The annual dividend of BA was about 7.9%. 3.2 already paid in Dec 25 as interim and 3.22 skan dstsng in May. Only reasonably good companies can have such good payouts.

Expect BA to take off soon. It has only only a good quality earning with sounding cash accrual ratio that turns earnings into free cash but also an excellent 30% EBITDA margin that only software companies can match. It will be a challenge for shortists to short BA.

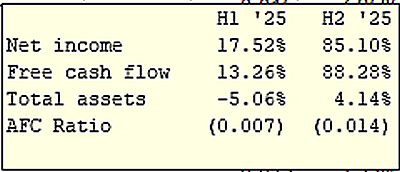

This counter has started to rise and if it can keep above 1.50, the breakout price for the present trend/ The target ' price is aroujnd 2.00 for a reward ratio of 2:1. This counter has a good fundamental with positive net income that has been converted to free cash, which is even better than Wilmar.

Tob231 ( Date: 02-Mar-2026 09:59) Posted:

Joelton, with such good result, this counter dropped ...

dividend also no enough to cover the drop 😫 |

|

Bumitama Agri H2 earnings rise 7.4% to 1.54 trillion rupiah on record-high Q4 revenue

The group&rsquo s total dividend for the year will be S$0.0935 per share &ndash an all-time high

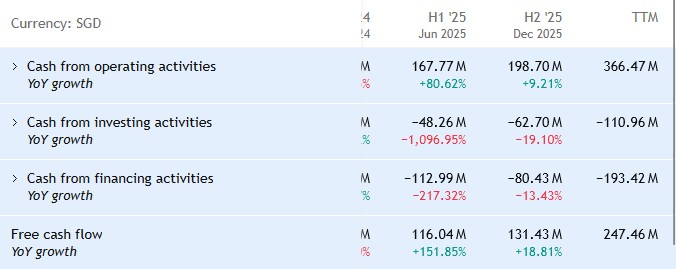

[SINGAPORE] Indonesian palm oil producer Bumitama Agri : P8Z -0.75% posted a net profit of 1.54 trillion rupiah (S$120 million) for its second half ended Dec 31, 2025, up 7.4 per cent from 1.43 trillion rupiah in H2 2024.

Its earnings per share (EPS) for the six months stood at 886 rupiah, up from 825 rupiah in the year-ago period, the group said on Friday (Feb 27).

Revenue for the half-year climbed 11.8 per cent year on year to 10.21 trillion rupiah, from 9.13 trillion rupiah.

The improvements came as the company recorded its highest ever quarterly revenue for Q4 2025, of 6.34 trillion rupiah, which surpassed the previous record high it achieved.

On the back of a robust financial performance, the company proposed a final dividend per share of S$0.0322 for FY2025. This brings its total dividend per share for the year to S$0.0935, which the group said is an all-time-high distribution and a 41 per cent increase from the prior financial year.

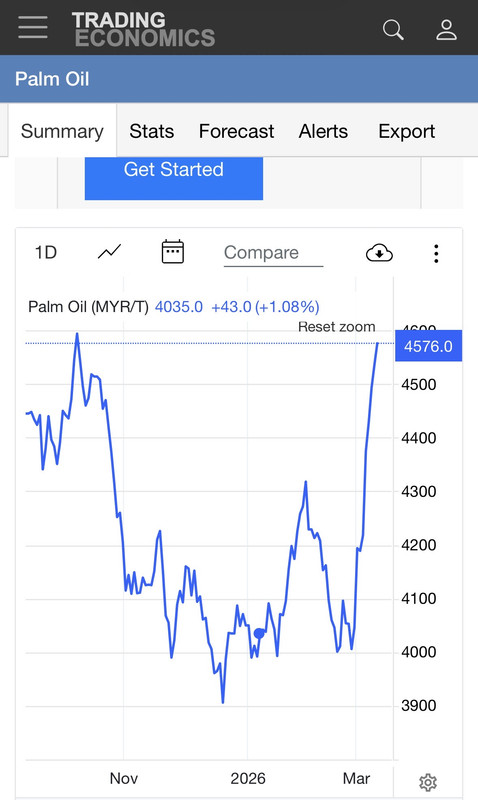

Firmer palm oil prices lift SGX agri stocks ahead of H2 results, but Indonesia risks cloud outlook

Market watchers expect the strong streak from earlier in FY2025 to continue, but individual companies face potential downside risks

[SINGAPORE] The tightening global supply of crude palm oil (CPO) likely boosted Singapore-listed agriculture players for the second half and fourth quarter of the 2025 financial year, but investors remain wary as Indonesia& rsquo s shifting regulations and land clawback campaign cast a shadow over the sector.

With the companies expected to report their results this week, analysts said industry tailwinds should extend the strong momentum from H1, though policy risks and company-specific challenges cloud the outlook.

Meanwhile, attention is also on Olam Group : VC2 , which is continuing its multi-year restructuring. Investors are closely watching its balance sheet for progress on the divestment of its Olam Agri unit to the Saudis and the planned initial public offering of its food ingredients unit, ofi.

Palm oil planters

Analysts flagged two key developments in H2 FY2025 for palm oil producers: regulatory fog in Indonesia and higher CPO prices due to tighter supply.

The prices are expected to be boosted by Indonesia& rsquo s B50 biodiesel mandate, which requires the blending of 50 per cent palm oil-based fuel with diesel, said OCBC Group Research in a note on Jan 14.

Despite the postponement of Indonesia& rsquo s B50 mandate, the existing B40 programme absorbed over 13 million tonnes of CPO in 2025, compared with 7.5 million tonnes in 2020. This provides a robust floor for palm oil demand, helping to underpin prices, said Macquarie Equity Research in a note on Jan 16.

Nirgunan Tiruchelvam, head of consumer and Internet at Aletheia Capital, noted in October 2025 that Bumitama Agri : P8Z and First Resources : EB5 are the most leveraged to CPO price gains through youthful estates and high extraction rates.

Indofood Agri Resources : 5JS should benefit from stronger downstream refining spreads, while Kencana Agri : BNE offers the highest operating leverage given its smaller base, said Tiruchelvam.

These four Singapore-listed stocks are priced around 30 per cent lower than their competitors, despite having a return on invested capital in the mid-teens and dividend yields of up to 9 per cent, he added.

Still, he highlighted a valuation gap. While CPO prices doubled between 2015 and 2025, regional plantation stocks lagged by 17 per cent.

He attributed this disconnect to a sharp decline in the correlation between palm oil prices and stock performance, which fell from 83 per cent between 1995 and 2015 to 42 per cent after 2015. This drop came as fund managers divested palm oil for ESG reasons, he said.

However, geopolitical shifts, such as the rollback of ESG standards under the Trump administration, could reignite investor interest and potentially restore the historical link between commodity prices and plantation share values, he noted.

Macquarie analysts Amanda Foo and Hanel Tan said that the global CPO market was moving into a & ldquo structurally tight phase& rdquo . They added that supply growth is increasingly capped by moratoriums on new plantation developments in Indonesia and Malaysia, declining yields from ageing trees, and the onset of La Nina weather patterns.

That said, regulatory risks remain. Indonesia& rsquo s land clawback campaign potentially affects hundreds of companies across palm oil, forestry and mining. OCBC analysts noted that the risk of regulatory fines from alleged unauthorised planting in Indonesia could weigh on investor confidence.

Meanwhile, market watchers said that larger integrated players such as Wilmar International : F34 and Golden Agri-Resources : E5H are also likely to benefit from firmer CPO prices.

Tiruchelvam, however, noted that Wilmar& rsquo s contract fraud liability ruling in China and ongoing legal challenges in Indonesia introduced a & ldquo structural overhang& rdquo .

Macquaries Foo added in a separate note: & ldquo While Wilmar has yet to find reprieve from its regulatory situation, we believe this has been more than priced in by the market.& rdquo

OCBC Group Research expects Golden Agri-Resources to report softer fresh fruit bunch production in H2 2025 due to its aggressive replanting programme and dry weather conditions.

Olam Group

While palm oil players grapple with yields and mandates, agribusiness giant Olam Group is navigating developments centred on its balance sheet and the completion of its reorganisation strategy.

Market watcher Jamal Aliyev, manager at nut distribution company CCI Apac, noted that Olam Group& rsquo s primary drag has been high net gearing, driven by the spike in cocoa and coffee prices in 2024.

During Olam Groups earnings briefing for FY2024, the company reported that invested capital grew by 34.4 per cent year on year, primarily on elevated commodity prices in its ofi portfolio.

However, with cocoa prices retreating from over US$11,000 per tonne in 2024 to around US$3,300 per tonne now, Olam Group is expected to see a reduction in working capital needs, noted Aliyev.

This should lead to improvements in net gearing, fortify Olam Groups balance sheet and lower its finance expenses for the second half of FY2025 and the first half of FY2026, he added.

Post-Olam Agri divestment, the remaining Olam Group will be practically debt-free, he said, as the majority of the sale proceeds are intended to repay the group& rsquo s debt.

Full-year results for the agri sector kick off on Feb 26 with Golden-Agri Resources and Wilmar, while Bumitama Agri, First Resources, Indofood, Mewah International and Olam Group will report on Feb 27.

Bumitama Agri&rsquo s 9M profit rises 29% with record rainfall in Central Kalimantan

Crude palm oil accounts for 84% of its sales, with the remainder from palm kernel

[SINGAPORE] Palm oil producer Bumitama Agri posted a 29 per cent rise in net profit to 1.87 trillion rupiah (S$145.7 million) for the nine months ended Sep 30.

This was on the back of an 18 per cent rise in its nine-month revenue to 13.6 trillion rupiah, the company said in a business update on Thursday (Nov 13).

Bumitama&rsquo s revenue was buoyed by production recovery, which progressed as expected, and improved productivity. The output of fresh fruit bunches was up 8 per cent to 2.54 million tons.

&ldquo The respectable output performance occurred amid record-breaking rains in the Central Kalimantan estates during September,&rdquo Bumitama said, adding that the weather had hindered some deliveries.

Crude palm oil accounted for 84 per cent of its sales, while the remainder came from palm kernel.

Contributions from both rose during the 9M period, driven by increases in average selling prices from the year-ago period &ndash by 17 per cent for crude palm oil, and 75 per cent for palm kernel.

&ldquo Improving industry prospects in the past five years have resulted in robust financial performance and paved the way for significant deleveraging,&rdquo the company said, adding that it expects Q4 to be the peak crop period of the year.

+0.04

+0.04