Its a flash report, perhaps bulls still waiting for the actual numbers end of April...

however , flash report is much like sample size during election....usually quite accurate

however , flash report is much like sample size during election....usually quite accurate

JurongW ( Date: 07-Apr-2026 16:48) Posted:

|

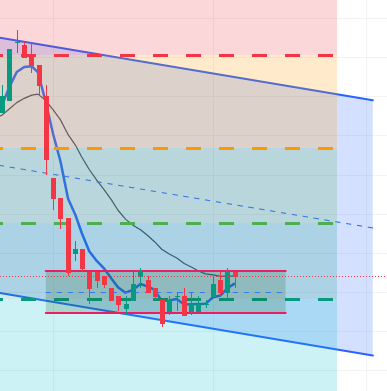

$1.30 have some technical support...

Sgvale ( Date: 07-Apr-2026 16:43) Posted:

|

I see. Breakdown based on negative URA report which happen a few days ago.

Perhaps, the bad news has been priced in or not yet?

Perhaps, the bad news has been priced in or not yet?

muifan ( Date: 07-Apr-2026 16:35) Posted:

|

Next level $1.45

this horse is waiting for breakdown...

URA report few days ago...Sale transaction volume fell by about 40% on a quarter-on-quarter basis in 1st Quarter 20261.

URA report few days ago...Sale transaction volume fell by about 40% on a quarter-on-quarter basis in 1st Quarter 20261.

Tripletop breakout from the channel soon?

Pending 5/20 EMA crossover for entry confirmation.

Pending 5/20 EMA crossover for entry confirmation.

JurongW ( Date: 07-Apr-2026 14:12) Posted:

|

Pending breakout from the channel.......soon ?

Purchase of 66,500 shares by CEO:

- 25 Mar - 22,000 shares at $1.67

- 26 Mar - 44,500 shares at $1.68

Below for reference only. This is based on inputs from MS-copilot - do verify the figures as sometimes they can be wrong.

PropNex currently trades at a richer valuation than APAC Realty, reflecting its stronger earnings momentum and higher dividend yield. APAC Realty, meanwhile, is priced more conservatively, with analysts generally assigning neutral to accumulate ratings.

PropNex currently trades at a richer valuation than APAC Realty, reflecting its stronger earnings momentum and higher dividend yield. APAC Realty, meanwhile, is priced more conservatively, with analysts generally assigning neutral to accumulate ratings.

📊 Valuation Comparison: PropNex vs APAC Realty (as of Mar 2026)

| Metric | PropNex (SGX:OYY) | APAC Realty (SGX:CLN) |

|---|---|---|

| Market Cap | ~SGD 1.30 billion | ~SGD 450&ndash 500 million (based on analyst coverage) |

| Enterprise Value | SGD 1.15 billion | Not disclosed, but significantly lower given smaller scale |

| PE Ratio (Trailing/Forward) | 18.5x / 18.0x | Estimated 12&ndash 14x based on target prices and earnings |

| Dividend Yield | ~5.1% (99.9% payout ratio) | ~3.5&ndash 4.0% (historical range, lower payout) |

| Analyst Ratings | Generally positive (UOB Kay Hian, DBS highlight strong earnings momentum) | Mixed: Accumulate/Hold/Neutral with target price around S$0.66&ndash 0.70 |

| Growth Drivers | Strong pipeline of new residential launches, record FY2025 revenue, robust resale activity | Stable but slower growth, reliant on resale and rental markets, less exposure to new launches |

🔎 Key Insights

- PropNex Premium: Investors are willing to pay a higher multiple for PropNex because of its dominant market share in Singapore, strong earnings recovery, and high dividend payout.

- APAC Realty Discount: APAC Realty trades at a lower valuation, reflecting smaller scale, thinner margins, and less aggressive growth prospects. Analysts are cautious, with most ratings around Neutral/Hold.

- Dividend Contrast: PropNex&rsquo s nearly full payout ratio (~99.9%) makes it attractive for income-focused investors, while APAC Realty&rsquo s yield is more modest.

- Risk Profile: PropNex&rsquo s valuation premium means it is more sensitive to downturns in property transaction volumes. APAC Realty, while cheaper, may offer less upside unless it captures stronger market share or benefits from sector tailwinds.

⚖ ️ Bottom Line

- If you want growth + yield &rarr PropNex looks stronger, with higher valuation justified by earnings momentum.

- If you want value entry &rarr APAC Realty offers a cheaper way to play Singapore&rsquo s property brokerage sector, but upside is capped unless market conditions improve significantly.

Still looks expensive relative to APAC Realty.

Down so much. Wait to cherry pick.

River Green over weekend sold 90%. War time still got so many people buying.

After xd dividends more to drop

Joelton ( Date: 04-Mar-2026 10:15) Posted:

|

Analysts downgrade PropNex on expected slowdown in home sales

Phillip Securities downgraded PropNex to &lsquo accumulate&rsquo with a higher target price DBS downgraded the firm to &lsquo hold&rsquo and lowered its target price

[SINGAPORE] Analysts have downgraded their calls on PropNex on forecasts that a moderation in residential sales for 2026 could impact earnings, after the real estate firm posted record performance for 2025 last week.

Phillip Securities on Monday (Mar 2) lowered its recommendation for PropNex to &ldquo accumulate&rdquo from &ldquo buy&rdquo , on expectations of a decline in new home sales in 2026, but raised its target price to S$2.08 from S$2.02.

Meanwhile, DBS on Monday downgraded its call on the firm to &ldquo hold&rdquo and lowered its target price to S$1.95 from S$2.15, using a sum-of-the-parts approach. The bank pointed to a &ldquo more measured earnings growth profile&rdquo moving forward following a share price rally of nearly 100 per cent in 2025.

This comes as PropNex on Friday recorded its strongest full-year revenue in its 25 year history, with revenue up 42.6 per cent at S$1.1 billion from S$783 million previously, and net profit rising 72 per cent on the year to S$70.4 million for FY2025.

Paul Chew, Phillip Securities head of research, expects new home sales to decline by 17 per cent decline for 2026, while private and HDB resale volumes are expected to be flat. However, he noted that H1 2026 earnings will register strong unbilled sales in Q4 2025.

This comes as a lower number of new launches and the absence of pent-up demand will impact new home sales, Chew said. He noted that some 8,800 units are to be launched in 2026, down from 11,409 units in 2025.

Similarly, DBS analyst Tabitha Foo projects a &ldquo more modest growth trajectory&rdquo for PropNex in FY2026 to FY2027, with a &ldquo more modest pipeline of new launches in 2026&rdquo after 2025 recorded stellar sales volumes, especially in the primary market.

&ldquo The launch pipeline comprises a larger proportion in the Outside Central Region, which typically is more price quantum sensitive. Nonetheless, with its commanding market share, PropNex is still poised to capture a lion share of transactions,&rdquo Foo said.

Phillip Securities&rsquo Chew forecasts PropNex&rsquo s profit after tax and minority interests for FY2026 to come in 15 per cent lower.

Foo noted that DBS has lowered its earnings estimate for FY2026 to FY2027 by around 21 to 22 per cent on assumptions of lower new home sales.

Strong demand driven by population increase, market leadership

While home sales volumes are set to ease, Phillip Securities&rsquo Chew expects population growth to shore up strong underlying demand for residential property.

Chew highlighted an expected increase in population numbers for 2026, with an expected increase of 25,000 to 30,000 new citizens. He said: &ldquo New citizens are incentivised to purchase properties by lower or no stamp duty, the avoidance of high rent and their tendency to have higher-tier income.&rdquo

&ldquo There is a rising number of wealth transfer buyers where parents support the property purchase of their children,&rdquo Chew added.

DBS believes that PropNex&rsquo s leading position in Singapore&rsquo s real estate brokerage services market and large sales force should enable it to grow its market share across various segments and support its performance in 2026.

&ldquo Given its commanding market share and diversified earnings base (new launches, private resale and HDB resale), performance in 2026 could still come in higher year on year,&rdquo said DBS.

The bank noted that PropNex has Singapore&rsquo s most extensive sales network with more than 14,000 agents, close to 40 per cent of the share of salespersons across property agencies.

Phillip Securities downgraded PropNex to &lsquo accumulate&rsquo with a higher target price DBS downgraded the firm to &lsquo hold&rsquo and lowered its target price

[SINGAPORE] Analysts have downgraded their calls on PropNex on forecasts that a moderation in residential sales for 2026 could impact earnings, after the real estate firm posted record performance for 2025 last week.

Phillip Securities on Monday (Mar 2) lowered its recommendation for PropNex to &ldquo accumulate&rdquo from &ldquo buy&rdquo , on expectations of a decline in new home sales in 2026, but raised its target price to S$2.08 from S$2.02.

Meanwhile, DBS on Monday downgraded its call on the firm to &ldquo hold&rdquo and lowered its target price to S$1.95 from S$2.15, using a sum-of-the-parts approach. The bank pointed to a &ldquo more measured earnings growth profile&rdquo moving forward following a share price rally of nearly 100 per cent in 2025.

This comes as PropNex on Friday recorded its strongest full-year revenue in its 25 year history, with revenue up 42.6 per cent at S$1.1 billion from S$783 million previously, and net profit rising 72 per cent on the year to S$70.4 million for FY2025.

Paul Chew, Phillip Securities head of research, expects new home sales to decline by 17 per cent decline for 2026, while private and HDB resale volumes are expected to be flat. However, he noted that H1 2026 earnings will register strong unbilled sales in Q4 2025.

This comes as a lower number of new launches and the absence of pent-up demand will impact new home sales, Chew said. He noted that some 8,800 units are to be launched in 2026, down from 11,409 units in 2025.

Similarly, DBS analyst Tabitha Foo projects a &ldquo more modest growth trajectory&rdquo for PropNex in FY2026 to FY2027, with a &ldquo more modest pipeline of new launches in 2026&rdquo after 2025 recorded stellar sales volumes, especially in the primary market.

&ldquo The launch pipeline comprises a larger proportion in the Outside Central Region, which typically is more price quantum sensitive. Nonetheless, with its commanding market share, PropNex is still poised to capture a lion share of transactions,&rdquo Foo said.

Phillip Securities&rsquo Chew forecasts PropNex&rsquo s profit after tax and minority interests for FY2026 to come in 15 per cent lower.

Foo noted that DBS has lowered its earnings estimate for FY2026 to FY2027 by around 21 to 22 per cent on assumptions of lower new home sales.

Strong demand driven by population increase, market leadership

While home sales volumes are set to ease, Phillip Securities&rsquo Chew expects population growth to shore up strong underlying demand for residential property.

Chew highlighted an expected increase in population numbers for 2026, with an expected increase of 25,000 to 30,000 new citizens. He said: &ldquo New citizens are incentivised to purchase properties by lower or no stamp duty, the avoidance of high rent and their tendency to have higher-tier income.&rdquo

&ldquo There is a rising number of wealth transfer buyers where parents support the property purchase of their children,&rdquo Chew added.

DBS believes that PropNex&rsquo s leading position in Singapore&rsquo s real estate brokerage services market and large sales force should enable it to grow its market share across various segments and support its performance in 2026.

&ldquo Given its commanding market share and diversified earnings base (new launches, private resale and HDB resale), performance in 2026 could still come in higher year on year,&rdquo said DBS.

The bank noted that PropNex has Singapore&rsquo s most extensive sales network with more than 14,000 agents, close to 40 per cent of the share of salespersons across property agencies.

The drop in share price seems to be driven by investors taking profits and reacting to a lower dividend payout, rather than a lack of underlying business performance.

QueenMaya ( Date: 27-Feb-2026 13:55) Posted:

|

Clear case of a big boy getting out who got in much earlier.

beng1102 ( Date: 27-Feb-2026 13:30) Posted:

|

Strong buy now @2.03 as selling seems over.

stlimst ( Date: 27-Feb-2026 11:58) Posted:

|

This is SGX.

BBs control not the common folks.

BBs control not the common folks.

beng1102 ( Date: 27-Feb-2026 11:07) Posted:

|

Good result. Why drop so much now. Strangely! Sell on news cannot explain this drop as it is too much.

Joelton ( Date: 27-Feb-2026 10:17) Posted:

|