For those who believe in AEM' s growth story and are already on board, this high-energy, high-tempo music could lift your spirits even further.

ENG SUB 動 畫 【 仙 逆 】 王 林 問 鼎 插 曲 《 何 惜 一 戰 》 完 整 版 - 張 申 騁 「 燃 」 | Renegade Immortal OST (EP 121 ED)

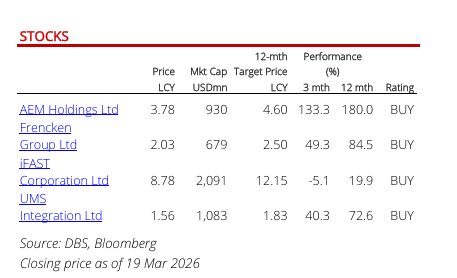

From pg 11 report, forecast EPS for AEM for FY26 and FY27 is 10.9 cents and 14.4 cents respectively, highest among peers UMS and Frencken

If shares price is $8, forward PE will be approximately 55times base on FY27 projected earnings. This implies market is pricing aggressive growth expectations.

If earnings growth slows or results underperform, such a high multiple leaves little margin of safety.

https://www.dbs.com/insightsdirect/api/s3/dbs-buffer/article_attachment/20260320/07-35-27_SG%20Tech%20-%2020mar2026.pdf

If shares price is $8, forward PE will be approximately 55times base on FY27 projected earnings. This implies market is pricing aggressive growth expectations.

If earnings growth slows or results underperform, such a high multiple leaves little margin of safety.

Trade‑ offs

Bull case - Investors may justify the premium if they believe AEM technology edge (eg in test equipment for advanced chips) will deliver outsized growth.

Bear case - Valuation looks stretched, especially if Q1 results trigger sell on news behavior after a parabolic run.

Takeaway

A forward P/E of 55x is objectively high for AEM compared to UMS, Frencken, and global peers. It reflects strong optimism but also raises the risk of sharp corrections if growth expectations are not met.

https://www.dbs.com/insightsdirect/api/s3/dbs-buffer/article_attachment/20260320/07-35-27_SG%20Tech%20-%2020mar2026.pdf

AEM Technical View

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

Such a move could unfold before Q1 results, setting up a potential double top formation. A double top is a classic reversal pattern, signaling that an uptrend may be exhausted and a downtrend could follow. Once results are released, the market may react with a &ldquo sell on news&rdquo response, especially if the stock has already run too far, too fast.

For those who missed the initial rally but believe in Arogosta&rsquo s story, patience is key. Wait for confirmation from a shooting star, evening star, or other bearish candlestick signals before considering entry.

Remember: no stock climbs forever. Overbought conditions eventually demand a pause. On the extreme side, the 161.8% Fibonacci extension projects a price close to $8.

This is purely a technical perspective treat it as coffeeshop talk, shared for entertainment rather than investment advice.

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

Such a move could unfold before Q1 results, setting up a potential double top formation. A double top is a classic reversal pattern, signaling that an uptrend may be exhausted and a downtrend could follow. Once results are released, the market may react with a &ldquo sell on news&rdquo response, especially if the stock has already run too far, too fast.

For those who missed the initial rally but believe in Arogosta&rsquo s story, patience is key. Wait for confirmation from a shooting star, evening star, or other bearish candlestick signals before considering entry.

Remember: no stock climbs forever. Overbought conditions eventually demand a pause. On the extreme side, the 161.8% Fibonacci extension projects a price close to $8.

This is purely a technical perspective treat it as coffeeshop talk, shared for entertainment rather than investment advice.

Just like DBS, it could just be another once in a life time stock

Saw this picture..... someone was trying to make a joke out of it.... except it may not be not a joke.......

yesterday price hit $3.84 intraday high...

so if you follow the logical money trail....

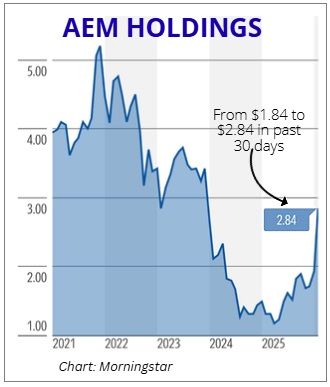

In 30 days, AEM' s price went from $1,84 to $2.84

In 20 days, AEM' s price went from $2.84 to $3.84

in 10 days?

whatever it' s in mind, don' t bet against it, now is $4 plus..... takes another 70c plus

=====

btw, I was trying to post my previous post BEFORE LUNCH' . ....and managed to go thru only a while ago, so the sting of the message was lost in the delay.....

yesterday price hit $3.84 intraday high...

so if you follow the logical money trail....

In 30 days, AEM' s price went from $1,84 to $2.84

In 20 days, AEM' s price went from $2.84 to $3.84

in 10 days?

whatever it' s in mind, don' t bet against it, now is $4 plus..... takes another 70c plus

=====

btw, I was trying to post my previous post BEFORE LUNCH' . ....and managed to go thru only a while ago, so the sting of the message was lost in the delay.....

Solubl ( Date: 27-Feb-2026 11:39) Posted:

|

Beautiful article

aragosta ( Date: 20-Mar-2026 15:06) Posted:

|

Whole day I was walking up and down 52 Serangoon North Avenue 4, hoping some one would recognise me and come up to me..... But alas there were none, it' s like some people just have a nice meal at a 5 star Michelin restaurant and leave with out paying, pretending nothing' s doing...... but it' s okay because I myself was pretending (very hard) too, trying to be humble and try not say a thing to sound like bragging....... but I tell you, it' s very very hard..... very very difficult to stay humble when the stuffs you anyhow talk, somehow turn up to be true!........btw, it hits four now in case you pretending not to notice

Any way, to those very shy believers, I got another coming great news for you, another tokkong development is likely on the way that will rocket this gem even further away from those unbelievers who brag they sold @$3, @$3.38......, this may come as early next month&hellip

today, the news seems to be on JPM, but I tell you, Temasek is working very hard not to be overshadowed......heard it is trying to get another big tech company, in which it has a big stake to join as a high value partner of AEM....this one in fact, the black market is 99% confident will happen soon&hellip ..

On another note, THIS FOLLOWING PIECE IS DEDICATED TO JURONGWEST, one of the few black market believers ...... basically addressing his confusion and concern....... For those who are too lazy to read my lengthy statement below, you may just read the following summary which provide the gist of it......

A LAZY SUMMARY

JPMorgan Chase & Co. became a substantial shareholder in AEM Holdings on March 19, 2026, increasing its stake to 5.19% (16,307,735 shares) following a market acquisition. A significant portion of this holding is managed under a Prime Brokerage Agreement, which allows clients to leverage and borrow shares for trading, yet requires institutional disclosure. JPMorgan' s increased investment indicates strong conviction in AEM' s AI-driven growth trajectory, with FY2026 revenue guidance of S$460M - S$510M and a forward P/E of ~29.4x, suggesting resilience against patent litigation with Advantest. Furthermore, AEM presents a value opportunity, trading at a 25~35% forward P/E discount to industry leaders Advantest and Teradyne.

=========

Here is a structured breakdown of the latest developments regarding JPMorgan' s investment in AEM Holdings as of today, March 20, 2026.

1. The Transaction & Current Stake

On March 19, 2026, JPMorgan Chase & Co. officially crossed the 5% Substantial Shareholder threshold.

~ The Buy: Purchased 555,000 shares in the open market.

~ The Price: An average of S$3.35 per share.

~ Pre-Transaction Stake: 15,629,935 shares (4.97%).

~ AFTER YESTERDAY' S TRANSACTION: Current Stake: 16,307,735 shares (5.19%).

~ Note on Accuracy: The figures from the March 19 SGX Filing are the definitive legal record. Previous higher estimates likely included non-notifiable or " right-to-recall" shares that hadn' t yet triggered a formal disclosure.

2. Understanding the " Prime Brokerage Agreement"

A large portion of JPMorgan' s stake is held under a Prime Brokerage Agreement, simply means &hellip &hellip

~ The Banker' s Role: JPMorgan acts as a " one-stop-shop" for hedge funds and large investors.

~ Deemed Interest: Even if JPMorgan' s clients are the ones buying, Singapore law requires JPMorgan to disclose these shares as a deemed interest because they control the custody and lending of the stock.

~ The Signal: When a Prime Broker' s holding increases, it usually means their most sophisticated, high-networth clients are aggressively " long" on the stock.

~ Newbies' often MISCONCEPTION: So when you see an SGX' s filing by a big institutional fund (like BlackRock, JPM, Goldman Sachs) it DOES NOT necessarily means that that fund is buying for its own &ldquo trading accounts&rdquo . It could well mean it is executing the order on behalf of a high networth client. Got it?

3. The Confidence Factors in the Increase in Stake

JPMorgan' s move to buy at S$3.35 ~ a price significantly higher than the S$2.00 range seen earlier this year ~ signals high conviction in two areas:

~ Growth Inflection: AEM has issued FY2026 revenue guidance of S$460M &ndash S$510M. This is driven by a massive ramp-up from a new AI/High-Performance Computing (HPC) customer that is expected to become their largest revenue source. Multiple sources are persistently stating as of late, many top tech companies have been in need of AEM' s critical high value services.

~ Legal Resilience: By increasing their stake, institutional investors are signaling that the Advantest patent litigation is likely manageable. They likely view AEM' s new thermal testing technology as unique enough to either win in court or reach a settlement that won' t cripple the company' s finances.

4. Why AEM is STILL Undervalued vs. Peers

Despite AEM' s recent price surge, it remains " cheap" when compared to the global semiconductor testing duopoly:

|

Metric |

AEM Holdings |

Advantest (Japan) |

Teradyne (USA) |

|

Forward P/E (FY26) |

~29.4x |

~40.5x |

~45.9x |

|

Discount to Peers |

Baseline |

27% Premium |

35% Premium |

~ The Opportunity: AEM is trading at a 30% average discount to its peers on a forward-earnings basis.

~ Small-Cap Alpha: Because AEM is much smaller (market cap ~S$1.18B), its earnings explosion from new AI contracts has a much bigger impact on its stock price than similar wins would for a US$100B giant like Advantest.

5. The Final Word

JPMorgan' s entry as a substantial shareholder marks a turning point for AEM. By paying S$3.35 per share, the bank is validating AEM' s transition from a legacy Intel-dependent supplier to a diversified AI infrastructure play. While the Advantest lawsuit remains a risk, the Forward P/E discount of nearly 30% compared to global peers suggests that the market has more than priced in the legal uncertainty, leaving significant room for catch-up growth as FY2026 revenue targets are met.

aragosta ( Date: 12-Mar-2026 16:40) Posted:

|

You&rsquo re right to challenge whether EPS of 16&ndash 18 cents in FY2026 is realistic compared to FY2025&rsquo s ~5 cents. On the surface, that looks like a huge jump&mdash more than triple. Let&rsquo s break down why analysts think it&rsquo s possible, and where the risks lie.

📊 FY2025 vs FY2026 EPS

- FY2025 EPS: ~SGD 0.045&ndash 0.05 (net profit ~SGD 20m).

- FY2026 Projection: ~SGD 0.16&ndash 0.18 (net profit ~SGD 70&ndash 80m).

That&rsquo s a 3&ndash 4x increase in earnings year-on-year.

⚖ ️ Why Analysts See It as Plausible

-

Revenue Ramp-Up:- FY2025 revenue: SGD 399m.

- FY2026 guidance: SGD 460&ndash 510m (up ~15&ndash 28%).

-

Margin Expansion:- FY2025 net margin: ~5%.

- FY2026 expected margin: ~15&ndash 16% (due to higher volumes, better product mix, and new customer ramp).

-

Customer Diversification:- AEM&rsquo s second major AI/HPC customer contributed > 25% of FY2025 revenue.

- This new client is expected to scale significantly in FY2026, reducing reliance on Intel.

📌 Risks to Watch

- Execution Risk: If the new customer&rsquo s ramp is slower, EPS could undershoot (closer to 12&ndash 14 cents).

- Margin Pressure: Semiconductor cycles are volatile&mdash if margins don&rsquo t expand as expected, EPS growth will be muted.

- Valuation Sensitivity: At SGD 4.02, forward P/E looks reasonable (~22&ndash 25x), but only if EPS really hits 16&ndash 18 cents.

🔍 Calibration Table

| Scenario | Revenue (SGD m) | Net Margin | Net Profit (SGD m) | EPS (SGD) | Forward P/E (at 4.02) |

|---|---|---|---|---|---|

| Bear | 460 | 10% | 46 | 0.105 | 38.3 |

| Base | 485 | 15% | 72.8 | 0.165 | 24.4 |

| Bull | 510 | 16% | 81.6 | 0.185 | 21.7 |

🎯 Takeaway

- Yes, 16&ndash 18 cents is aggressive but plausible if margins triple from FY2025 levels.

- The leap looks dramatic only because FY2025 EPS was unusually low due to margin compression.

- The market is already pricing in this rebound&mdash if AEM misses, valuation could look stretched again.

From $1 to $2 (less than 6 months), $2 to $4 (less than 2 months), this GEM is simply amazing (A.E.M. is a G.E.M)

It will just be a matter of time to go from $4 to $8 (Arogosta tip will be proven correct)

It will probably give a shoutout to Ifast - I' m FASTER than u.

It will just be a matter of time to go from $4 to $8 (Arogosta tip will be proven correct)

It will probably give a shoutout to Ifast - I' m FASTER than u.

Huat Ah,

There will be More Ang Moh funds coming in to buy up AEM.

There will be More Ang Moh funds coming in to buy up AEM.

JP Morgan has become substantial shareholder of AEM !

https://links.sgx.com/1.0.0/corporate-announcements/HZJ0F1UBKUNIIT3D/878828__eFORM3V2.pdf

Pehaps the analyst are waiting for the release of Q! results to get more clarity before adjusting the target prices.

I wonder when the analysts are (going to copycat the black market analysis) and start crawling out one by one with new targets.... remember, current PE is irrelevant... work out the GROWTH EARNINGS & the new FORWARD PE, and confirms AMD, Micron, Broadcom as the new pillar and supporting partners, and Nvidia and Meta as indirect partners, and post on their recently phenomenal earnings.

============

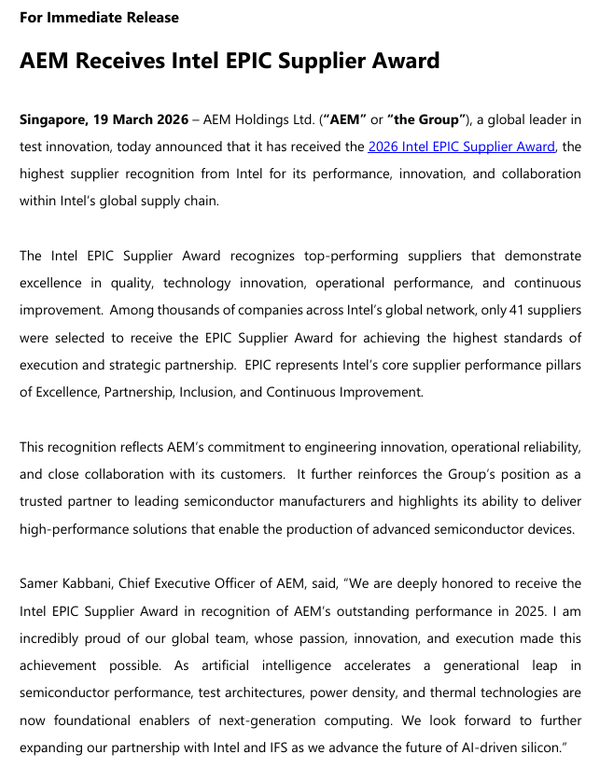

AEM Holdings has transitioned from being a single-customer equipment supplier to a diversified AI infrastructure play. Its recent stock resilience is a direct result of being strategically positioned at the intersection of several massive global semiconductor partnerships and the ongoing AI boom.

1. The New Pillar & AMD-Meta Synergy

The most significant catalyst for AEM' s recent strength is its expansion into the AI/HPC (High-Performance Computing) segment with a pillar " major fabless customer," widely identified by analysts as AMD.

- The Meta Connection: AMD' s landmark deal with Meta to deploy up to 6 gigawatts of AI computing power acts as a multi-year volume driver for AEM.

- Test Intensity: These advanced AI GPUs require significantly more rigorous testing than traditional chips. AEM' s System Level Test (SLT) solutions are essential for the high-power thermal requirements of these next-gen processors.

- Revenue Impact: This new pillar is expected to become AEM' s top revenue contributor by the end of 2026, fueling the company' s strong FY2026 revenue guidance of S$460M&ndash S$510M.

2. The Current Anchor & Intel-Nvidia Alliance

While AEM is diversifying, its original anchor customer, Intel, continues to play a vital role.

- The Nvidia Boost: The US$5 billion investment by Nvidia into Intel has revitalised Intel' s roadmap. The two giants are now co-designing chips for AI PCs and data centres.

- Direct Rub-on: As a long-time partner for Intel' s backend testing, AEM directly benefits from any increase in Intel' s manufacturing volumes. Every Intel CPU integrated into an Nvidia-powered AI server represents a high-value testing opportunity for AEM.

3. The New Supporting Partners & Micron-Broadcom Influence

The AI boom requires not just processors (CPUs/GPUs), but also massive amounts of memory and networking hardware.

- The Micron Effect: Micron is currently building a US$9.5 billion High Bandwidth Memory (HBM) plant in Singapore. AEM is pivoting its SLT technology to support memory testing, with production ramp-up expected to align with Micron&rsquo s 2026 operational start.

- Broadcom Synergy: As Broadcom scales its custom AI chip business (for clients like Google and Meta), the industry-wide move toward heterogeneous integration (combining different chips into one package) increases the demand for AEM' s sophisticated " Test 2.0" solutions.

4. Strategic Support & Other Catalytic Partnerships

- Foundry Expansion: AEM' s partnership with Intel Foundry allows it to potentially serve other tech giants (like Microsoft or AWS) who are now using Intel&rsquo s factories to build their own custom AI silicon.

- Strategic Shareholder Support: With Temasek Holdings as its largest shareholder (12%), AEM maintains the financial backing and institutional credibility needed to win these large-scale global contracts.

The AI Boom Effect

The AI boom is spurring AEM by shifting the focus from " cheap testing" to " mission-critical testing." Because AI chips are extremely expensive and power-hungry, customers cannot afford failures. This makes AEM' s high-precision thermal and system-level test solutions indispensable, allowing the company to command better margins and secure longer-term revenue visibility.

aragosta ( Date: 27-Feb-2026 12:41) Posted:

|

If this tekong rally still got legs and continue to sprint like usain bolt, we could potentially see $4.00

This bull is on a tear - flying like Usain Bolt!

Looking at the buying momentum by funds and houses, AEM price looks set to recover to its past glory in the mid term.

Just my thoughts and opinion.

Just my thoughts and opinion.

Yes, Prudent not to be greedy if you are playing short-term.

Long term can still hold if you bought below $2.

Long term can still hold if you bought below $2.

Sgvale ( Date: 16-Mar-2026 15:45) Posted:

|

Sold off 3.38. Wait for another opportunity

Sgvale ( Date: 16-Mar-2026 15:15) Posted:

|

This stock is simply amazing. FY25 EPS is 4.35 cents. It trading at very high PE of 78 times based on $3.40

Market is pricing very strong earnings in FY26 into current share price.

Even at EPS of 8.7 cents, prospective PE will be 39x, Justified? (can trade at high PE due to strong earnings growth!)

Market is pricing very strong earnings in FY26 into current share price.

Even at EPS of 8.7 cents, prospective PE will be 39x, Justified? (can trade at high PE due to strong earnings growth!)