Cup and handle formation. Expect to cross 90 to 100 tmr...

PQTPQK ( Date: 12-Nov-2025 16:21) Posted:

|

very near to the hist high again...

SJ0724 ( Date: 12-Nov-2025 16:04) Posted:

|

So quiet here....

should test the high again...

Next33 ( Date: 06-Oct-2025 10:54) Posted:

|

" Nam Cheong&rsquo s shares currently trade at the lowest valuation among its oil and gas peers, with a PE ratio of just 3.8x versus the peer average of 9.6x.

This is also well below its historical average of 8.7x between 2008 and 2015, prior to its downturn.

While the circumstances today are certainly different, the valuation gap suggests scope for a re-rating should fundamentals continue to improve."

Source:

This is also well below its historical average of 8.7x between 2008 and 2015, prior to its downturn.

While the circumstances today are certainly different, the valuation gap suggests scope for a re-rating should fundamentals continue to improve."

Source:

Spotlight on Singapore&rsquo s oil & gas services sector: Two potential turnaround stocks

https://secure.fundsupermart.com/fsmone/article/rcms336853/spotlight-on-singapores-oil-gas-services-sector-two-potential-turnarou

3Q should be great because

-- seasonally it' s beautiful weather at sea, no monsoon rains, so the vessels are busy at work.

-- in addition, the long-term charters secured by Nam Cheong start after a period of preparation in 2Q (which was why 2Q utilisation rate was lower than expected).

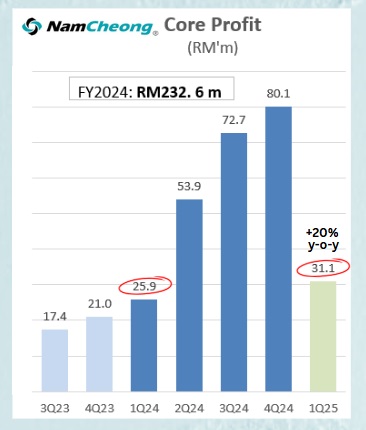

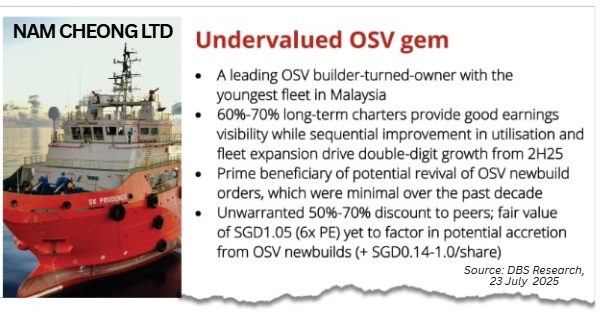

Fair value is $1.05 according to DBS Research.

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16215-nam-cheong-another-announcement-and-long-term-charters-rise-to-rm1-7-billion?highlight=WyJuYW0iLCJjaGVvbmciXQ==

-- seasonally it' s beautiful weather at sea, no monsoon rains, so the vessels are busy at work.

-- in addition, the long-term charters secured by Nam Cheong start after a period of preparation in 2Q (which was why 2Q utilisation rate was lower than expected).

Fair value is $1.05 according to DBS Research.

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16215-nam-cheong-another-announcement-and-long-term-charters-rise-to-rm1-7-billion?highlight=WyJuYW0iLCJjaGVvbmciXQ==

Solubl ( Date: 09-Sep-2025 11:57) Posted:

|

consolidation going on.... if 3Q results are good... thhe stock can re-rate

Nam Cheong PE around 4X, with upside potential of about 40% to DBS Research fair value price of $1.05

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16324-pacific-radiance-nam-cheong-positive-momentum-attracts-analyst-bullishness

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16324-pacific-radiance-nam-cheong-positive-momentum-attracts-analyst-bullishness

Just one of the small contracts probably include chartering of one fleet only. Termination due to non-performance by the contractor. Little to no impact as they can easily charter it short term. Look at the price you know artificially kena suppress to let BB buy more. Haha

TraderBen ( Date: 03-Sep-2025 21:45) Posted:

|

Contract termination.. omg

DBS Research

3 Sep 2025

Position for external funds inflow, EQDP, and REITs. These three sources of funds are driving Singapore equities higher YTD, beyond the STI heavyweights. Here&rsquo s how one can position going forward: (1) Passive funds: Driven by Singapore&rsquo s safehaven status, the stock market&rsquo s attractive yield, and P/B valuation, as well as the fading US exceptionalism narrative. Large-cap stocks are the key beneficiaries our picks are Singtel, Yangzijiang, DFI Retail. (2) EQDP for small-mid caps: Potential beneficiaries are UMS Integration, SIA Eng, ComfortDelGro, GuocoLand, Nam Cheong, SingLand Group, Hotel Properties. (3) Falling domestic interest rates: These are shifting flows from money markets (e.g., MAS T-bills, fixed deposits) into income stocks. Our picks include MLT, MPACT, CICT, FCT for large caps and Suntec REIT, LendLease REIT, ESR REIT, Elite UK REIT for SMCs.

3 Sep 2025

Position for external funds inflow, EQDP, and REITs. These three sources of funds are driving Singapore equities higher YTD, beyond the STI heavyweights. Here&rsquo s how one can position going forward: (1) Passive funds: Driven by Singapore&rsquo s safehaven status, the stock market&rsquo s attractive yield, and P/B valuation, as well as the fading US exceptionalism narrative. Large-cap stocks are the key beneficiaries our picks are Singtel, Yangzijiang, DFI Retail. (2) EQDP for small-mid caps: Potential beneficiaries are UMS Integration, SIA Eng, ComfortDelGro, GuocoLand, Nam Cheong, SingLand Group, Hotel Properties. (3) Falling domestic interest rates: These are shifting flows from money markets (e.g., MAS T-bills, fixed deposits) into income stocks. Our picks include MLT, MPACT, CICT, FCT for large caps and Suntec REIT, LendLease REIT, ESR REIT, Elite UK REIT for SMCs.

The Board of Directors (&ldquo Board&rdquo ) of Nam Cheong Limited (&ldquo Company&rdquo ) and its subsidiaries (together, the &ldquo Group&rdquo ) refer to its announcement dated 27 June 2025 (&ldquo Announcement&rdquo ) informing, inter alia, that the Group has secured a charter contract for one of its offshore support vessels (&ldquo OSV&rdquo ) to an offshore wind farm contractor in Japan (&ldquo Charterer&rdquo and &ldquo Charter Contract&rdquo ).

posted in SGX:

blocker for the time being...

posted in SGX:

blocker for the time being...

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16324-pacific-radiance-nam-cheong-positive-momentum-attracts-analyst-bullishness

PACIFIC RADIANCE & NAM CHEONG: Positive Momentum Attracts Analyst Bullishness

should test 0.80 again ...

aimtowin ( Date: 29-Aug-2025 16:41) Posted:

|

The Asian penny stock market in 2025 presents a compelling mosaic of opportunities for investors seeking undervalued companies with robust balance sheets and alignment to high-growth sectors. Amid a shifting macroeconomic landscape&mdash marked by U.S. monetary policy easing, trade dynamics, and sector-specific tailwinds&mdash certain stocks stand out for their fiscal discipline, strategic positioning, and potential to capitalize on global trends.

Shipbuilding and Energy Transition: Yangzijiang Shipbuilding (SGX:BS6) and Nam Cheong Limited (SGX:1MZ)

Yangzijiang Shipbuilding, a Singapore-listed shipbuilder, exemplifies the intersection of fiscal strength and sectoral momentum. With a debt-free balance sheet and a five-star financial health rating, the company is poised to benefit from the Asia Pacific Marine Scuttles Market&rsquo s expansion, driven by global demand for offshore vessels [1]. Similarly, Nam Cheong Limited has pivoted into offshore support vessels for renewable energy, with 80% of its fleet under long-term charters. This alignment with the energy transition reduces operational risk while capitalizing on green infrastructure investments [1].

https://www.ainvest.com/news/undervalued-asian-penny-stocks-strong-balance-sheets-2025-navigating-macroeconomic-shifts-high-potential-gains-2508/

Back to 6 series??

hopefully there is positive news coming...

UNCHARTED NOW!! 80 cents in sight!

stlimst ( Date: 21-Aug-2025 20:19) Posted:

|

Yes....possibly.

For me, I shifted some to BK after they annouced some positive news.

Good run, great!

For me, I shifted some to BK after they annouced some positive news.

Good run, great!

Newbie85 ( Date: 21-Aug-2025 18:12) Posted:

|