Post Reply

12481-12500 of 12508

Post Reply

12481-12500 of 12508

3Q2014 results out soon

Gold price is down but this counter is holding up....

Very optimistic. I expect only 9k oz for Q3. Their production might be lumpy and I only conservatively assume 2k oz for July and August. However, based on 2013 results, monsoon appears to affect them on Q1 instead of Q4. So I assume similar production of 9k oz for Q4 also, supported by their new crusher. Having turned net cash last quarter, hopefully shareholders can get rewarded with decent dividend.

Sep gold production was about 5200 oz. June production was about 4300 oz. Assuming Jul and Aug production were 4300 oz per month. estimated gold production for Q3 is 13,800 oz. Q2 all in cost was $649. Assuming ave gold selling price is $1200. Profit will be US$550 per oz. 13800 x 550 = US$7.59M. This is higher than 1st half profit after tax which was at US$7.05M.

vested. Q4 production will be affected by the monsoon season. So, assume 50% production yield of Q3, Q4 probably at 7000 oz. 7000 x 550 = US$3.8M Estimated current year profit after tax = 7.05 + 7.59 + 3.8 = US$18.4M or 4.5 UScents or PE ration of 6.2 (based on 28 cents). Dividend policy (i thought the CEO mentioned before) is 30% profit, which is 1.35 US cents.

Just a simple calculation. anyway, I' m vested.

Vested. Looking forward to a stunning set of results and PER to drop below 5.

anyone vested here?

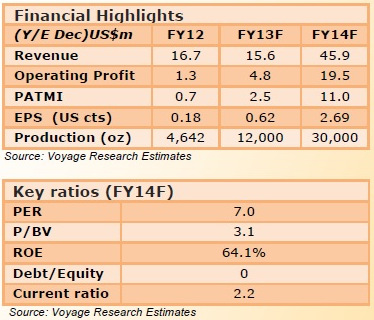

Voyage Research pegs CNMC Goldmine' s intrinsic value at 84 cents

Analyst: Liu Jinshu

Chris Lim (standing), CEO of CNMC, with Peter Choo, vice-chairman of CNMC (seated).

NextInsight file photo.CNMC Goldmine Holdings Ltd reported a 254% increase in net profit after tax on revenue growth of 62% for 2QFY2014, compared with 1QFY2014.

The 1H results were largely in line with our expectations. In particular, profit after tax amounted to US$7.05 million ($8.81 million), of which cash generated from operations was US$6.39 million.

Essentially, CNMC' s production and profitability can be said to be " out of the woods" and no longer at risk of lapsing into periodic losses, as was the case during its first year of operations post-listing.

To reward shareholders, the company has further raised its interim dividend to 0.15 cents a share (1% annual yield), compared with 0.1 cent previously.

1HFY2014 net margin came in at 42.6% versus our estimate of 34.4%.

We maintain our forecasts and valuation in this report. Intrinsic value of 84 cents.

ozone2002 ( Date: 21-Jul-2014 09:58) Posted:

Last:0.295 Vol:184k  +0.005 +0.005

looks like they are ramping up production of goldbars.. gold price has been moving upwards as well

jcbull ( Date: 09-Jul-2014 19:02) Posted:

Sokor Gold Project produced 4,356.47 ounces of gold doré bars1 in the month of June 2014, which is the highest record todate for monthly output since the start of gold production in July 2010, surpassing its previous record of 3,419.51 ounces as reported in the Announcement, representing an increase of approximately

27.4%.

In line with the Company&rsquo s strategy of ramping up its gold production, the installation of a 350 tonnes per hour crushing system is currently in progress and near to completion. The Company expects to conduct trial runs of the crushing system in the third quarter of 2014.

Vested

|

|

|

|

Not to forget the extra $3-4M savings per annum of tax exemption savings..

4.3 CNMC to enjoy 5-year tax-exemption period

On 14 May 2014, CNMC received the Pioneer Certificate from the Malaysian Investment Development Authority (MIDA). Pioneer status entitles the Sokor

Gold Field Project to 100% income tax exemption on its statutory income for a period of five years from 1 Jul 2013 (retrospective) to 30 Jun 2018. The tax

benefit attributable to FY13 profit will be reflected in CNMC&rsquo s 2Q14 bottomline. Going forward, we estimate that CNMC will enjoy tax savings of US$3m-4m p.a.

This will have significant positive impact on CNMC&rsquo s bottomline.

June gold production is more than the entire Q1. Expect a suge in profit for Q2 and another surge for Q3 as the 3rd leach yard only commenced operation in the middle of Q2. Heavily overweighted.

result out on Monday morning. Expect to see a surge in profit due to (1) improved production from one month of 3rd leach operation (2) better weather as compare to Q1 which was a monsoon period (3) plough back of past tax paid now that they are tax exempted. (4) better All-in-cost due to higher economic of scale saving and tax exemption. (5) better gold price.

Goldprice shot up due to Obama authorizing the bombing of ISIS to protect American in Iraq.

Vested.

Last:

0.295 Vol:

184k +0.005

looks like they are ramping up production of goldbars.. gold price has been moving upwards as well

jcbull ( Date: 09-Jul-2014 19:02) Posted:

Sokor Gold Project produced 4,356.47 ounces of gold doré bars1 in the month of June 2014, which is the highest record todate for monthly output since the start of gold production in July 2010, surpassing its previous record of 3,419.51 ounces as reported in the Announcement, representing an increase of approximately

27.4%.

In line with the Company&rsquo s strategy of ramping up its gold production, the installation of a 350 tonnes per hour crushing system is currently in progress and near to completion. The Company expects to conduct trial runs of the crushing system in the third quarter of 2014.

Vested

|

|

Sokor Gold Project produced 4,356.47 ounces of gold doré bars1 in the month of June 2014, which is the highest record todate for monthly output since the start of gold production in July 2010, surpassing its previous record of 3,419.51 ounces as reported in the Announcement, representing an increase of approximately

27.4%.

In line with the Company&rsquo s strategy of ramping up its gold production, the installation of a 350 tonnes per hour crushing system is currently in progress and near to completion. The Company expects to conduct trial runs of the crushing system in the third quarter of 2014.

Vested

chart looks gd! strong consolidation at 270, RSI not oversold.

really looks gd

Listing ( Date: 02-Jul-2014 12:23) Posted:

|

Any updates?

Hopfully can see BIG push soon.....It' s a very good cheap stock with GREAT POTENTIAL!!!!!!......

ozone2002 ( Date: 17-Jan-2014 14:17) Posted:

|

Voyage Research optimistic about CNMC Goldmine Holdings' outlook

Analyst: Liu Jinshu  Chris Lim, CEO of CNMC Goldmine. Chris Lim, CEO of CNMC Goldmine.

NextInsight file photoCNMC Goldmine Holdings Limited announced in Dec 2013 that: a) it has formed a joint venture with the Perak state government to explore tin mining and b) it will be paying its maiden dividend of 0.1 S cents per share on 20 Jan 2014. We reiterate our highly positive outlook on CNMC on the back of increased production following the completion of leaching pad 2 in Sep 2013. Maintain Increase Exposure.

Reiterates Record Gold Pour in Nov: We recall that CNMC successfully commissioned its second gold de-absorption plant in Nov 2013, following record gold pours of 2,131oz (or 66.3kg) of gold dore bars from the new plant. In contrast, the company produced 81.5kg (or 2,620oz) of gold dore bars in Oct 2013. The new plant tripled overall gold de-absorption capacity to 3 t. per cycle to match the 2014 1m t. of ore heap leaching capacity.  Gold Prices Remain above Model Input: Gold Prices Remain above Model Input: Spot gold currently trades at US$1252/oz, which remains above the input gold price of US$1200/oz which we applied towards our forecasts and valuation of CNMC. We are unfazed by lower gold prices, as falling unit costs and higher production are expected to more than offset price declines. Moreover, the decline in gold prices seemed to have slowed since 3Q 2013 (down 2.7% from end 3Q 2013 to 14 Jan 2014). CNMC reported an impressive low all-in sustaining cost of US$566/oz in 3Q 2013. We remain optimistic about CNMC?s 4Q 2013 results and 2014 outlook.

ozone2002 ( Date: 17-Jan-2014 14:09) Posted:

was looking at voyage research.. looks promising to invest..

KIV |

|

|

|

Much more Rise to come...A very potential and Gem stock....

Hopfully can see some breakout from the current price.....

All good news, no reason not to move up........

More good news coming out from the company...hold more for good time to come

Indeed, this gold miner is doing very well recently and expect profit to escalate. Hopfully it will expand it' s mining to elsewhere in other region and outlook will be even more promising....Now it' s already good. Expect buying interest to come in....Let' s stay tune for it.....

fooodball ( Date: 15-May-2014 10:52) Posted:

this gold miner doing well..

will it go back up high

|

|

this gold miner doing well..

will it go back up high