No I ite

daytrader123 ( Date: 24-Aug-2021 00:36) Posted:

|

I think I got A* for history... you seem to be able to read my mind well.. you got study psychology is it?

leroy55 ( Date: 24-Aug-2021 00:24) Posted:

|

Tell me more about oio. You know ah Tiong. You sound like you know the history very well.

daytrader123 ( Date: 24-Aug-2021 00:18) Posted:

|

Sorry I hardly short....

I recommend if you dare, try shorting OIO:)

I recommend if you dare, try shorting OIO:)

leroy55 ( Date: 24-Aug-2021 00:03) Posted:

|

Daytrader, u can consider to short sta counter too

what bring u here by the way ?

what bring u here by the way ?

SNP 500 just broke through previous high of 4480 hitting a high just now at 4484 and now still trending up as strength begets strength climbing a wall of worries type of market.

Like I mentioned in earlier report, US stock market is in a SECULAR BULL Market.

Any type of corrective drop by 5% to 8% after establishing new high will not derail its short term trend as its medium to long term PRIMARY UPTREND is intact.

My Fibonacci target 1% extension still on course to target minimum 4600 and above by year end remains unchanged.

Like I mentioned in earlier report, US stock market is in a SECULAR BULL Market.

Any type of corrective drop by 5% to 8% after establishing new high will not derail its short term trend as its medium to long term PRIMARY UPTREND is intact.

My Fibonacci target 1% extension still on course to target minimum 4600 and above by year end remains unchanged.

你 的 前 世 不 就 是 哪 个 tony或 royal吗 ? 你 的 阿 拉 伯 同 志 跑 去 哪 哪 了 ? 你 投 胎 转 世 了 喔 !

yerongtian ( Date: 23-Aug-2021 17:56) Posted:

|

A GOOD READ ON THE US STOCK MARKET BY A 3RD PARTY ANALYST:

" The markets finished higher on Friday, but lower for the week.

Stocks have been on a tear recently, helped by a stellar Q2 earnings season, and a better than expected employment report.

But as earnings season winds down, and the latest jobs report becomes more distant in the rearview mirror, stocks took a pause.

There is no doubt the economy is strong. Even with renewed concerns over increasing virus cases threatening to slow the reopening.

One look at the jobs picture shows that. And with more jobs available than there are unemployed people to fill them, it looks like the robust pace of hiring will continue for quite some time.

But while economic growth is all around, some numbers have slipped a bit. Still growing, but maybe not quite as fast as had been expected.

Some of this was brought on by supply chain disruptions and worker shortages.

But with the enhanced unemployment benefits, which incentivized some workers to stay at home, expiring in September, we should soon see millions of new workers joining the workforce in the months ahead, and that should begin to bring relief to both of the aforementioned concerns, along with some inflation relief as well.

We should also soon get some insight on the fate of the $1.2 trillion infrastructure bill, and the $3.5 trillion budget framework, with the House returning to session this week.

That could inject another massive dose of spending into the economy.

But, of course, that will also likely come with tax proposals as well.

So traders will be watching these developments carefully.

In the meantime, we have a full slate of economic reports on deck this week starting with today' s Chicago Fed National Activity Index, the PMI Composite Flash report, and Existing Home Sales.

Tomorrow we' ll get the Redbook retail sales report, New Home Sales, and the Richmond Fed Manufacturing Index.

On Wednesday its MBA Mortgage Applications, Durable Goods Orders, and the State Street Investors Confidence Index.

Thursday we' ll get another look at Q2 GDP, Weekly Jobless Claims, Corporate Profits, and the Kansas City Fed Manufacturing Index.

And then of Friday, we' ll finish up with Personal Income and Outlays, Retail and Wholesale Inventories, and Consumer Sentiment.

We' ll also hear from Fed Chair Jerome Powell on Friday morning, as he speaks at the Jackson Hole, WY Economic Symposium, which has been moved online.

His speech on ' The Economic Outlook' will be closely watched.

Should be a busy week.

And with stocks trading near their all-time highs, it won' t take much to see them break out even higher."

As always, due diligence will prevail.

NB:

Correction from previous SNP 500 high of 4480 may be tested again.

Failing which, SNP 500 may fall back 200 to 300 points to test between 4180 to 4280 range.

Yet major support lies between 4100 and 4150.

All said, SNP 500 is still in a SECULAR BULL market and that any short term drawdown between 5% to 8% drop will not even derial its Primary Uptrend to eventually test Fibonacci 1% extension minimum 4600 and above by year end.

" The markets finished higher on Friday, but lower for the week.

Stocks have been on a tear recently, helped by a stellar Q2 earnings season, and a better than expected employment report.

But as earnings season winds down, and the latest jobs report becomes more distant in the rearview mirror, stocks took a pause.

There is no doubt the economy is strong. Even with renewed concerns over increasing virus cases threatening to slow the reopening.

One look at the jobs picture shows that. And with more jobs available than there are unemployed people to fill them, it looks like the robust pace of hiring will continue for quite some time.

But while economic growth is all around, some numbers have slipped a bit. Still growing, but maybe not quite as fast as had been expected.

Some of this was brought on by supply chain disruptions and worker shortages.

But with the enhanced unemployment benefits, which incentivized some workers to stay at home, expiring in September, we should soon see millions of new workers joining the workforce in the months ahead, and that should begin to bring relief to both of the aforementioned concerns, along with some inflation relief as well.

We should also soon get some insight on the fate of the $1.2 trillion infrastructure bill, and the $3.5 trillion budget framework, with the House returning to session this week.

That could inject another massive dose of spending into the economy.

But, of course, that will also likely come with tax proposals as well.

So traders will be watching these developments carefully.

In the meantime, we have a full slate of economic reports on deck this week starting with today' s Chicago Fed National Activity Index, the PMI Composite Flash report, and Existing Home Sales.

Tomorrow we' ll get the Redbook retail sales report, New Home Sales, and the Richmond Fed Manufacturing Index.

On Wednesday its MBA Mortgage Applications, Durable Goods Orders, and the State Street Investors Confidence Index.

Thursday we' ll get another look at Q2 GDP, Weekly Jobless Claims, Corporate Profits, and the Kansas City Fed Manufacturing Index.

And then of Friday, we' ll finish up with Personal Income and Outlays, Retail and Wholesale Inventories, and Consumer Sentiment.

We' ll also hear from Fed Chair Jerome Powell on Friday morning, as he speaks at the Jackson Hole, WY Economic Symposium, which has been moved online.

His speech on ' The Economic Outlook' will be closely watched.

Should be a busy week.

And with stocks trading near their all-time highs, it won' t take much to see them break out even higher."

As always, due diligence will prevail.

NB:

Correction from previous SNP 500 high of 4480 may be tested again.

Failing which, SNP 500 may fall back 200 to 300 points to test between 4180 to 4280 range.

Yet major support lies between 4100 and 4150.

All said, SNP 500 is still in a SECULAR BULL market and that any short term drawdown between 5% to 8% drop will not even derial its Primary Uptrend to eventually test Fibonacci 1% extension minimum 4600 and above by year end.

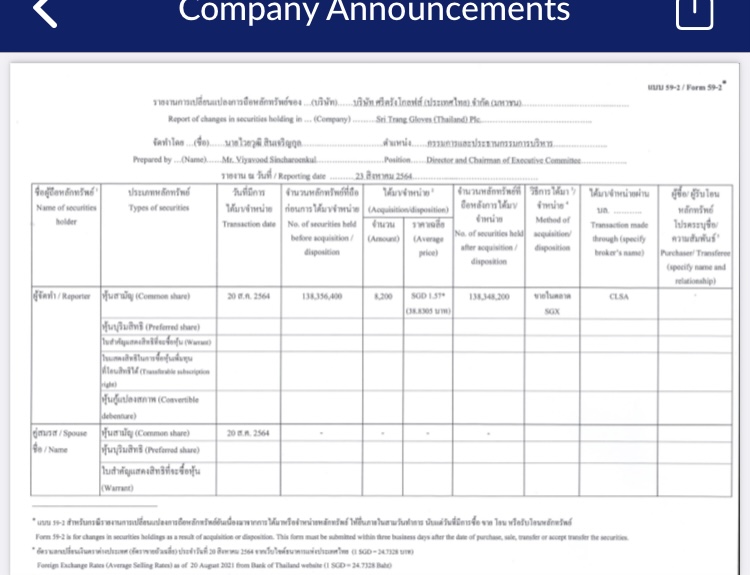

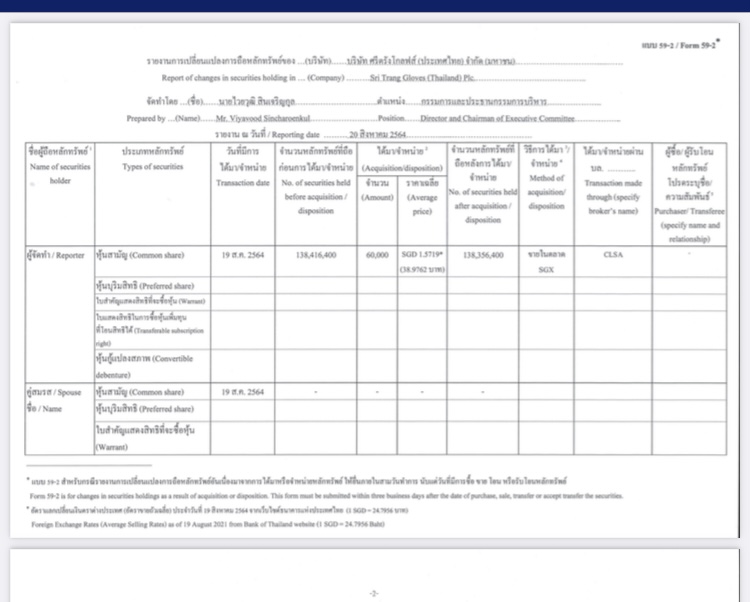

Dr Viyawood sell shares

你 们 到 底 有 几 个 ironman?

Stock futures were up during Asian hours after volatile week on Wall Street as investors eye a key event where the Federal Reserve could hint at prospects for tapering stimulus.

Futures tied to the Dow Jones Industrial Average inched up 138 points S& P 500 futures and Nasdaq 100 futures were both up by 16 points. and 59 points respectively.

Major averages were coming off a losing week as investors grew worried that the Fed?s potential move to pull back monetary stimulus could slow down the economic recovery that is already challenged by the spread of the delta Covid-19 variant.

The blue-chip Dow fell 1.1% last week, while the S& P 500 declined nearly 0.6%, breaking a two-week winning streak. The tech-heavy Nasdaq dipped 0.7% during the week.

?We suspect investor conviction is being challenged by the potential for upcoming monetary policy changes, shifting growth vs. value rotations, and a rising trajectory of new coronavirus cases,? Craig Johnson, technical market strategist at Piper Sandler, said in a note.

Traders are eagerly awaiting the Jackson Hole symposium for clues on the Fed?s timeline for dialing back its $120 billion a month bond-buying program.

The event takes place virtually on Thursday and Friday.

For the month of August, major benchmarks are poised to post modest gains.

The S& P 500 is up 1.1% month to date, while the blue-chip Dow has gained 0.5% and the Nasdaq has climbed 0.3%.

?August is a historically volatile month for markets and this year is no different, with investors currently climbing multiple walls of worries,? said Rod von Lipsey, managing director at UBS Private Wealth Management.

?Upticks in Covid-19 cases and a downward spiral in Afghanistan are creating a crisis of confidence, at a time when many investors are on holiday

Futures tied to the Dow Jones Industrial Average inched up 138 points S& P 500 futures and Nasdaq 100 futures were both up by 16 points. and 59 points respectively.

Major averages were coming off a losing week as investors grew worried that the Fed?s potential move to pull back monetary stimulus could slow down the economic recovery that is already challenged by the spread of the delta Covid-19 variant.

The blue-chip Dow fell 1.1% last week, while the S& P 500 declined nearly 0.6%, breaking a two-week winning streak. The tech-heavy Nasdaq dipped 0.7% during the week.

?We suspect investor conviction is being challenged by the potential for upcoming monetary policy changes, shifting growth vs. value rotations, and a rising trajectory of new coronavirus cases,? Craig Johnson, technical market strategist at Piper Sandler, said in a note.

Traders are eagerly awaiting the Jackson Hole symposium for clues on the Fed?s timeline for dialing back its $120 billion a month bond-buying program.

The event takes place virtually on Thursday and Friday.

For the month of August, major benchmarks are poised to post modest gains.

The S& P 500 is up 1.1% month to date, while the blue-chip Dow has gained 0.5% and the Nasdaq has climbed 0.3%.

?August is a historically volatile month for markets and this year is no different, with investors currently climbing multiple walls of worries,? said Rod von Lipsey, managing director at UBS Private Wealth Management.

?Upticks in Covid-19 cases and a downward spiral in Afghanistan are creating a crisis of confidence, at a time when many investors are on holiday

From Ironman work

Daily Update on My STA Proprietory Short Term Buying Zone Pivot at 32.48 Bahts ($1.325) and STA closing at 40.25 Bahts ($1.640) on 20th August 2021 is Above Neutral Zone of 39.04 Bahts ($1.593) as STA Thai is the Lead Market but 2nd Quarter Rubber Results including Profits from Associates and Joint Ventures of

US$30 million much Better than 1st Quarter Results of US$10 Milllion.

Understand 3rd Quarter Results STA will have a Marked to Market Inventory Gain which cannot be realised in 2nd Quarter Results of US$26.20 Million (839.1 Million Bahts) as per SET' s Accounting Practice.

Had the Marked to Market Inventory Gain been Realised in 2nd Quarters Profits, STA would have enjoyed higher Rubber Profits inclusive of Profits from Associates and Other Joint Venture Contributions of US$56.20 deriving at a Profits of US$186.20 which only Marginally Lower than 1st Quarter Results of US$191.00.

But Overall 2nd Quarters STA Results including Gloves Contribution came in at US$160 Million compared to First Quarter Results of US$191 Million (5959 Million Bahts) well below my Expectations of US$194.98 Million (6083 Million Bahts) due to Loss of Gloves Production of 900 million Gloves from Shutting Down of 2 Gloves Factories and Freight Issues Resulting in Delayed Shipment of Gloves beyond shipment month June.

STGT 2nd Quarters Profits of US$231 Million (7.28 Billion Bahts) well below 1st Quarter Results of US$322 Million (10,051 Million Bahts) Below my Expectations of US$290 Million (8845 Million Bahts) and Below Market Expectations of Some Analysts.

On 20th August 2021, STA' s NVDR Foreign Institutions Showing 0.22 Million+ Shares Net Sellers whilst STGT Showing Million 0.61 Shares Net Sellers.

For the Month of January 2021 to date STA NVDR Foreign Institutions showing 35.27 Million+ Shares Net Sellers (Shortist' s Included 205.30 Million+) and STGT NVDR showing 20.66 Million+ Shares Net Buyers (Shortists Included 104.65 Million+).

NVDR STA Foreign Institutions were Sellers whilst Local Institutions/Proprietory Trade/Local Individuals were Buyers (SHORTISTS Included).

Short Term to Intermediate Term (Less Volatility):

Corrective Downside Possibly Over with Potential Rebounce if STA Price Action can close 2 consecutive days above 42.50 Bahts.

Consolidation Range between 36.25 Bahts ($1.500) and 50.50 Bahts ($2.095).

Please Note that STA' s Price Action can only Reclaim its Short Term/Intermediate UPTREND provided STA can close above 50.50 bahts on 2 consecutive days.

Medium (Less Volatility) to Long Term (High Volatility):

Underlying Primary Uptrend on Earnings Visibility (Profit Making Company) for the Rest of 2021.

Negative Rubber/Gloves News Events or Even Rotation Play Between STA (Selling) and STGT (Buying) can Cause a Correction in the Market at Any Point in Time which Potentially can be Worse than Non Rubber/Gloves News Events like Global Stock Market Drop.

Other than that, Profit Taking in a Technically Overbought Market is Healthy to Correct Any Market Excesses but when Market Propels Higher in the Short Term with High Volatility, Correction may Potentially be Deeper than We may Think in the Event of Unsuspecting Servere Driven Negative News.

Into every Short Term/Intermediate Term New High, STA may Attract Profit Taking but we must be Realistic that any STA' s Price Rise is Never Linear and will be Subjected to Drawdown at Any Point in Time Along Its Upside Short/Intermediate Term Trend.

As Always, Due Diligence is Warranted on

Judgemental Call to Suit Own Risk Appetite.

NB:

As Much as I can Tell, Short/Intermediate Term Technicals ABC Pattern is trying to Form its (C) Low but Nobody Knows where is the Technical Low.

Whether 36.25 Bahts is the (C) Low of ABC Pattern has yet to be confirmed.

I Must Admit that the Further Price Drop in STA from the 42.00 bahts Support Mentioned recently has been Exercerbated by the Drop in Shanghai Rubber Futures Price to Test the Fibonacci 61.80% thereabout at 36.50 Bahts which STA tested a low of 36.25 Bahts on 13th July.

STA' s price drop to date to Recent Low is also partly being Influenced by the Recent Corrective Fall in Copper Prices as Evident by China' s Releasing Copper into the Market by China State Reserve Coupled with Falling Latex Demand Due to M' sian MCO Affecting Gloves Counters As Gloves Production Being Affected Dampening Rubber Sentiment but Recently Rubber Futures Prices have Rebounded from its Recent Low Price Low being Undepinned by Physical Tyre Grade Rubber Demand which has been Quite Strong to Date Resulting in Decent Margin for STA' s Rubber Division which is Expected to Continue for this 3rd Quarter July to September Rubber Sales Period.

According to Elliott Wave Theory the Wave 4 is Clearly Corrective. Prices may Meander Sideways for an Extended Period which is often Frustrating because of Lack of Progress in the Larger Trend.

As per Elliott Wave Theorist' s Rule of Thumb, if any Wave Labelling has been Violated, the Chart' s Techincian has to Relabel the Price Action to Reflect Realistic Market Direction (Please Note that Elliott Wave Reading is Not Engraved in Stone) as in Any Medium to Long Term Share Counter Outlook, Earnings will Still Hold the Key to STA' s Market Direction.

At Present Juncture of STGT 38.50 Bahts and STA at 40.25 Bahts Closing, STA' s Intrinsic Value is 40.45 Bahts which now STA is slightly discounted to STGT and yet STA' s EPS of 3.28 Much Higer than STGT' s EPS of 2.50.

STGT 38.50 Bahts × 2.872 Billion Issued Shares x 0.562% (STGT Earnings Contribution to STA) ÷ 1.536 Billion Issued Shares of STA to Derive at Intrinsic Value of STA at 40.45 Bahts.

On Top of STA' s Intrinsic Value of 40.45 Bahts, STA Midstream Natural Rubber Assets including 30+ Factories/Plantations/Land are being Valued at " ZERO" .

I do not View STA' s 2nd Released Result that Bad to Warrant Me to Make the Necessary Adjustment to My STA' s Portfolio Presently After having Analysed STA' s Financial Results Thoroughly.

The Mere Mention of HEMP' s Project Materialising by Year End 2021 by Few Thai Analysts Could have Fuelled this Slight Rebounce After Checking With STA' s Investor' s Department Who Confirmed the Project is Moving Along Fine but Yet Much Leg Work Needs to be Done as Mr Market is Normally Forward Looking.

Could the Mention of the HEMP' s Project by Management be the Catalyst for STA to Stage the Slight Rebounce Few Days Ago When Foreign NVDR Buyers bought 11.58 Million Shares on 11th August which I Shall Leave to Market Participants to Make Their Own Decision Whether This Rebounce Can be Sustained Leading to a Recovery in STA' s Short Term Price Action which had Yet to Be Determined by Mr Market.

Besides, STA' s Price has already Reacted Downwards to the 36.25 Bahts Level before Rebouncing but Its Results is not as Bad as most Analysts may have thought as yet STA 2nd Quarter Result is still Above One or Two Market Analysts' Expectations.

Only a US$31 Million down for 2nd Quarters Results compared to 1st Quarter Results but yet a Money Making company with Decent Dividend Payout to Date.

From My Priveleged Thai Informant, a Fair Value for STA' s Rubber Assets of Minimum 5 Bahts on Top of Its Intrinsic Value, has been Ascribed to

STA' s Rubber Division.

Yet, as a Medium to Long Term Investor, I am the least not Perturbed by any STA' s Short Term/Intermediate Term Whipsawing Price Action as I am Invested in a Fundamentally Sound Growth Stock with Potential Decent Dividend Payout for the 3rd Quarter Reporting as STGT specifically Expounded in their 2nd Quarter Results Report that Dividend will be paid out as well by STGT and I believe so as STA will enjoy likewise as it earns 56.2% contributions from STGT.

I still view STA will Enjoy Decent Profits and not a Loss Making Company for 3rd Quarter Results Reporting.

Idealistically, let' s hope all STA' s Iron Hand Medium to Long Term Investors Remain Steadfast to their 2 Cs (Conviction and Confidence) on the Improved Earnings Results of STGT on Resumption of their 2 Factories Operations Hit By Covid Spread Shutdown Recently and One Factory' s Expansion Coupled with another New Factory Fully Operational by 3rd Quarter and Another One in 4th Quarter to add Extra Gloves Capacity Moving Forward.

As Always, Due Diligence is Warranted to Suit Risk Appetite on Own Judgemental Call as Own Money, Own Target.

Daily Update on My STA Proprietory Short Term Buying Zone Pivot at 32.48 Bahts ($1.325) and STA closing at 40.25 Bahts ($1.640) on 20th August 2021 is Above Neutral Zone of 39.04 Bahts ($1.593) as STA Thai is the Lead Market but 2nd Quarter Rubber Results including Profits from Associates and Joint Ventures of

US$30 million much Better than 1st Quarter Results of US$10 Milllion.

Understand 3rd Quarter Results STA will have a Marked to Market Inventory Gain which cannot be realised in 2nd Quarter Results of US$26.20 Million (839.1 Million Bahts) as per SET' s Accounting Practice.

Had the Marked to Market Inventory Gain been Realised in 2nd Quarters Profits, STA would have enjoyed higher Rubber Profits inclusive of Profits from Associates and Other Joint Venture Contributions of US$56.20 deriving at a Profits of US$186.20 which only Marginally Lower than 1st Quarter Results of US$191.00.

But Overall 2nd Quarters STA Results including Gloves Contribution came in at US$160 Million compared to First Quarter Results of US$191 Million (5959 Million Bahts) well below my Expectations of US$194.98 Million (6083 Million Bahts) due to Loss of Gloves Production of 900 million Gloves from Shutting Down of 2 Gloves Factories and Freight Issues Resulting in Delayed Shipment of Gloves beyond shipment month June.

STGT 2nd Quarters Profits of US$231 Million (7.28 Billion Bahts) well below 1st Quarter Results of US$322 Million (10,051 Million Bahts) Below my Expectations of US$290 Million (8845 Million Bahts) and Below Market Expectations of Some Analysts.

On 20th August 2021, STA' s NVDR Foreign Institutions Showing 0.22 Million+ Shares Net Sellers whilst STGT Showing Million 0.61 Shares Net Sellers.

For the Month of January 2021 to date STA NVDR Foreign Institutions showing 35.27 Million+ Shares Net Sellers (Shortist' s Included 205.30 Million+) and STGT NVDR showing 20.66 Million+ Shares Net Buyers (Shortists Included 104.65 Million+).

NVDR STA Foreign Institutions were Sellers whilst Local Institutions/Proprietory Trade/Local Individuals were Buyers (SHORTISTS Included).

Short Term to Intermediate Term (Less Volatility):

Corrective Downside Possibly Over with Potential Rebounce if STA Price Action can close 2 consecutive days above 42.50 Bahts.

Consolidation Range between 36.25 Bahts ($1.500) and 50.50 Bahts ($2.095).

Please Note that STA' s Price Action can only Reclaim its Short Term/Intermediate UPTREND provided STA can close above 50.50 bahts on 2 consecutive days.

Medium (Less Volatility) to Long Term (High Volatility):

Underlying Primary Uptrend on Earnings Visibility (Profit Making Company) for the Rest of 2021.

Negative Rubber/Gloves News Events or Even Rotation Play Between STA (Selling) and STGT (Buying) can Cause a Correction in the Market at Any Point in Time which Potentially can be Worse than Non Rubber/Gloves News Events like Global Stock Market Drop.

Other than that, Profit Taking in a Technically Overbought Market is Healthy to Correct Any Market Excesses but when Market Propels Higher in the Short Term with High Volatility, Correction may Potentially be Deeper than We may Think in the Event of Unsuspecting Servere Driven Negative News.

Into every Short Term/Intermediate Term New High, STA may Attract Profit Taking but we must be Realistic that any STA' s Price Rise is Never Linear and will be Subjected to Drawdown at Any Point in Time Along Its Upside Short/Intermediate Term Trend.

As Always, Due Diligence is Warranted on

Judgemental Call to Suit Own Risk Appetite.

NB:

As Much as I can Tell, Short/Intermediate Term Technicals ABC Pattern is trying to Form its (C) Low but Nobody Knows where is the Technical Low.

Whether 36.25 Bahts is the (C) Low of ABC Pattern has yet to be confirmed.

I Must Admit that the Further Price Drop in STA from the 42.00 bahts Support Mentioned recently has been Exercerbated by the Drop in Shanghai Rubber Futures Price to Test the Fibonacci 61.80% thereabout at 36.50 Bahts which STA tested a low of 36.25 Bahts on 13th July.

STA' s price drop to date to Recent Low is also partly being Influenced by the Recent Corrective Fall in Copper Prices as Evident by China' s Releasing Copper into the Market by China State Reserve Coupled with Falling Latex Demand Due to M' sian MCO Affecting Gloves Counters As Gloves Production Being Affected Dampening Rubber Sentiment but Recently Rubber Futures Prices have Rebounded from its Recent Low Price Low being Undepinned by Physical Tyre Grade Rubber Demand which has been Quite Strong to Date Resulting in Decent Margin for STA' s Rubber Division which is Expected to Continue for this 3rd Quarter July to September Rubber Sales Period.

According to Elliott Wave Theory the Wave 4 is Clearly Corrective. Prices may Meander Sideways for an Extended Period which is often Frustrating because of Lack of Progress in the Larger Trend.

As per Elliott Wave Theorist' s Rule of Thumb, if any Wave Labelling has been Violated, the Chart' s Techincian has to Relabel the Price Action to Reflect Realistic Market Direction (Please Note that Elliott Wave Reading is Not Engraved in Stone) as in Any Medium to Long Term Share Counter Outlook, Earnings will Still Hold the Key to STA' s Market Direction.

At Present Juncture of STGT 38.50 Bahts and STA at 40.25 Bahts Closing, STA' s Intrinsic Value is 40.45 Bahts which now STA is slightly discounted to STGT and yet STA' s EPS of 3.28 Much Higer than STGT' s EPS of 2.50.

STGT 38.50 Bahts × 2.872 Billion Issued Shares x 0.562% (STGT Earnings Contribution to STA) ÷ 1.536 Billion Issued Shares of STA to Derive at Intrinsic Value of STA at 40.45 Bahts.

On Top of STA' s Intrinsic Value of 40.45 Bahts, STA Midstream Natural Rubber Assets including 30+ Factories/Plantations/Land are being Valued at " ZERO" .

I do not View STA' s 2nd Released Result that Bad to Warrant Me to Make the Necessary Adjustment to My STA' s Portfolio Presently After having Analysed STA' s Financial Results Thoroughly.

The Mere Mention of HEMP' s Project Materialising by Year End 2021 by Few Thai Analysts Could have Fuelled this Slight Rebounce After Checking With STA' s Investor' s Department Who Confirmed the Project is Moving Along Fine but Yet Much Leg Work Needs to be Done as Mr Market is Normally Forward Looking.

Could the Mention of the HEMP' s Project by Management be the Catalyst for STA to Stage the Slight Rebounce Few Days Ago When Foreign NVDR Buyers bought 11.58 Million Shares on 11th August which I Shall Leave to Market Participants to Make Their Own Decision Whether This Rebounce Can be Sustained Leading to a Recovery in STA' s Short Term Price Action which had Yet to Be Determined by Mr Market.

Besides, STA' s Price has already Reacted Downwards to the 36.25 Bahts Level before Rebouncing but Its Results is not as Bad as most Analysts may have thought as yet STA 2nd Quarter Result is still Above One or Two Market Analysts' Expectations.

Only a US$31 Million down for 2nd Quarters Results compared to 1st Quarter Results but yet a Money Making company with Decent Dividend Payout to Date.

From My Priveleged Thai Informant, a Fair Value for STA' s Rubber Assets of Minimum 5 Bahts on Top of Its Intrinsic Value, has been Ascribed to

STA' s Rubber Division.

Yet, as a Medium to Long Term Investor, I am the least not Perturbed by any STA' s Short Term/Intermediate Term Whipsawing Price Action as I am Invested in a Fundamentally Sound Growth Stock with Potential Decent Dividend Payout for the 3rd Quarter Reporting as STGT specifically Expounded in their 2nd Quarter Results Report that Dividend will be paid out as well by STGT and I believe so as STA will enjoy likewise as it earns 56.2% contributions from STGT.

I still view STA will Enjoy Decent Profits and not a Loss Making Company for 3rd Quarter Results Reporting.

Idealistically, let' s hope all STA' s Iron Hand Medium to Long Term Investors Remain Steadfast to their 2 Cs (Conviction and Confidence) on the Improved Earnings Results of STGT on Resumption of their 2 Factories Operations Hit By Covid Spread Shutdown Recently and One Factory' s Expansion Coupled with another New Factory Fully Operational by 3rd Quarter and Another One in 4th Quarter to add Extra Gloves Capacity Moving Forward.

As Always, Due Diligence is Warranted to Suit Risk Appetite on Own Judgemental Call as Own Money, Own Target.

Vizient Announces Agreement with Sri Trang Gloves to Improve Supply Assurance for Nitrile Gloves

August 16, 2021 06:00 AM Eastern Daylight Time

IRVING, Texas--(BUSINESS WIRE)--Vizient, Inc. today announced an agreement with Thailand-based Sri Trang Gloves for chemo-rated nitrile exam gloves as part of the Vizient Novaplus® Enhanced Supply program. Sri Trang is one of the world&rsquo s leading glove manufacturers and the agreement will bring additional supply assurance for this essential component of personal protective equipment required to safely deliver patient care.

.@Vizientinc announces agreement with Thailand-based Sri Trang Gloves for chemo-rated nitrile gloves as part of the Vizient Novaplus® Enhanced Supply program. Tweet this

Under the Novaplus Enhanced Supply program, suppliers are required to maintain certain levels of onshore inventory to mitigate supply disruptions and demand surges. The program also increases production transparency and greater demand predictability to drive production and supply resiliency.

As part of the agreement with Sri Trang, Vizient members will be able to commit to a monthly purchasing volume for nitrile gloves at any level and then have a matching 90-day, onshore supply maintained by Sri Trang specifically for that provider organization.

&ldquo As a result of the pandemic, Vizient members are looking for new ways to engage with manufacturers and distributors for supply assurance,&rdquo said Brent Gee, vice president of contract and program services for Vizient. &ldquo This agreement with Sri Trang will further ensure supply of nitrile gloves, which are essential for care delivery, in the event of demand spikes for this product.&rdquo

Established in 1987, Sri Trang&rsquo s operations span all sectors of the natural rubber industry, from rubber plantations and rubber processing to glove production. Currently, Sri Trang has 10 glove manufacturing facilities on 3 campuses in Thailand which produce 35 billion disposable glove pieces annually with exports to 160+ countries globally.

Sri Trang recently announced their intent to establish production in the U.S. The proposed 100-plus acre campus will serve as a North American hub for Sri Trang comprising a nitrile glove manufacturing facility, distribution center and warehouse, and administrative complex. Potential U.S. production is estimated to reach 2.5 billion nitrile gloves annually after the first full year of production. The facility will support Sri Trang&rsquo s existing operation in Tampa, Florida &ndash Sri Trang USA, Inc. &ndash and augment their east coast distribution centers.

About Vizient Novaplus

Novaplus Enhanced Supply Program, a Vizient sourcing program, contracts suppliers to provide additional inventory of essential products to mitigate supply disruptions and demand surge. Contract terms provide greater predictability and sustainability to drive continued production and supply resiliency. Production transparency requirements increase visibility to anticipate and further mitigate potential supply disruptions. By purchasing through Novaplus Enhanced Supply, health care facilities also receive expanded value and benefits built on the foundation of the industry&rsquo s longest-run private label program.

The Week On Wall Street: A 2-Day Growth Scare

Summary

1) Earnings season comes to a close and the positive results have kept this market very resilient.

2) Geopolitical issues make the headlines this week. Avoid the rhetoric, watch the price action.

3) Look under the hood of the latest retail sales report before jumping to a conclusion

Summary

1) Earnings season comes to a close and the positive results have kept this market very resilient.

2) Geopolitical issues make the headlines this week. Avoid the rhetoric, watch the price action.

3) Look under the hood of the latest retail sales report before jumping to a conclusion

Major U.S. stock averages rebounded Friday, but closed the week in red amid fears of the Federal Reserve pulling back its stimulus.

The Dow Jones Industrial Average gained 225.96 points, or nearly 0.7%, to 35,120.08. The S& P 500 added 0.8% to reach 4,441.67. The tech-heavy Nasdaq Composite rose about 1.2% to 14,714.66

All three major stock indexes finished the week lower. The Dow dipped 1.1% this week, while the S& P 500 shed nearly 0.6% and the Nasdaq Composite moved 0.7% lower.

?With Fed tapering coming while delta variant keeps spreading, the transition away from liquidity/policy regime to more mid-cycle markets means we may experience a bumpier ride ahead,? Barclays equity strategists said in a note.

?Market narrative may thus turn more cautious, as concerns about peaking growth rates, delta variant and policy mistake may prove headwinds, at a time when seasonality and technicals are unfavorable.?

Technology stocks traded in the green Friday, providing the market with support. Microsoft, Cisco and Salesforce were among the biggest winners in the Dow as investors snapped up tech stocks amid concerns about slowing economic recovery. Chip stocks rose, with Nvidia closing 5.1% higher.

Tesla shares added 1% after Elon Musk?s electric car maker had an AI day on Thursday. The company unveiled a new custom chip and plans to build a humanoid robot.

The stock was down nearly 5.2% lower for the week as investors worried about growth in China, one of the electric vehicle maker?s key markets.

This week, WTI crude oil tumbled more than 9%, taking energy stocks with it. Diamondback Energy and Valero Energy sunk nearly 9.9% and 9.1%, respectively, on the week.

Minutes from the Fed?s July meeting released this week showed the central bank is willing to start reducing its monthly asset purchases this year. Investors sold equities and commodities this week and bought bonds on fears the move by the Fed may upend a global economy already under stress by the delta variant.

August trading flows typically bring volatility with mostly lower volume, but the delta Covid variant also looms over markets.

?The spread of the delta variant is weighing on both consumption and productions, and pushing out growth,? Goldman Sachs? Chris Hussey said in a note.

Fed officials are set to gather for their annual meeting in Jackson Hole, Wyo., next week. Market participants will be awaiting insights into the Fed?s ?taper talks? as many central bankers aim to move away from easy policy.

The Dow Jones Industrial Average gained 225.96 points, or nearly 0.7%, to 35,120.08. The S& P 500 added 0.8% to reach 4,441.67. The tech-heavy Nasdaq Composite rose about 1.2% to 14,714.66

All three major stock indexes finished the week lower. The Dow dipped 1.1% this week, while the S& P 500 shed nearly 0.6% and the Nasdaq Composite moved 0.7% lower.

?With Fed tapering coming while delta variant keeps spreading, the transition away from liquidity/policy regime to more mid-cycle markets means we may experience a bumpier ride ahead,? Barclays equity strategists said in a note.

?Market narrative may thus turn more cautious, as concerns about peaking growth rates, delta variant and policy mistake may prove headwinds, at a time when seasonality and technicals are unfavorable.?

Technology stocks traded in the green Friday, providing the market with support. Microsoft, Cisco and Salesforce were among the biggest winners in the Dow as investors snapped up tech stocks amid concerns about slowing economic recovery. Chip stocks rose, with Nvidia closing 5.1% higher.

Tesla shares added 1% after Elon Musk?s electric car maker had an AI day on Thursday. The company unveiled a new custom chip and plans to build a humanoid robot.

The stock was down nearly 5.2% lower for the week as investors worried about growth in China, one of the electric vehicle maker?s key markets.

This week, WTI crude oil tumbled more than 9%, taking energy stocks with it. Diamondback Energy and Valero Energy sunk nearly 9.9% and 9.1%, respectively, on the week.

Minutes from the Fed?s July meeting released this week showed the central bank is willing to start reducing its monthly asset purchases this year. Investors sold equities and commodities this week and bought bonds on fears the move by the Fed may upend a global economy already under stress by the delta variant.

August trading flows typically bring volatility with mostly lower volume, but the delta Covid variant also looms over markets.

?The spread of the delta variant is weighing on both consumption and productions, and pushing out growth,? Goldman Sachs? Chris Hussey said in a note.

Fed officials are set to gather for their annual meeting in Jackson Hole, Wyo., next week. Market participants will be awaiting insights into the Fed?s ?taper talks? as many central bankers aim to move away from easy policy.

Dr Viyawood sell away the shares

leroy55 ( Date: 21-Aug-2021 01:01) Posted:

|

For the Benefit of New Readers to ISDN' s Thread:

ISDN' s short term market price action is down but

awaits for new catalyst for market to stabilise it but only we do not know how deep the correction will be but it may be deeper that what we may think.

Suspect there might be a potential rebounce due to oversold technical readings on certain daily technical tools but yet high possibility to consolidate before trying to cover EXHAUSTION GAP.

Seeing short term strong support below 0.60 technically as recent more than decent earnings release on 12th August will support ISDN' s downside as ISDN to date is a money making company.

Medium to long term investors just need to practise patience as no market is linear.

For those who have opted for dividend payout instead of taking scrips, just relax and enjoy coming payout.

For those who opted for scrips, they just need to be patient and may have to wait it out to enjoy eventual potential higher price appreciation down the road.

Due diligence is warranted always.

ISDN' s short term market price action is down but

awaits for new catalyst for market to stabilise it but only we do not know how deep the correction will be but it may be deeper that what we may think.

Suspect there might be a potential rebounce due to oversold technical readings on certain daily technical tools but yet high possibility to consolidate before trying to cover EXHAUSTION GAP.

Seeing short term strong support below 0.60 technically as recent more than decent earnings release on 12th August will support ISDN' s downside as ISDN to date is a money making company.

Medium to long term investors just need to practise patience as no market is linear.

For those who have opted for dividend payout instead of taking scrips, just relax and enjoy coming payout.

For those who opted for scrips, they just need to be patient and may have to wait it out to enjoy eventual potential higher price appreciation down the road.

Due diligence is warranted always.

A rising number of companies have also come under investigation or have been voluntarily suspended from trading for long periods of time, which he says is the stock market equivalent of a "black hole". Investors are left in the lurch holding "zombie companies".

According to a report from SGX, 56 stocks have been suspended from trading for 12 months or longer as at May this year, while another 9 stocks are set to be delisted in due course. This translates to about 10 per cent of counters currently listed on the bourse. In 2016 when SGX first started giving half-yearly updates of such stocks, there were only 20 stocks on this list.

Mr Nallakaruppan recalls his own experience with railway parts maker Midas Holdings, which shocked shareholders with litigation suits and enforcement orders. The stock has been suspended from trading since February 2018, but remains listed on SGX.

"It's sad when you see all your money wiped out like this, and all these affect investors' confidence overtime," he says. "This isn't like Monopoly money, it's real money that people are losing."

Delistings have also been on the rise, notes Maybank Kim Eng's (MBKE) chief executive Aditya Laroia. "Since 2012, delistings on SGX have outpaced new listings by 40 per cent," he notes. "This is largely driven by the limited niche, specialised sectors offered on SGX compared to other regional exchanges. Notable valuation discounts have been the result, encouraging delistings."

A lack of liquidity has prompted listed companies to head for privatisation, including BreadTalk, Fragrance Group and SK Jewellery.

SGX's latest financial results released on Aug 5 reflect some of these sentiments. SGX posted net profit of S$205.6 million for the second half of FY2021 ended June, down from S$258.6 million in the year-ago period. The group's H2 operating revenue fell 6.8 per cent year-on-year to S$535.1 million, with the decline coming from its equities segment, amid a fall in treasury and other revenue as well as trading and clearing revenue.

For the full FY2021, SGX's largest business segment, equities, saw operating revenue decline 7.7 per cent to S$701.1 million.

SGX market strategist Geoff Howie notes that STI constituent stocks typically "dominate" the inflows and outflows of the Singapore market in terms of market value. However, in July this year, only six out of the 30 stocks that saw the highest net institutional inflows were constituent stocks.

The health of the stock market is largely dependent on the authorities and regulators here, argues Mak Yuen Teen, a corporate governance advocate and associate professor at the National University of Singapore.

Prof Mak notes that 10 years ago, Singapore was home to more than 150 "S-chip" companies, or Chinese companies listed on SGX. This number is down to just 71 today, and could drop even further, he warns.

"Just over the first six months of this year, another six S-chips have disappeared. I am not saying they are all going to collapse, but I think we will continue to see more doing so," he says.

What was once an "S-chip problem" has spread to the rest of the market over the past few years. Big companies like Hyflux and Noble, Singapore-based companies like Best World and Trek 2000, and Eagle Hospitality Trust are some of the names that have collapsed, wiping out investors' money along with them.

Mom-and-pop investors also have limited protection in the market, notes Prof Mak, and may not have the resources to make up for losses. As such, the bourse regulator needs to do more to protect the interests of these investors in terms of holding relevant parties responsible for stock market scandals. These include the likes of company directors, issue managers, sponsors and auditors.

"While SGX Regco has strengthened certain rules and improved its surveillance, and there are signs of them and other regulators stepping up, we have yet to see results," says Prof Mak.

"We should aim for a market with good quality companies, not aim to increase the number of listings regardless of quality."

Changing investment landscape

According to a report from SGX, 56 stocks have been suspended from trading for 12 months or longer as at May this year, while another 9 stocks are set to be delisted in due course. This translates to about 10 per cent of counters currently listed on the bourse. In 2016 when SGX first started giving half-yearly updates of such stocks, there were only 20 stocks on this list.

Mr Nallakaruppan recalls his own experience with railway parts maker Midas Holdings, which shocked shareholders with litigation suits and enforcement orders. The stock has been suspended from trading since February 2018, but remains listed on SGX.

"It's sad when you see all your money wiped out like this, and all these affect investors' confidence overtime," he says. "This isn't like Monopoly money, it's real money that people are losing."

Delistings have also been on the rise, notes Maybank Kim Eng's (MBKE) chief executive Aditya Laroia. "Since 2012, delistings on SGX have outpaced new listings by 40 per cent," he notes. "This is largely driven by the limited niche, specialised sectors offered on SGX compared to other regional exchanges. Notable valuation discounts have been the result, encouraging delistings."

A lack of liquidity has prompted listed companies to head for privatisation, including BreadTalk, Fragrance Group and SK Jewellery.

SGX's latest financial results released on Aug 5 reflect some of these sentiments. SGX posted net profit of S$205.6 million for the second half of FY2021 ended June, down from S$258.6 million in the year-ago period. The group's H2 operating revenue fell 6.8 per cent year-on-year to S$535.1 million, with the decline coming from its equities segment, amid a fall in treasury and other revenue as well as trading and clearing revenue.

For the full FY2021, SGX's largest business segment, equities, saw operating revenue decline 7.7 per cent to S$701.1 million.

SGX market strategist Geoff Howie notes that STI constituent stocks typically "dominate" the inflows and outflows of the Singapore market in terms of market value. However, in July this year, only six out of the 30 stocks that saw the highest net institutional inflows were constituent stocks.

The health of the stock market is largely dependent on the authorities and regulators here, argues Mak Yuen Teen, a corporate governance advocate and associate professor at the National University of Singapore.

Prof Mak notes that 10 years ago, Singapore was home to more than 150 "S-chip" companies, or Chinese companies listed on SGX. This number is down to just 71 today, and could drop even further, he warns.

"Just over the first six months of this year, another six S-chips have disappeared. I am not saying they are all going to collapse, but I think we will continue to see more doing so," he says.

What was once an "S-chip problem" has spread to the rest of the market over the past few years. Big companies like Hyflux and Noble, Singapore-based companies like Best World and Trek 2000, and Eagle Hospitality Trust are some of the names that have collapsed, wiping out investors' money along with them.

Mom-and-pop investors also have limited protection in the market, notes Prof Mak, and may not have the resources to make up for losses. As such, the bourse regulator needs to do more to protect the interests of these investors in terms of holding relevant parties responsible for stock market scandals. These include the likes of company directors, issue managers, sponsors and auditors.

"While SGX Regco has strengthened certain rules and improved its surveillance, and there are signs of them and other regulators stepping up, we have yet to see results," says Prof Mak.

"We should aim for a market with good quality companies, not aim to increase the number of listings regardless of quality."

Changing investment landscape

A GOOD READ ON THE US STOCK MARKET BY A 3RD PARTY ANALYST:

"Stocks finished mixed yesterday with the Dow off modestly, while the S&P and Nasdaq were up modestly.

But all three of those indexes were up solidly from their worst levels of the day.

News on Wednesday that the Fed was considering tapering by the end of the year weighed on stocks then and yesterday morning.

But the markets were able to shrug that off by the end of the day.

The taper talk was not really much of a surprise since the Fed had been hinting at that for months.

Some have begun pointing to some lighter than expected numbers in some economic reports too.

To be sure, some numbers have missed their expectations.

But others have easily surpassed them.

One thing traders are anxious to see get here is the end of the enhanced unemployment benefits in September.

That will begin to alleviate supply chain disruptions, worker shortages, and inflation. (For employers, it can't come soon enough.)

While last month's better than expected employment report showed 943K new jobs being created, those numbers are expected to soar even higher as millions more return to the workforce in the coming months.

And that's great news for everybody.

In other news, Weekly Jobless Claims fell more than expected with -29,000 fewer new claims at 348K.

The Philadelphia Fed Manufacturing Index came in weaker than expected at 19.4 vs. last month's 21.9 and views for 25.0.

But the Leading Indicators report came in stronger than expected with a m/m gain of 0.9% vs. last month's 0.5% and the consensus for 0.8%.

Stocks are currently lower for the week with one trading day left.

And we'd need to see a sizable gain to turn that around today.

But pullbacks can also be opportunities to pick up more of your favorite stocks, or get into new ones, at even better prices.

Because with strong growth forecasts for the rest of the year, it looks like there's a lot more upside to go."

As always, due diligence is warranted.

NB:

Suspect recent all time high at 4480 is the temporary top for SNP 500.

Minor support now located at 4350. Any breakdown below that level will likely exacerbate further drop to test major support between 4100 and 4150 but high possibility of basing out for a rally thereafter to test my year end target of 4600 minimum Fibonacci 1% Extension.