capital for share buyback and has almost one year to do so. The Group will continue to execute share buyback strategies to enhance shareholder value. The amount of capital allocated for share buyback had taken into consideration the near-term investment needs of the Group.

Q: What is the Group&rsquo s dividend policy?

The Group has a dividend policy of paying out at least 40% of its profits as dividends. The Group will continue to seek to maintain an attractive dividend yield as compared to what has been delivered prior to the spinoff, striking a balance between dividend pay-out and capital growth.

Q: With more investment in PE, equity etc., how does it affect the Group&rsquo s liquidity to pay dividends?

Dividends will be paid out via cash flows generated from interest income, dividend distributions, and exits from investee companies.

For more on the company, check out analyst reports:

Key highlights from the CIMB initiation report:

&bull 0.4x P/B

&bull Pledged to pay out 40% of net profits as dividends (> 4% projected dividend yield)

&bull Targets to double AUM to S$7bn in 3-5 years (YZJFH&rsquo s current AUM is S$4.76bn- CIMB&rsquo s estimate)

&bull YZJFH&rsquo s current market cap is trading below CIMB&rsquo s estimate of c.S$1.8bn of cash by end-FY22 (S$0.46/share)

|

CIMB believes YZJFH can utilise its strong Chinese network to capture China&rsquo s growing wealth management market. Together with the newly acquired asset management firm, GEM Asset Management (GEM), CIMB thinks the group can replicate its success outside China with existing ammunition and by leveraging third-party money to grow its AUM.