Post Reply

41-60 of 7131

Post Reply

41-60 of 7131

SGX Shortsell Volume on 19/5/2026 (Tue)

ComfortDelGro - 13,446,500 shares @ SGD 17,212,797Winnertakeall ( Date: 19-May-2026 07:55) Posted:

SGX Shortsell Volume on 18/5/2026 (Mon)

ComfortDelGro - 13,406,600 shares @ SGD 17,020,419 |

|

will CDG be like singpost? kept dropping from $2 to $1 and now only 35 cents?Spike18 ( Date: 19-May-2026 16:58) Posted:

| Night is at its darkest before dawn ! As we do not really know what time we are at, will commence accumulation ... as dawn will surely come so will CDG given its pedigree |

|

Night is at its darkest before dawn ! As we do not really know what time we are at, will commence accumulation ... as dawn will surely come so will CDG given its pedigree

DBS has adjusted target price downward to $1.11 in view of the weak results.

Winnertakeall ( Date: 19-May-2026 15:35) Posted:

x 0 x 0

x 0 x 0 |

After ComfortDelGro reported weaker-than-expected Q1 FY2026 earnings, several analysts cut their target prices, though most still see upside from current levels.

Current share price is around S$1.27& ndash 1.28. Consensus target prices are now mostly in the S$1.50& ndash 1.60 range.

Key updated analyst targets after Q1 results:

|

Research House

|

Rating

|

Target Price

|

| UOB Kay Hian |

Hold |

S$1.54 |

| Maybank |

Hold |

S$1.50 |

| Phillip Securities |

Neutral |

S$1.35 |

| DBS |

Hold |

S$1.60 |

| Consensus Average |

Mixed |

S$1.56 |

Main reasons analysts reduced targets:

- Taxi and private-hire profits dropped sharply

- Higher fuel costs

- Smaller Singapore taxi fleet

- Weak UK airport transfer demand

- Competitive pressure in Australia taxi operations

But analysts still see support from:

- Strong public transport business

- Stable cash flow and dividends

- Overseas bus contract improvements

- Long-term mobility and EV/autonomous transport plans

The market currently appears cautious near-term, but many analysts still expect recovery in later quarters if fuel costs ease and taxi utilisation improves. At current prices, implied upside to consensus target is roughly 20%+.

|

|

|

After ComfortDelGro reported weaker-than-expected Q1 FY2026 earnings, several analysts cut their target prices, though most still see upside from current levels.

Current share price is around S$1.27 ~ 1.28. Consensus target prices are now mostly in the S$1.50 ~ 1.60 range.

Key updated analyst targets after Q1 results:

|

Research House

|

Rating

|

Target Price

|

| UOB Kay Hian |

Hold |

S$1.54 |

| Maybank |

Hold |

S$1.50 |

| Phillip Securities |

Neutral |

S$1.35 |

| DBS |

Hold |

S$1.60 |

| Consensus Average |

Mixed |

S$1.56 |

Main reasons analysts reduced targets:

- Taxi and private-hire profits dropped sharply

- Higher fuel costs

- Smaller Singapore taxi fleet

- Weak UK airport transfer demand

- Competitive pressure in Australia taxi operations

But analysts still see support from:

- Strong public transport business

- Stable cash flow and dividends

- Overseas bus contract improvements

- Long-term mobility and EV/autonomous transport plans

The market currently appears cautious near-term, but many analysts still expect recovery in later quarters if fuel costs ease and taxi utilisation improves. At current prices, implied upside to consensus target is roughly 20%+.

UOBKH downgrades ComfortDelGro to &lsquo hold&rsquo as Q1 earnings disappoint

Brokerage slashes target price for the land transport operator by 15% to S$1.54

[SINGAPORE] ComfortDelGro (CDG) : C52 -1.56% has been downgraded to &ldquo hold&rdquo from &ldquo buy&rdquo by UOB Kay Hian, following a first-quarter financial performance that fell significantly short of market expectations.

In a report on Thursday (May 14), the brokerage also slashed its target price for the land transport operator by 15 per cent to S$1.54, down from S$1.82 previously.

The transport player&rsquo s net profit fell 16.1 per cent to S$40.5 million in the first quarter ended Mar 31, amid challenges in the taxi and private-hire vehicle business.

For the first quarter ended Mar 31, CDG&rsquo s core operating profit fell 18 per cent year on year to S$66.2 million, while core profit after tax and minority interests (Patmi) slid 16 per cent to S$40.3 million.

The lacklustre performance came despite a 5 per cent increase in revenue to S$1.2 billion. Both core operating profit and Patmi missed expectations, UOBKH said, achieving just 17 per cent of the research house&rsquo s and consensus full-year forecasts.

&ldquo We lower our 2026-28 earnings forecasts by 19 per cent, primarily on a material downgrade to point-to-point operational profit due to higher fuel costs, Singapore taxi fleet contraction, persistent UK airport transfer headwinds and Australian competitive pressures,&rdquo said analysts Heidi Mo and Kai Jie Tang.

Headwinds from taxi segment

The sharp earnings miss was primarily driven by a severe contraction in CDG&rsquo s taxi and point-to-point (P2P) transport segment, where operating profit collapsed by 45 per cent year on year and 31 per cent sequentially to S$17.5 million.

Consequently, core operating margins contracted 5.1 percentage points to 7.3 per cent.

&ldquo The decline was across all geographies,&rdquo the analysts said.

Domestically, CDG&rsquo s Singapore taxi fleet continued its downward trajectory, shrinking to 7,556 units by March 2026 from 8,424 at the end of 2024. The local market share slipped to 61.7 per cent as rival GrabCab aggressively expanded its taxi fleet from 20 to 420 vehicles over a nine-month period.

In international markets, the group&rsquo s Australian A2B business faced &ldquo intensifying ride-hailing competition and cautious consumer spending&rdquo .

Concurrently, long-haul inbound travel to the United Kingdom remained suppressed due to the ongoing Middle East conflict, which directly reduced airport transfer volumes for its premium private hire arm, Addison Lee.

Considering these headwinds, UOB Kay Hian lowered its 2026 P2P operating profit forecast for the company by about 40 per cent to S$93 million.

Public transport cushions

Providing some insulation to the group was the public transport segment, which posted a revenue increase of 7 per cent year-on-year to S$814.5 million.

This was supported by higher daily ridership on the North East Line and Downtown Line, up 2.7 per cent and 2.1 per cent, respectively, which flowed through alongside a rail fare adjustment implemented in December 2025. Operating profit for public transport rose a modest 3 per cent to S$37.7 million.

Meanwhile, CDG&rsquo s inspection and testing segment delivered a strong beat on operating profit, which rose 34 per cent year on year to S$12.1 million.

This performance was lifted by peak installation volumes of ERP 2.0 on-board units, though analysts caution that contributions are &ldquo expected to taper progressively&rdquo over the rest of the year.

Outlook

The research house noted that &ldquo P2P headwinds and the absence of a near-term recovery catalyst remain&rdquo .

Near-term swing factors that investors should monitor include the upcoming tender results for the Serangoon-Eunos bus package expected in the third quarter of 2026.

Conversely, the loss of the Tampines bus package to Go-Ahead, effective July 2026, will present a modest headwind, analysts said.

Despite the downgrade to operational growth, the group said that CDG&rsquo s dividend yield &ldquo remains decent at 5.1 per cent&rdquo .

As at the trading break on Monday, shares of ComfortDelGro were flat at S$1.28.

SGX Shortsell Volume on 18/5/2026 (Mon)

ComfortDelGro - 13,406,600 shares @ SGD 17,020,419

I should have said $126.50 since minimal no. of shares to buy is 100.

JurongW ( Date: 18-May-2026 23:41) Posted:

If key management is not willing to put even $1 of their own money into buying shares, it signals the price still is not low enough.

JurongW ( Date: 18-May-2026 23:37) Posted:

Another quarter of negative results will pressure the share price towards that target.

2026 is shaping up to be a forgettable year. |

|

|

|

If key management is not willing to put even $1 of their own money into buying shares, it signals the price still is not low enough.JurongW ( Date: 18-May-2026 23:37) Posted:

Another quarter of negative results will pressure the share price towards that target.

2026 is shaping up to be a forgettable year.

tangsookiam1947 ( Date: 18-May-2026 23:29) Posted:

| SBB quite useless? everyday dropping.... maybe drop until $1? |

|

|

|

Another quarter of negative results will pressure the share price towards that target.

2026 is shaping up to be a forgettable year.tangsookiam1947 ( Date: 18-May-2026 23:29) Posted:

SBB quite useless? everyday dropping.... maybe drop until $1?

JurongW ( Date: 18-May-2026 18:25) Posted:

SBB today - 292,000 shares bought at 1.265 ($369,863) |

|

|

|

SBB quite useless? everyday dropping.... maybe drop until $1?JurongW ( Date: 18-May-2026 18:25) Posted:

SBB today - 292,000 shares bought at 1.265 ($369,863)

JurongW ( Date: 15-May-2026 19:34) Posted:

SBB today - 730,000 shares bought at 1.30 ($950,241) |

|

|

|

SBB today - 292,000 shares bought at 1.265 ($369,863)JurongW ( Date: 15-May-2026 19:34) Posted:

SBB today - 730,000 shares bought at 1.30 ($950,241) |

|

Sooo many fearmongers, LOL

MengKK ( Date: 18-May-2026 11:52) Posted:

Good idea,Sell yours property/condo/HDB all dump in !

stonkmaster ( Date: 18-May-2026 04:02) Posted:

| 0.50 too high. Confirm will drop to 0.10 and I will go borrow from ah long to all in |

|

|

|

Good idea,Sell yours property/condo/HDB all dump in !

stonkmaster ( Date: 18-May-2026 04:02) Posted:

0.50 too high. Confirm will drop to 0.10 and I will go borrow from ah long to all in.

tangsookiam1947 ( Date: 17-May-2026 14:44) Posted:

| im waiting at $0.50... why $0.80 is good? |

|

|

|

Q2/2H results very critical to ComfortDelGro

Let' s wait for the next reporting in Aug2026Winnertakeall ( Date: 16-May-2026 13:47) Posted:

After the weaker 1Q2026 results, ComfortDelGro is not standing still.

Management is pushing several strategies to stabilise earnings and improve long-term growth.

Main plans going forward:

- Transforming taxi business into a &ldquo hybrid fleet + platform&rdquo model

- CDG admitted traditional taxi operations are under pressure from ride-hailing competition.

- It plans to strengthen its own booking/platform ecosystem instead of relying mainly on taxi rentals.

- Focus is shifting toward:

-

- premium corporate customers,

-

- specialised transport services.

- Investing in autonomous vehicle (AV) and AI capabilities

- Management said it wants to build AV ecosystems globally and integrate autonomous vehicles into real transport networks.

- AI and technology investments are part of improving operational efficiency and future competitiveness.

- Expanding stronger public transport operations

- Public transport remains CDG&rsquo s most stable earnings pillar.

- The company is focusing on:

-

- renewing UK bus contracts at better margins,

-

- improving rail ridership in Singapore,

-

- bidding for new transport contracts.

Possible future catalysts include:

- Serangoon-Eunos bus package tender result,

- Jurong Region Line operations from 2028,

- more overseas transport contracts.

- Cost control and fuel management

- Fuel costs hurt margins in Q1.

- Management said part of fuel exposure is hedged and some public transport contracts have indexation mechanisms to offset higher energy costs.

- Growing overseas businesses

- Overseas operations already contribute over 50% of revenue.

- CDG continues focusing on:

-

- European transport operations,

-

- non-emergency patient transport,

-

- corporate mobility services.

- Long-term driving centre investment

- Around S$200 million is being allocated for a next-generation driving centre in Singapore.

- Goal is to improve training capacity and increase market share over time.

What investors are watching now:

- Whether taxi earnings stabilise,

- Recovery in UK airport transfer demand,

- Whether competition from Grab and PHV players eases,

- Potential share buyback if share price stays weak (not officially announced yet).

Overall:

- Near-term earnings may remain soft for a few quarters.

- But CDG is trying to shift from a mature taxi operator into a broader mobility and transport platform company.

- Dividend support still looks relatively solid because public transport cash flows remain stable.

|

|

0.50 too high. Confirm will drop to 0.10 and I will go borrow from ah long to all in.

tangsookiam1947 ( Date: 17-May-2026 14:44) Posted:

im waiting at $0.50... why $0.80 is good?

JurongW ( Date: 16-May-2026 14:41) Posted:

The part on " Near-term earnings may remain soft for a few quarters" means share price will continue to move lower until the price remains attractive enough for BBs to buy on the cheap.

It prior peak was about $1.60, if it can drop by half say to $0.80 if Q2 to Q4 results continue to disappoint the market, it presents a good buying opportunity.

Imagine paying 8 cents dividend at this price, translates to a yield of 10%

NAV is about $1.20+ |

|

|

|

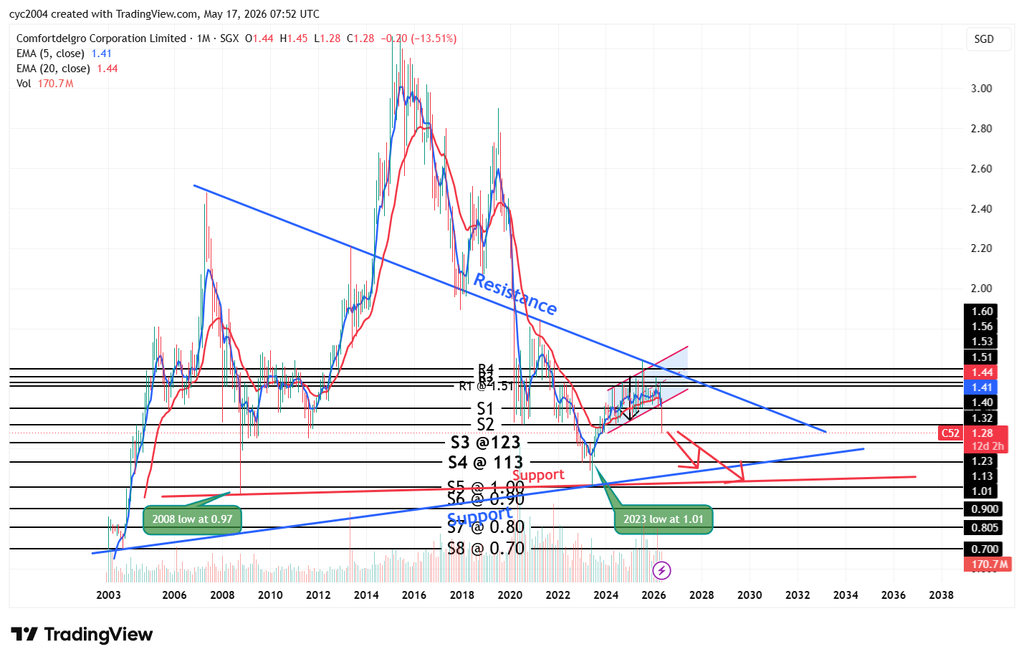

KIV

Highest share price in Jun 2015 - $3.26

Drop by Half : $1.63

Half of $1.63 $0.815

Half of $0.815: $0.405tangsookiam1947 ( Date: 17-May-2026 23:27) Posted:

i think it may crash below $1 very soon....dydd

JurongW ( Date: 17-May-2026 15:54) Posted:

KIV

|

|

|

|

i think it may crash below $1 very soon....dyddJurongW ( Date: 17-May-2026 15:54) Posted:

KIV

|

|

KIV

📊 Lower P/E Assignment Scenarios

Let us stress test with

9× and 10× P/E, which would reflect investor caution:

| Scenario |

EPS (cents) |

P/E Multiple |

Implied Value (SGD) |

| &ndash 10% profit |

~9.5 |

10× |

0.95 |

| &ndash 10% profit |

~9.5 |

9× |

0.86 |

| &ndash 20% profit |

~8.5 |

10× |

0.85 |

| &ndash 20% profit |

~8.5 |

9× |

0.77 |

⚖ ️ Implications

- At 9&ndash 10× P/E: CDG&rsquo s fair value compresses into the 0.77&ndash 0.95 range, well below current 1.28 and below NAV (1.20).

- Dividend yield trade‑ off: At ~0.85, yield could spike to ~9&ndash 10%, which might attract yield hunters even if earnings are weak.

- Market psychology: Assigning 9&ndash 10× P/E signals investors see CDG as a &ldquo no‑ growth, yield‑ only&rdquo play, rather than a transport growth stock.

- NAV disconnect: Trading below NAV would mean the market is discounting asset backing due to structural headwinds (taxi competition, contract risk).

👉 So yes, assigning a lower P/E is realistic if sentiment turns defensive, CDG could be valued more like a bond proxy, with yield as the only anchor. That would put fair value closer to

SGD 0.80 to 0.95 under a 20% earnings drop.