SIA

Last:6.89

-0.08

-0.08

Drill Baby Drill

Post Reply

21-40 of 95

Post Reply

21-40 of 95

Due Diligence is warranted. For record, i hope binder is looking too

Airline industry benefitting from lower oil price: IATA head

The global aviation industry is benefitting from lower oil prices because they&rsquo re bringing down the cost of kerosene, the head of the IATA industry association said.

The reduction in oil prices is in turn helping drive down ticket prices, said Willie Walsh, the director general of the International Air Transport Association.

&ldquo It&rsquo s typically our single biggest cost, so it would help to offset any weakening demand if we were to witness a slowdown,&rdquo Walsh said in an interview with Bloomberg Television at IATA&rsquo s annual general meeting in New Delhi. &ldquo It also tends to have an impact on pricing. There&rsquo s almost a direct correlation between the price of oil and and the price of airline tickets.&rdquo

Airlines have become increasingly cautious about the demand outlook as global economic dislocations prompted by US President Donald Trump&rsquo s tariffs hurt demand. At the same time, a diminished economic outlook has also depressed oil prices, providing a cost advantage for carriers.

Walsh said that while lower ticket prices typically stimulate demand, it also &ldquo clearly drives down the overall revenue for the industry&rdquo .

Global aviation executives are meeting in New Delhi over the next few days to discuss the state of the industry. Walsh is set to unveil his formal outlook for profitability and revenue for the airline industry on Monday.

Fed out want to sell yet MAS is stock picking sgx counter to boost its market share in q3. Tolan.

If I hold it , it may sell down in view of technical recession or like another black Monday bcz of Japanese hiking yield. Yet MAS will take advantage to buy low n push it high

If I sell, any time this stock will push it to higher bcz of market sentiment clearly favor air industry after T5 airport opening and ceo confirm no tariff cost effect.

I have made selling call twice only to cancel

Next week shld break out above 700.

If not hold another month.

Worse, hold till dividend.

expect to see go back to previous price.

it has been happening this way

RPT - SIA Engineering Company Ltd - SIA Engineering Company Signs S$1.3 Bln Services Agreements With Singapore Airlines and Scoot

Don' t think anything anyone gain or lose lo.

just take with pinch of salt. market beater always wants us to believe what they say

for all we know, it could be other reason

BinderyT ( Date: 19-May-2025 15:13) Posted:

Ok, thanks. Surprising as T5 was announced awhile ago.

dontbetray ( Date: 19-May-2025 13:18) Posted:

simple summary of the market update:

Aviation Stocks Rise:

-

Singapore Airlines (SIA): Reported record revenue ($19.5B) and net profit ($2.8B) for FY2025. Despite strong results, shares rose just 2.4% to $6.90. Bonus for staff is 7.45 months, slightly lower than last year. Dividends also decreased from 48 to 40 cents per share.

-

SIA Engineering: Shares climbed over 7% to $2.42. Net profit surged 43.8% to $139.6M, driven by higher demand for maintenance services. Dividend increased to 9 cents per share.

-

Sats: Shares gained 2.8% to $2.99. Announced a $250M investment in upgrading ground and cargo operations at Changi Airport, in line with plans for Terminal 5 and Changi East.

Overall, the aviation sector is benefiting from strong travel demand and infrastructure growth

|

|

|

|

Ok, thanks. Surprising as T5 was announced awhile ago.

dontbetray ( Date: 19-May-2025 13:18) Posted:

simple summary of the market update:

Aviation Stocks Rise:

-

Singapore Airlines (SIA): Reported record revenue ($19.5B) and net profit ($2.8B) for FY2025. Despite strong results, shares rose just 2.4% to $6.90. Bonus for staff is 7.45 months, slightly lower than last year. Dividends also decreased from 48 to 40 cents per share.

-

SIA Engineering: Shares climbed over 7% to $2.42. Net profit surged 43.8% to $139.6M, driven by higher demand for maintenance services. Dividend increased to 9 cents per share.

-

Sats: Shares gained 2.8% to $2.99. Announced a $250M investment in upgrading ground and cargo operations at Changi Airport, in line with plans for Terminal 5 and Changi East.

Overall, the aviation sector is benefiting from strong travel demand and infrastructure growth

|

|

simple summary of the market update:

Aviation Stocks Rise:

-

Singapore Airlines (SIA): Reported record revenue ($19.5B) and net profit ($2.8B) for FY2025. Despite strong results, shares rose just 2.4% to $6.90. Bonus for staff is 7.45 months, slightly lower than last year. Dividends also decreased from 48 to 40 cents per share.

-

SIA Engineering: Shares climbed over 7% to $2.42. Net profit surged 43.8% to $139.6M, driven by higher demand for maintenance services. Dividend increased to 9 cents per share.

-

Sats: Shares gained 2.8% to $2.99. Announced a $250M investment in upgrading ground and cargo operations at Changi Airport, in line with plans for Terminal 5 and Changi East.

Overall, the aviation sector is benefiting from strong travel demand and infrastructure growth

ah bear and blunderyt, i notice you all following my counter call. why ah?

ChatGPT said:

Singapore Airlines (SIA) is currently navigating a complex economic landscape with a mix of positive and challenging factors.

✈ ️ Singapore Airlines: Financial Performance

In the fiscal year ending March 31, 2025, SIA reported a record net profit of

S$2.78 billion, bolstered by a

S$1.1 billionnon-cash accounting gain from the merger of its 49%&ndash owned Indian carrier Vistara with Air India.

Reuters+1CNA+1

However, the airline' s

operating profit declined by 37% to

S$1.71 billion, primarily due to increased competition leading to a

5.5% drop in passenger yields. Despite these challenges, SIA' s total revenue grew by

2.8% year-on-year to

S$19.54 billion, driven by resilient demand in both passenger and cargo segments.

ReutersNasdaq+1AeroTime+1

🛢 ️ Oil Prices: Trends and Implications

As of mid-May 2025,

Brent crude oil prices have decreased by approximately

12% since the beginning of the year, trading around

$65.41 per barrel. This decline is attributed to factors such as increased OPEC+ production and economic uncertainties stemming from U.S.-China trade tensions.

Trading Economics

For airlines like SIA, lower oil prices can reduce operating costs. However, SIA employs fuel hedging strategies, which may delay the immediate benefits of falling oil prices.

📊 Overall Assessment

While SIA faces challenges such as increased competition and fluctuating oil prices, its strong financial position, strategic investments, and operational agility position it well to navigate the current economic environment.

No material impact from tariffs on bookings for now: SIA CEO

[SINGAPORE] Singapore Airlines (SIA) : C6L+0.29%has not seen any significant impact of the US tariff turmoil on its bookings for now, chief executive Goh Choon Phong said at its financial results briefing on Friday (May 16).

He said: &ldquo At this point in time, based on what we can see in bookings, we do not see any significant impact, any material impact. So we are still seeing robust demand on our routes... It is really very uncertain. I don&rsquo t think anybody will tell you exactly what will happen.&rdquo

However, he said the carrier group has the nimbleness and agility to manage the uncertainties ahead.

Giving an example, he said: &ldquo In the days immediately after the implementation of the US tariff on China... we were able to fill our Singapore-USA flights with cargoes from South-east Asia rather than from China, where it was more greatly impacted.&rdquo

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

Lee added that the passenger flights to the US were holding up well.

SIA had 145 passenger planes and seven freighters, while its budget airline Scoot had 53 passenger aircraft, serving the group passenger network of 128 destinations and cargo network of 132 destinations as at Mar 31.

The airline group on Thursday posted revenue of S$10 billion for the

second half of FY2025 ended March, a gain of 1.9 per cent year on year (yoy), breaking the half-year record of S$9.9 billion in the year-ago period.

Net profit surged 65 per cent to S$2 billion as the group chalked up a S$1.1 billion one-off, non-cash accounting gain from the Air India-Vistara merger.

In 2024, Vistara was merged with Air India, resulting in SIA holding a 25.1 per cent share in the merged entity. Vistara was a 49 per cent associated company of the Singapore airline, before the corporate action took place.

Stripped of that gain, earnings would have been 24 per cent lower yoy at S$938.1 million.

Net profit for the full year would similarly have been lower &ndash by 37.2 per cent &ndash at S$1.7 billion, instead of the record S$2.8 billion, without the one-off gain.

SIA&rsquo s operating profit dipped 22.1 per cent to S$914 million, due to increased expenditure and lower yields.

Competition pushed yields down by 4.5 per cent for passenger and 2.1 per cent for cargo in the second half of FY2025. Group passenger load factor was 0.5 percentage point lower at 86.8 per cent, while the cargo load factor fell 1.4 percentage points to 54.9 per cent.

However, Lee said at the Friday briefing that passenger yield erosion has slowed in FY2025.

SIA, meanwhile, has not seen its mainland Chinese market recover to pre-pandemic levels, although inbound travel into the North Asian country has improved, with the load factor for Chinese flights rising to more than 80 per cent the last six months &ndash up from about 70 per cent last year.

The full-service carrier&rsquo s present capacity for the mainland Chinese market is largely on a par with pre-pandemic levels, while Scoot&rsquo s has recovered to about 80 per cent.

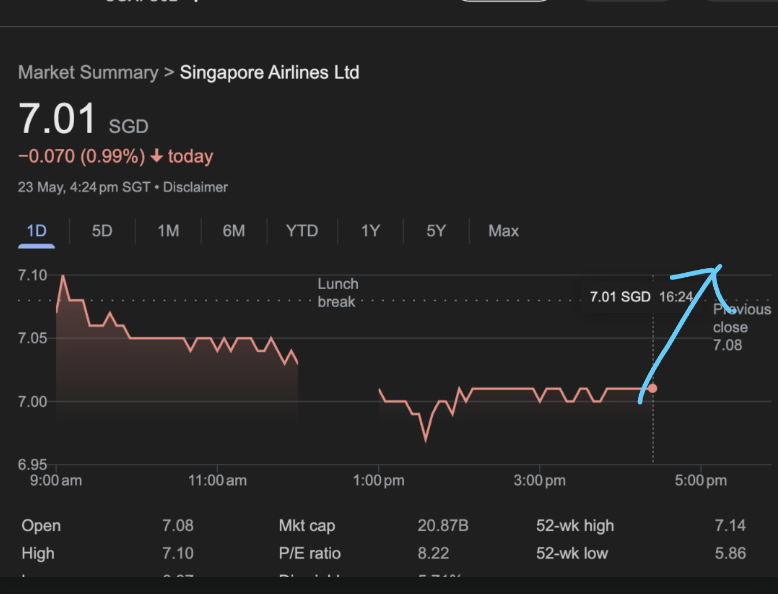

Shares of SIA closed S$0.02 or 0.3 per cent higher at S$6.90 on Friday.

Singapore welcomed hefty 1.4 million tourists in April, marking 4.5% YoY increase

The Singapore Tourism Board (STB) has revealed that the country welcomed 1.4 million tourists in April. This marks a sizeable 4.5% increase compared to the same period last year.

The month-on-month growth was also notable, with April&rsquo s arrivals rising by 7.7% from March. STB&rsquo s data suggests steady post-pandemic recovery in the travel sector as visitor numbers continue to climb.

Between January and April this year, a total of 5.71 million tourists visited the city-state, representing a 1.2% increase over the same four-month period in 2024.

Tourists from Indonesia made up the largest group of arrivals in April, followed closely by those from mainland China and India. However, when looking at cumulative figures for the year so far, mainland China remains Singapore&rsquo s top source of visitors, with 1.04 million Chinese tourists arriving from January to April.

Indonesia came in second place for year-to-date arrivals, while Australia rounded out the top three.

Industry observers say the consistent growth is a positive sign for Singapore&rsquo s hospitality and retail sectors, particularly ahead of the mid-year holiday season.

STB is expected to continue ramping up marketing efforts in key markets such as China and India to further boost inbound travel.

ChatGPT said:

Here&rsquo s a concise summary of the key points from the article about Singapore Airlines (SIA):

Financial Performance:

-

Record net profit: $2.8 billion for FY ending March 31, 2025.

-

Boosted by: A one-off, non-cash gain of $1.1 billion from the Air India-Vistara merger.

-

Revenue: Up 2.8% to $19.54 billion.

Staff Bonus:

-

Bonus payout: 7.45 months&rsquo bonus under profit-sharing scheme.

-

Slightly lower than last year&rsquo s 7.94 months.

Operational Highlights:

-

Passengers carried: Record 39.4 million (+8.1%).

-

Passenger yields: Down 5.5% due to competition.

-

Cargo revenue: Up $94 million (+4.4%) from e-commerce, perishables, and sea freight disruptions.

Dividends:

-

Total dividend: 40 cents/share (includes interim 10 cents) final 30 cents to be paid in August (pending approval).

-

Total payout: $1.2 billion.

Strategic Developments:

-

25.1% stake in merged Air India.

-

Fleet: 205 aircraft (78 more on order).

-

Network: 128 destinations in 36 countries.

-

New routes & upgrades: Includes Brisbane, Vienna, and enhanced lounges and cabin products.

Outlook:

-

Challenges: Tariff shifts, geopolitics, economic uncertainties, and supply constraints.

-

Opportunities: Growing Asia-Pacific market, dual-brand strategy (SIA + Scoot), and tech investment including AI

ChatGPT said:

Overall,

very good &mdash but with some caveats:

Why it' s good:

-

Record profit: $2.8B is the highest in SIA&rsquo s history.

-

Strong revenue: $19.54B despite global uncertainties.

-

Generous staff bonus: 7.45 months shows strong performance and staff recognition.

-

Dividend payout: $1.2B to shareholders is a sign of financial health.

-

Passenger and cargo growth: Demand remains strong.

-

Strategic gains: Stake in Air India, new routes, and heavy investment in premium products and tech.

Points to watch:

-

Profit partly from one-off gain: $1.1B was non-cash from the Air India-Vistara merger.

-

Passenger yields dropped: Lower earnings per km due to intense competition.

-

Growth challenges: Capacity expansion outpaced traffic growth.

-

Future uncertainty: Global trade tensions and economic risks could impact future earnings.

Verdict: Very positive overall &mdash a strong year operationally and financially, though future growth may face some headwinds.

SIA posts record $2.8 billion full-year profit staff to get 7.45 months&rsquo bonus

SIA' s record profit was boosted by a one-off non-cash accounting gain of $1.1 billion from the Air India-Vistara merger.ST PHOTO: LIM YAOHUI

SINGAPORE &ndash Singapore Airlines (SIA) has posted a record $2.8 billion net profit for the year ended March 31 and is said to be rewarding staff with a profit-sharing bonus of 7.45 months.

Its record profit was boosted by a one-off non-cash accounting gain of $1.1 billion from the

Air India-Vistara merger, it said in a filing on the Singapore Exchange on May 15.

Group revenue also climbed 2.8 per cent from the year before to hit a record $19.54 billion, driven by resilient demand for air travel and cargo uplift, it added.

In response to queries from The Straits Times on staff bonus, SIA said it can confirm that employees will receive a profit-sharing bonus in recognition of their dedication and hard work in FY2024-25.

&ldquo This is based on a longstanding formula that has been agreed with our staff unions,&rdquo SIA said, without disclosing details of the formula and bonus.

The 7.45 months&rsquo bonus is slightly lower than the

7.94 months for the year before.

The Air India-Vistara merger was completed in November 2024.

Before the merger, Vistara was jointly owned by Tata Sons and SIA. After the merger, SIA holds a 25.1 per cent stake in the enlarged Air India, allowing it to participate directly in the fast-expanding Indian aviation market.

SIA and its budget airline Scoot also carried a record 39.4 million passengers, up 8.1 per cent, it said.

Despite carrying more passengers, passenger yields &ndash the amount earned per passenger for each kilometre flown &ndash dipped 5.5 per cent to 10.3 cents per revenue passenger-kilometre.

This was amid intensified competition due to industry-wide capacity injection, SIA said.

Passenger traffic growth, which stood at 6.4 per cent, also lagged behind its capacity expansion of 8.2 per cent.

Meanwhile, its cargo flown revenue improved by $94 million, or 4.4 per cent, buoyed by the strong demand for e-commerce and perishables, as well as the spillover from disruptions to sea freight.

SIA&rsquo s board of directors recommended a final dividend of 30 cents per share for the full year.

Including the interim dividend of 10 cents per share paid on Dec 11, 2024, the total dividend for the year will be 40 cents per share, representing a total dividend distribution of $1.2 billion for the year.

The final dividend, which is subject to shareholders&rsquo approval, will be paid on Aug 27.

Looking ahead, SIA said the global airline industry faces a challenging operating environment amid changing tariff policies and trade tensions, economic and geopolitical uncertainties, and continued supply chain constraints.

&ldquo These factors may impact consumer and business confidence, potentially affecting both passenger and cargo markets,&rdquo it added.

&ldquo The group remains vigilant, closely monitoring developments and prepared to respond swiftly to market conditions.&rdquo

On a positive note, SIA said shifts in global passenger and trade flows may open new opportunities for the group, with its well-diversified global passenger and cargo network.

It added that its hub in Singapore offers a strategic advantage, given its position at the centre of growing economies in South-east Asia, South Asia and the wider Asia-Pacific region, and the group&rsquo s strong presence in these markets.

&ldquo The group&rsquo s dual-brand strategy, which leverages both SIA and Scoot, provides it with the flexibility to offer customers a wide range of options while responding nimbly to market dynamics,&rdquo it said.

It is also prepared to partner other airlines to open up growth opportunities, particularly in the Asia-Pacific region.

&ldquo Continued focus on product leadership and service excellence, including investments in next-generation aircraft, new cabin products and airline lounges, will help the group&rsquo s airlines maintain their competitive edge by providing customers with more value and enhancing the end-to-end travel experience,&rdquo SIA said.

The group&rsquo s operating fleet stands at a total of 205 aircraft as at March 31. SIA operates 145 passenger aircraft and seven freighters, while Scoot has 53 passenger aircraft. As at May 1, the group has 78 aircraft on order.

Its passenger network also covered 128 destinations in 36 countries and territories as at March 31.

SIA will increase services to Brisbane, Colombo, Jakarta, Johannesburg, London (Gatwick), Manila and Seattle for the operating season from March to October.

Meanwhile, Scoot

launched services to Iloilo City in April and will begin operations to Vienna in June.

SIA will also start

revenue-sharing flights with All Nippon Airways (ANA) between Japan and Singapore from September, with the joint fare products for these services going on sale in May.

To bolster its premium positioning, SIA has

announced a $1.1 billion investment to install all-new cabin products across its Airbus A350-900 long-haul and ultra-long-range fleet, including the debut of its new First Class cabin in seven A350-900 ultra-long-range aircraft.

It also

announced a $45 million transformation of its SilverKris and KrisFlyer Gold lounges at Singapore Changi Airport Terminal 2, to provide more space, upgraded facilities and more food and beverage options.

The group also continues to invest in its digital capabilities, including generative artificial intelligence, giving it an edge in the competitive aviation landscape, SIA said.

SIA shares closed 0.3 per cent, or two cents, higher at $6.88 on May 15, before its financial results were announced.

ChatGPT said:

Overall, the

April 2025 results are positive for Singapore Airlines Group. Here' s a quick evaluation:

Good:

-

Passenger traffic increased by 4.8%, showing solid demand.

-

Passenger load factor (PLF) improved to a high 87.9%, indicating efficient use of capacity.

-

Scoot' s PLF at 91.4% is especially strong.

-

3.4 million passengers carried &mdash up 6.4%, outpacing capacity growth.

-

Scoot expansion with a new route to Iloilo City supports network growth.

Not So Good:

-

Cargo performance was weaker:

-

Cargo load grew 4.0%, but capacity rose 6.6%.

-

This led to a drop in cargo load factor by 1.5 percentage points to 57.1%.

-

SIA suspended its route to Houston, which could indicate weak demand or route restructuring.

Conclusion:

Positive overall, especially on the passenger side. Cargo performance was mixed, but not alarming. The Group appears to be managing growth well.

ChatGPT said:

Here&rsquo s a concise summary of the two key announcements made by

Singapore Airlines (SIA), pursuant to Rule 706A of the SGX Listing Manual, for the period

1 October 2024 to 31 March 2025:

A. Merger of Vistara (TATA SIA Airlines) and Air India

-

On 12 Nov 2024, Vistara (49% owned by SIA) merged with Air India (AI).

-

Post-merger, SIA holds 25.1% in the enlarged Air India, which includes Air India Express and a 50% stake in Air India SATS.

-

Consideration:

-

SIA gave up its 49% stake in Vistara and

-

Paid INR 20.585 billion (approx. SGD 360 million) in cash.

-

The valuation considered strategic rationale, invested capital, and future prospects.

-

Funded using SIA&rsquo s internal resources.

-

Net Asset Value (NAV) changes:

-

Vistara stake:

-

SGD 110M (as of 31 Mar 2022), SGD 0 (as of 30 Sep 2022)

-

SIA' s 25.1% in AI:

-

SGD 596.38M (Mar 2022, pro forma),

-

SGD 340.11M (Sep 2022, pro forma),

-

SGD 2,024.6M (Mar 2025)

-

Air India is now an associate company of SIA.

B. Acquisition of Remaining Shares in KrisShop Pte. Ltd. (KSPL)

-

On 5 Mar 2025, SIA acquired 2,047,502 shares in KSPL from SATS Ltd. for:

-

SGD 1 (share purchase), and

-

SGD 2.25 million (to take over SATS&rsquo outstanding loan to KSPL)

-

Funded through internal resources.

-

NAV of acquired shares: SGD 0.3 million (as at 31 Mar 2025)

-

KSPL is now a wholly owned subsidiary of SIA.

-

The transaction has no material impact on SIA&rsquo s EPS or NTA.

-

No interested persons involved.

Let me know if you&rsquo d like this turned into a presentation slide or further simplified.

You said:

ChatGPT said:

Here' s a quick assessment of whether the announcements are

good or bad for SIA:

A. Merger with Air India &ndash Generally Positive

Good:

-

SIA exchanged a 49% stake in Vistara (which had zero NAV as of Sep 2022) for a 25.1% stake in a much larger Air India group with a NAV of over SGD 2 billion by Mar 2025.

-

It gives SIA exposure to India&rsquo s fast-growing aviation market through a stronger partner.

-

The investment (SGD 360M) was funded internally &ndash no debt or equity dilution.

-

Potential for long-term returns and strategic synergies with Tata Group.

Risks:

-

Air India is still in a turnaround phase &ndash future performance depends on integration success and market competition.

-

SIA now holds a minority stake (25.1%), meaning less control.

Verdict: Generally positive &ndash smart long-term positioning in India.

B. Full Acquisition of KrisShop &ndash Neutral to Slightly Positive

Good:

-

Acquired the rest of KrisShop for a symbolic price (SGD 1) and took over a SGD 2.25M loan.

-

Now has full control of KrisShop, allowing strategic alignment with SIA&rsquo s broader retail and loyalty plans.

Risks:

-

KSPL&rsquo s NAV was only SGD 0.3M, implying limited current value.

-

Slight cost, but small in SIA&rsquo s financial context.

Verdict: Neutral to slightly positive &ndash small deal, low cost, potential longer-term benefit.

Overall Verdict: Good

SIA made a

strategic move into India&rsquo s aviation future and took full control of a smaller subsidiary at low cost. The merger is the more significant and positive of the two.

today announcement,should expect good results,buy to hold

| 15 May 2025 |

Announcement of FY2024/25 Fourth Quarter and Full Year Results |

dontbetray ( Date: 09-May-2025 22:55) Posted:

ChatGPT said:

Yes, Scoot&rsquo s expansion is generally good news for Singapore Airlines (SIA) for several key reasons:

1. Revenue Growth

More flights and higher capacity mean more ticket sales and revenue. As Scoot is a wholly owned subsidiary, this directly contributes to SIA Group&rsquo s overall earnings.

2. Market Share Expansion

By increasing frequency and capacity, Scoot can capture more market share, especially in high-growth regions like Southeast Asia and Australia. This helps SIA defend and expand its presence in the budget travel segment.

3. Fleet Optimization

Deploying larger aircraft like the Boeing 787 Dreamliner increases passenger capacity with fewer flights, improving fuel efficiency and reducing cost per seat&mdash enhancing profitability.

4. Meeting Travel Demand

Strong demand for regional travel post-pandemic is a positive trend. Scoot&rsquo s responsiveness to this demand strengthens SIA&rsquo s competitive edge compared to other regional carriers.

5. Brand Synergy

As Scoot grows, it indirectly boosts SIA&rsquo s brand ecosystem, allowing cross-selling, loyalty programs, and improved customer flow between budget and full-service offerings.

Stock Market Reflection: The slight uptick in SIA&rsquo s share price (+0.30%) might reflect investor confidence in this strategy.

|

|

Expedia Stock Tumbles After Q1 Report. Weak U.S. Travel Demand Is Weighing On Bookings.

Expedia Group (

EXPE) stock tumbled early Friday after the company reported mixed first quarter results and lowered its sales outlook, citing " weaker than expected" U.S. travel demand.

The results prompted a downgrade from one Wall Street analyst and have Expedia stock down more than 10% at 151.25 in recent premarket action on the

stock market today.

The Seattle-based Expedia said in a news release Thursday that Q1 adjusted earnings increased 90% to 40 cents per share for its March quarter, ahead of expectations of 35 cents per share. Revenue increased 3% to $2.99 billion. That missed expectations of $3.01 billion, according to FactSet.

The total booking value across Expedia platforms &ndash which include Hotels.com, Vrbo and Expedia.com &ndash grew 4% to $31.45 billion. Analysts were looking for $31.76 billion, according to FactSet.

" We posted first quarter bookings and revenue within our guidance range despite weaker than expected demand in the US, drove bottom-line meaningfully above our guidance, and made significant progress against our strategic priorities," Expedia Group Chief Executive Ariane Gorin said in a news release. " Looking ahead, we are committed to continuing to deliver margin expansion while growing our top-line."

Expedia Stock Downgraded

On a call with analysts late Thursday, Expedia Chief Financial Officer Scott Schenkel said the weakness in the U.S. market weighed on total bookings for the quarter.

" Demand in the U.S. was softer than expected, which was a headwind given two-thirds of our business comes from the U.S. point of sale," Schenkel said. " We also noticed softness in demand for inbound travel into the U.S., which was down 7%. As part of that, inbound bookings from Canada fell nearly 30%."

Expedia lowered its 2025 full-year guidance for gross bookings and revenue growth outlook. The company expects growth for both metrics to fall between 2% and 4%, compared to a previous 4% and 6%.

Booking Holdings (

BKNG) and

Airbnb(

ABNB) called out similar trends in the U.S. during their recent Q1 earnings calls. But both those companies &ndash particularly Booking Holdings,

with its Europe focus &ndash have larger international operations to lean on.

Analysts with Piper Sandler downgraded Expedia to a negative under-weight call following the report.

" The commentary around U.S. inbound travel and the B2C (business-to-consumer) business was discouraging and suggests a tough slog from here," Piper Sandler analyst Thomas Champion wrote. " It could also get incrementally worse."

Expedia Down 9% In 2025

Expedia stock entered Friday trading down 9% this year compared with a 3.7% decline for the S& P 500.

But shares are ahead 52% from 12 months ago and Expedia stock had rallied nearly 10% this month to retake its

50-day moving average, not including Friday' s earlier slide.

Coming into the report, Expedia stock had an IBD Composite Rating of 94 out of a best-possible 99, according to

IBD Stock Checkup. The score combines five separate proprietary ratings into one rating. The best growth stocks have a Composite Rating of 90 or better