https://www.stocksbnb.com/reports/wheelock-properties-singapore-prime-privatisation-candidate/

Privatisation thesis is still valid but what&rsquo s different this time round?

Our rationale for a privatisation is based on

Potential upside even without a privatisation

Investment Action

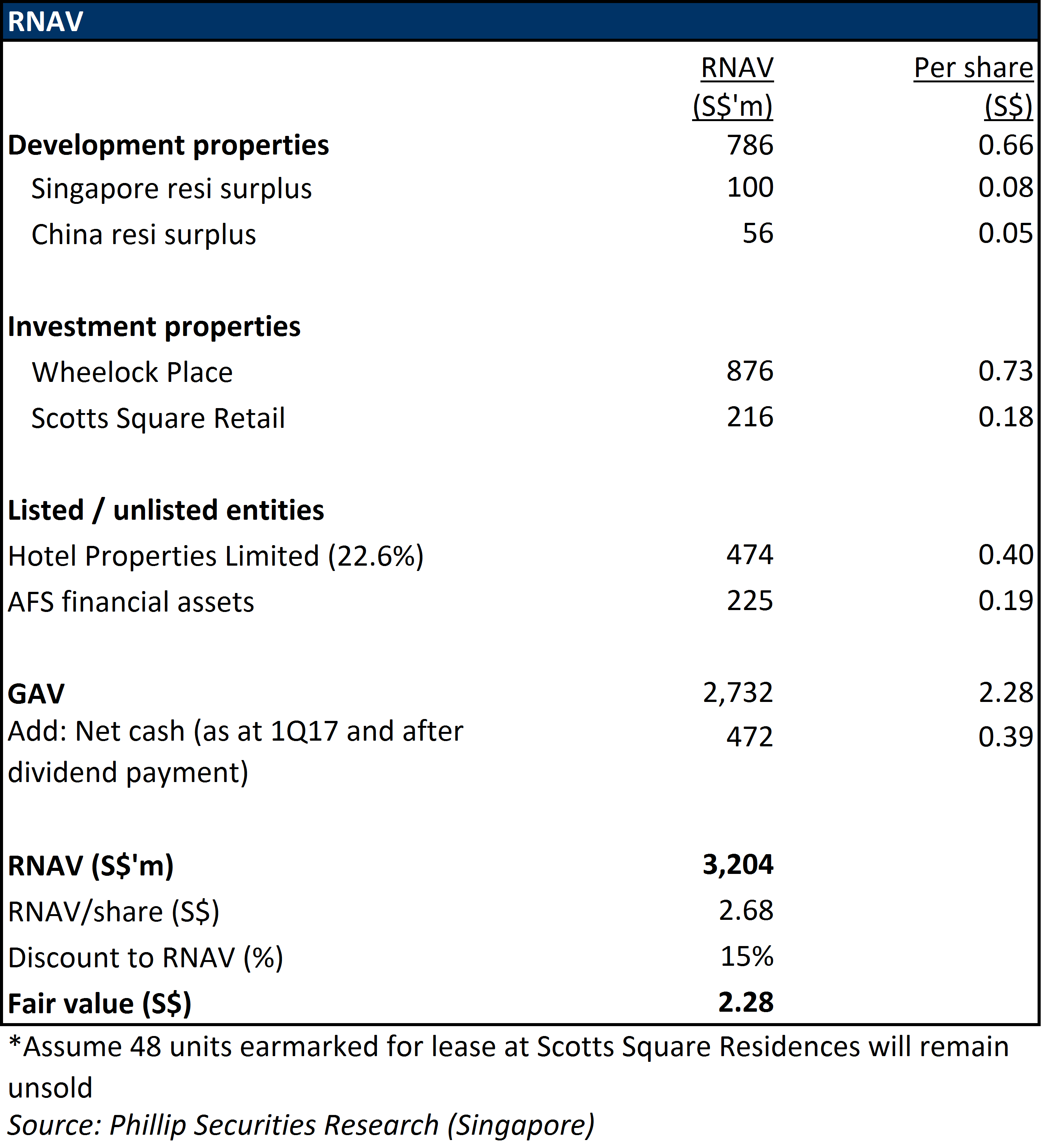

Given its valuation of 0.7x PB and a recent rally in share price, WPSG is still undervalued compared to its peers (0.9x PB). The current valuation also prices the Group&rsquo s S$1.1 billion of investment properties (Wheelock Place and Scotts Square) for free. With multiple catalysts that involve revenue recognition from development properties in the next 12 months and possibly a privatisation, the current valuation is undeservedly cheap. We have initiate with a Trading Buy and a target price of S$2.28 based on our full-year FY17 RNAV estimates.

Company Background

Wheelock Properties (Singapore) (WPSG), formerly known as Marco Polo Developments Limited, was listed on SGX-ST in 1981. The Group&rsquo s principal activities are property investment and property development with a focus on luxury developments. WPSG is a 76.2% subsidiary of Wheelock and Company (BB code: 20 HK).

Case for privatisation remains unchanged

We opine that Wheelock and Co could adopt a similar move for WPSG as shares of WPSG are thinly traded and has been trading at a significant discount to its NAV (40%). Additionally, the Group has not sought for funds from the equity market for more than 11 years since 2006.

Our rationale for a privatisation is based on:

Potential upside even without a privatisation

Wheelock Properties Singapore &ndash Prime privatisation candidate

June 2, 2017Recommendation: TRADING BUY // Target Price: S$2.28

- Valuations remain cheap with a growing net cash pile.

- In self-liquidation mode with all debt settled and development properties at tail end.

- Wharf Holdings&rsquo intent to consider listing a separate vehicle for its investment properties could bolster privatisation for Wheelock Properties Singapore (WPSG).

Privatisation thesis is still valid but what&rsquo s different this time round?

- In self-liquidation mode with all debt cleared as at 4Q16.

- Following the announcement of sister company, Wharf Holdings (BB Code: 4 HK), where it is exploring the option to spin off investment properties, Wheelock and Company (BB Code: HK 49) could take this opportunity to privatise WPSG.

- Cash position poised to double by 3Q17 upon recognition of revenue from The Panorama project.

Our rationale for a privatisation is based on

- All outstanding debt settled and no new land tender since 2013.

- Even more cash to be booked in the next two quarters.

- Existing assets could be inserted as part of sister company&rsquo s new listing involving its investment properties.

- HK parents gains full access to WPSG&rsquo s cash pile of c.S$830m.

- Most existing development projects are at their tail-end with no major foreseeable CAPEX.

- Allows the Group to wait for opportune time to clear remaining units and redevelopment opportunities involving existing investment properties.

Potential upside even without a privatisation

- Current valuation is still depressed compared to peers.

- Current discount to book should narrow with more cash to be booked in.

- BVPS expected to gain another 10 S&rsquo cents from deferred income by FY18.

- WPSG shares is an opportunity to enter HPL shares at a discount.

Investment Action

Given its valuation of 0.7x PB and a recent rally in share price, WPSG is still undervalued compared to its peers (0.9x PB). The current valuation also prices the Group&rsquo s S$1.1 billion of investment properties (Wheelock Place and Scotts Square) for free. With multiple catalysts that involve revenue recognition from development properties in the next 12 months and possibly a privatisation, the current valuation is undeservedly cheap. We have initiate with a Trading Buy and a target price of S$2.28 based on our full-year FY17 RNAV estimates.

Company Background

Wheelock Properties (Singapore) (WPSG), formerly known as Marco Polo Developments Limited, was listed on SGX-ST in 1981. The Group&rsquo s principal activities are property investment and property development with a focus on luxury developments. WPSG is a 76.2% subsidiary of Wheelock and Company (BB code: 20 HK).

- It has four ongoing property development projects (Singapore: 3, China: 1) under its property development arm.

- It owns two investment properties in Orchard Road, Wheelock Place and Scotts Square which are almost fully occupied as at 1Q17.

- It also owns a 22.6% stake in Hotel Properties Limited (BB Code: HPL SP) via its 40%-owned associate, 68 Holdings Pte Ltd.

Case for privatisation remains unchanged

- Wheelock Company HK privatisation transaction could re-enact for WPSG: Wheelock Properties HK was privatised by parent, Wheelock and Co (BB Code: HK 20), for HK$13 apiece in July 2010 following the sharp decline in share price caused by the 2008 global financial crisis. The offer price translates to a valuation of 0.96X PB. Wheelock and Co owned a 74% stake in Wheelock Properties HK prior to the offer. Wheelock Properties HK stated that the low liquidity and significant discount of its shares does not provide it with a viable funding alternative, as well as the need to continue bearing listing fees are among reasons for the privatisation move.

We opine that Wheelock and Co could adopt a similar move for WPSG as shares of WPSG are thinly traded and has been trading at a significant discount to its NAV (40%). Additionally, the Group has not sought for funds from the equity market for more than 11 years since 2006.

- No major developments since the passing of late CEO: Since the passing of CEO, David Lawrence, in 2012, the Group has not appointed another CEO and is currently helmed by Senior Executive Director, Ms Tan Bee Kim and Executive Director, Mr Tan Zing Yan, where the dual primarily oversees operations and risk management of the Group. According to AR16, the Group explains that it does not require a separate CEO and considers its current leadership structure efficient while taking into account of the company needs. Given that the Group has not elected a new CEO since 2012, we view that it is unlikely for operations to have a meaningful expansion. The Group has only engaged one property development project, The Panorama, in CY13 since then.

Our rationale for a privatisation is based on:

- All outstanding debt settled: Curiously WPSG has settled all its outstanding debt in 4Q16 and we view this is an unusual move for a property developer. Considering that net cash could soar to S$830 million from S$459 million by 3Q17 with the recognition of revenue from sales in The Panorama.

- Even more cash to be booked in: We opine that achieving S$830 million cash pile for WPSG is a bear case scenario, as this is assuming that there will be no further sales of unsold units from existing development projects. We estimate that the unsold units from Ardmore Three and Scotts Square Residences (excluding 48 units that are earmarked for lease) has a combined GDV of c.S$170m (5.4% of total GAV). With an expected recovery in CCR market segment, we view that it is unlikely for these units to stay unsold. Ardmore Three and Scotts Square Residences are freehold developments in the CCR market segment.

- Less cash for more cash: Assuming a conservative premium of 20% to the current market capitalisation of S$2.1 billion as at 2 June 2017, the Hong Kong parent would only need to shell out S$648 million to gain full access to the potential c.S$830 million cash pile since it owns 76% of WPSG.

- Existing assets could be inserted as part of sister company&rsquo s new listing Wharf Holdings (62% owned by Wheelock & Co), announced in March 2017 that they are exploring a possible separate listing of its investment properties in a bid to unlock shareholder&rsquo s value. We opine that the parent could delist WLSG and insert the two Singapore investment properties of WPSG as part of the new listing. The rationale behind the move is to negotiate for higher valuations by not being a direct comparable to other listed land lords in Hong Kong.

- Most existing development projects are at their tail-end with no major CAPEX: Apart from a development project in Fuyang City, other development projects from the company have already been mostly sold (> 80%). The Fuyang City project is about 23% launched and sold where it is expected to be fully complete by CY20, although its value is relatively small (about 25% of company&rsquo s development properties). We view that the sales registered in Phase 1 and 2A of Fuyang City Project will be able to fund the remaining project construction cost involved in the project.

- Wait for opportune time to clear remaining units and redevelopment of investment properties: A privatisation means that WPSG will be able to take its time to sell the remaining units in Scotts Square Residences and Fuyang City Project without having the need to answer to other shareholders. Its existing portfolio of Investment Properties (including HPL) in West Orchard sector offers significant redevelopment potential.

- Muted land banking activities since 2013: Since the last successful land tender took place in January 2013 for The Panorama (99.5% sold as at 1Q17), we have observed that WPSG has not participated in other land tenders under the Government Land Sale programme.

Potential upside even without a privatisation

- Current valuation is still depressed compared to peers: Wheelock and Company acquired 4.5 million more WPSG&rsquo shares (0.4% of total outstanding shares) in September 2016 at S$1.455. The previous share acquisition was in end-2011 when the company acquired 5.2m WPSG shares at S$1.50 apiece. The acquisition price of S$1.455 &ndash S$1.5 on two occasions suggests that price has somewhat already hit the floor. While the current share price of WPSG is about 15% &ndash 20% higher, translating to a valuation of 0.7X PB which is still relatively low when compared to a peer average of 0.9X.

- Current discount to book should narrow with more cash to be booked in: Out of its total assets as at 1Q17, more than 30% of this value is made up of liquid assets such as cash and marketable securities (including a 22.6% stake in HPL SP). This proportion is expected to grow to 50% as more cash will be booked in after The Panorama obtains TOP status in 3Q17, and a catalyst for the discount to narrow.

- BVPS expected to gain another 10 S&rsquo cents by FY18: BVPS of WPSG is expected to gain another 10 S&rsquo cents in FY18 via the booking in of S$100m of deferred income, upon the completion and hand over of units sold in Phase 2A of Fuyang City Project.

- WPSG shares is an opportunity to enter HPL at a discount: Given that WPSG is trading at a 0.7X PB, we view that each share acquired in WPSG represents an opportunity to enter HPL SP shares at a significant discount which are trading at 1.1X PB. WPSG owns a 22.6% stake in HPL SP shares via its associate company, 68 Holdings Pte Ltd.

Valuations