- Written by Sumer

- Published: 03 May 2014

Time & date: 2 pm, 29 Apr 2014.

Venue: Sheraton Towers.

Hotel Grand Central

Time & date: 11.30 am, 30 Apr 2014.

Venue: Hotel Grand Chancellor, No. 3 Belilios Road.

The following observations of the 2 AGMs were recently posted on NextInsight' s forum by Sumer, who is regarded as the resident property guru of the forum.

I ATTENDED Bonvests' and Hotel Grand Central' s AGMs to gauge for myself how the major owners/managementt are like. Here are my views:

1. I am not excited with the Bonvests team. Answers given by the board were short, with mostly " noted" as the answer to shareholders' queries and suggestions.

Management indicated no interest in redeveloping Liat Towers nor giving an indicative value in its annual report on the value of Sheraton Towers. Hence, I am not keen to follow up on the counter.

Nevertheless, the undervaluation of its assets remain. Perhaps patience may still pay off for those who own the stock, but I will pass on this one.

2. Hotel Grand Central' s (HGC) board is a direct opposite, a rather happy lot sharing information with shareholders generously.

2. Hotel Grand Central' s (HGC) board is a direct opposite, a rather happy lot sharing information with shareholders generously.The 2 Orchard Road hotels should achieve Temporary Occupation Permits (TOP) next year. With 752 rooms in total, any post-TOP valuation of these assets will add to its NTA.

I reckon a 50-ct surplus could be in order. It would even be better if management is open to the possibility of selling the leasehold hotel while keeping the freehold one, as that will mean a cash inflow that could be distributed out as dividends.

Nevertheless, as this is a hotel stock, a substantial discount to its NAV is a trade mark of its breed.

Management' s likability will probably keep me interested in this counter, despite its lack of immediate catalysts.

I think the 2 main speakers were 2 of the 3 Tan brothers: Tan Eng Teong, Teck Lin and Eng How. A woman who spoke, I believe, could be Tan Hwa Lian or Hellen Tan, or Michelle Tan (all are daughters of either one of the 3 brothers).

I believe Anthony Poh, the group accountant, also spoke.

I thought I could Google their pictures later, but apparently it' s hard to find them, so I am not too sure who exactly were the ones who spoke. Suffice, perhaps to say, that I had a good impression of all of those who spoke.

I notice Hotel Grand Central has many loyal long-time retail shareholders too, and they appear happy with management, a sign perhaps that they have been well looked after over the years.

For eg, I note that the company has dished out consistently good dividends. Even though earnings were below 3ct per share last year, HGC dished out 5ct dividend, allowing many to take scrip dividend and increase their stake in the company while HGC saves on cash payouts.

Compare HGC with some listed companies which consistently give the excuse that they " need money for expansion" for not paying better dividends.

Note: I am vested in HGC, but not a lot as it' s, after all, a hotel stock, and catalysts are few.

Hotel Grand Central has a market cap of S$716 million and a 4.2% dividend yield.

Hotel Grand Central has a market cap of S$716 million and a 4.2% dividend yield. Chart: FT.com

|

Lotustpsll says: Bonvest' s BOD may not be in tune with the times as to how to positively engage shareholders. Perhaps, they don' t need to, given the low level of minority shareholding - sadly, such cockiness or lackadaisical attitude is often seen. Sumer, how old (do you think) is Henry Ngo? I will stay vested on Bonvest as a deep value play. Interest in major S' pore commercial properties is there and I think this trend will continue given the attractiveness of the nation (asset value in both Sheraton and Liat will likely appreciate further). I will stay the course and bid my time. Diversity says: Yes, Chairman and his brother, Tan Teck Lin, are unassuming. Many years ago when HGC decided to invest in Australia and NZ, shareholders were jittery. HGC subsequently sold its NZ commercial properties for huge gains and bought land in Little India to build its second hotel in S' pore. In the recent two years, besides demolishing the flagship hotel in the Orchard Road area to build two new hotels, HGC bought two commercial properties in Australia and NZ with high rental yields. HGC now owns 3,008 rooms (not counting the 752 rooms under construction) in 15 hotels and 24,700 sq metres of lettable space in 3 commercial buildings. HGC is still holding on to the site in Christchurch where its hotel was hit by an earthquake and demolished later. HGC is planning to build a commercial building on the site to house government departments. Despite all these, its gearing is still low -- $152 m loans against $132m cash as at the end of 2013, the result of good financial discipline. |

The 165-room, 4-star Hotel Grand Chancellor in the Tasmanian city of Launceston: Its rooms are spacious and well kept, and the breakfast is excellent. Photo by Leong Chan TeikDuring my recent holiday in Tasmania, our tour group checked into Hotel Grand Chancellor Launceston. I felt a thrill when I recognised it as belonging to Singapore-listed Hotel Grand Central Limited in which I hold a small number of shares. The 165-room, 4-star Hotel Grand Chancellor in the Tasmanian city of Launceston: Its rooms are spacious and well kept, and the breakfast is excellent. Photo by Leong Chan TeikDuring my recent holiday in Tasmania, our tour group checked into Hotel Grand Chancellor Launceston. I felt a thrill when I recognised it as belonging to Singapore-listed Hotel Grand Central Limited in which I hold a small number of shares. The listco owns 13 hotels in five countries. It also has five associated hotels in Malaysia and three investment properties in Australia and New Zealand. I have held the shares for nearly four years, during which time I have not paid much heed to the share price movement nor Hotel Grand Central' s business performance. My " buy-and-forget" approach stems from my view that this is a relatively stable business, and I expect it to reliably yield a decent return under a seasoned management (The hotel listed on SGX in 1978). I have just discovered that my expectations have been met, as reflected by recent highlights of the company (below) that I have dug up. I reckon the outlook is challenging, though, as Airbnb and its peers will increasingly exert competitive pressure on hotel operators everywhere (see stories such as The Airbnb effect: tourists shun hotels for private stays). |

1. In 9M2016, Hotel Grand Central achieved S$39.4 million in net earnings, boosted by a S$28.1 million gain from the sale of a hotel in Gold Coast.

Its 9M2015 earnings (S$80.5 million) was enlarged also by one-off gains from the sale of assets.

| Stock price | $1.345 |

| 52-week range | $1.12 - $1.395 |

| Market cap | $892 m |

| PE (ttm) | 20 |

| Dividend yield | 3.72% |

| NAV | $1.95 |

| Data: Company, Bloomberg | |

2. Revenue was up 18% in 9M2016 to S$104.5 million, thanks to contributions by the redeveloped Hotel Chancellor @ Orchard and Hotel Grand Central which soft-opened in May and October 2015, respectively.

3. The 79-year-old chairman-cum-MD' s deemed interest in Hotel Grand Central has been rising. It now stands at 409,118,833 shares, or a 61.703% stake.

The most recent change in Tan Eng Teong' s interest took place from early June through early Aug 2016, when it rose by 250,500 shares.

4. Hotel Grand Central has been a reliable deliverer of dividends. For example, for FY11, 12, and 13, it paid out 5 cents a share, giving shareholders the option to receive it in cash or in scrip (at a certain discount to the market price).

In FY14, it paid out 10 cents a share (with a scrip option) before reverting to 5 cents a share (in cash only) for FY15.

5. The share price has done well, delivering a nearly 100% return over the past five years. Add the 30 cents a share in dividends ....

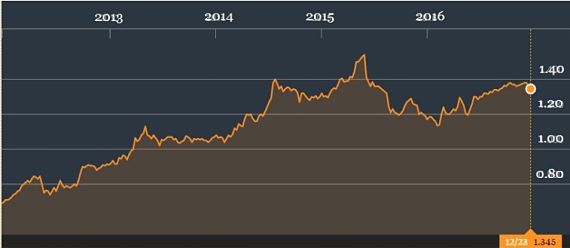

From 69 cents on 23 Dec 2011 to $1.345 currently, Hotel Grand Central has delivered capital gains of nearly 100%. In that period, the dividends totalled 30 cents a share. Thus, total shareholder return: 138%. Chart: Bloomberg

From 69 cents on 23 Dec 2011 to $1.345 currently, Hotel Grand Central has delivered capital gains of nearly 100%. In that period, the dividends totalled 30 cents a share. Thus, total shareholder return: 138%. Chart: BloombergSee past stories by various shareholders: