Hong Fok

Last:0.93

-

Technical Analysis-Seasonal Trend

Post Reply

41-60 of 1573

Post Reply

41-60 of 1573

Ah Cheong Lai Lor....

TikTalk ( Date: 01-Apr-2026 12:34) Posted:

|

$0.91 le

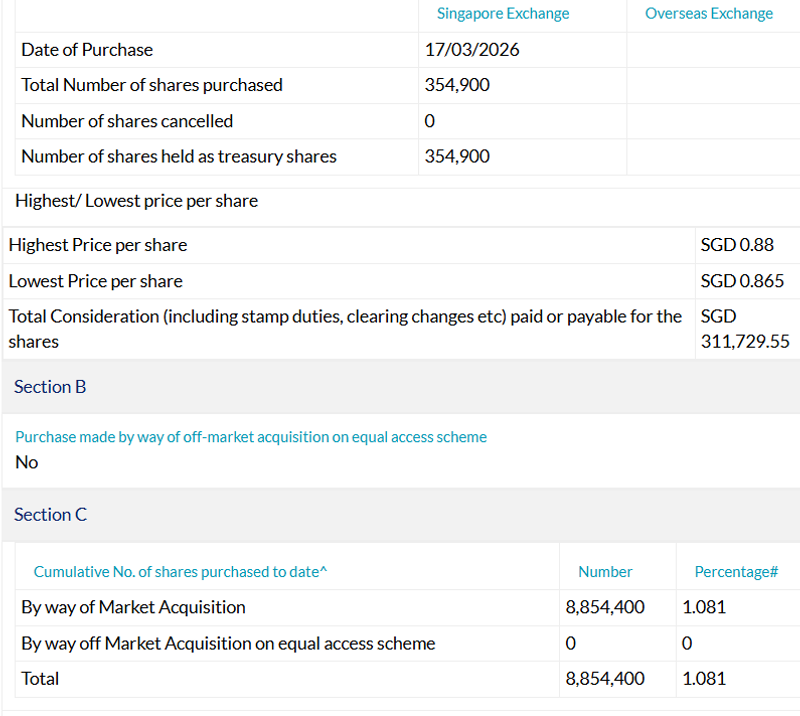

Resume SBB today - 50,600 shares bought at $0.865muifan ( Date: 23-Mar-2026 18:23) Posted:

|

Corporate action in April or May 2026??

Share buyback stopped

Agreed... More n more retail aware HF will sailing fast... @1.20

muifan ( Date: 20-Mar-2026 20:47) Posted:

| Today volume all done by retail ... |

|

Today volume all done by retail ...

Looking good ! May fly anytime!

7ocean ( Date: 20-Mar-2026 11:13) Posted:

Next week she' ll cross over $1

mrwise ( Date: 20-Mar-2026 10:20) Posted:

|

|

|

Next week she' ll cross over $1

mrwise ( Date: 20-Mar-2026 10:20) Posted:

|

Cannot let go below $2!!

Lai Lai Lai Don' t let Cheong Family collect cheap share

TikTalk ( Date: 20-Mar-2026 09:33) Posted:

|

cheong cheong cheong

When buying gets aggressive?it is a good buy call..

Things looking good

Do your own due diligence

Risk looks low with good returns

7ocean ( Date: 20-Mar-2026 09:20) Posted:

90% confirm privatization, They keep buying up

fruitfulness ( Date: 18-Mar-2026 18:04) Posted:

| For complete privatization, the offer price should be at least 0.5 NAV (shareinvestor.com states $2.83 as NAV, but others estimate the RNAV to be about $3.65 per share). In order not to be a miserably lowball offer, the first offer should come in between $1.40 and $1.80. But I am thinking it' s more likely to have asset monetization e.g. selling of International Building, than a complete privatization. |

|

|

|

90% confirm privatization, They keep buying up

fruitfulness ( Date: 18-Mar-2026 18:04) Posted:

| For complete privatization, the offer price should be at least 0.5 NAV (shareinvestor.com states $2.83 as NAV, but others estimate the RNAV to be about $3.65 per share). In order not to be a miserably lowball offer, the first offer should come in between $1.40 and $1.80. But I am thinking it' s more likely to have asset monetization e.g. selling of International Building, than a complete privatization. |

|

For complete privatization, the offer price should be at least 0.5 NAV (shareinvestor.com states $2.83 as NAV, but others estimate the RNAV to be about $3.65 per share). In order not to be a miserably lowball offer, the first offer should come in between $1.40 and $1.80. But I am thinking it' s more likely to have asset monetization e.g. selling of International Building, than a complete privatization.

Ya, Hong Fok should keep up their SBB to beyond the share price of $1.00. Then it is a clear indication by them that Hong Fok is severely undervalued.

JurongW ( Date: 18-Mar-2026 13:46) Posted:

That is a tough call. They may be buying back shares at a low price and if they eventually decide to delist, they would likely need to offer a considerable premium over the current price given the company high NAV.

Just my view.

7ocean ( Date: 18-Mar-2026 10:41) Posted:

| Is it possible for Hong Fok to be privatized or to split its shares |

|

|

|

That is a tough call. They may be buying back shares at a low price and if they eventually decide to delist, they would likely need to offer a considerable premium over the current price given the company high NAV.

Just my view.

7ocean ( Date: 18-Mar-2026 10:41) Posted:

Is it possible for Hong Fok to be privatized or to split its shares?

JurongW ( Date: 17-Mar-2026 17:46) Posted:

SBB today

|

|

|

|

Is it possible for Hong Fok to be privatized or to split its shares?

JurongW ( Date: 17-Mar-2026 17:46) Posted:

SBB today

|

|

SBB today

No idea, but the company has been buying back its shares regularly in the open market, perhaps due to undervaluation.

Its NAV is $3.65, so its now trading at less than 25% of its NAV.

7ocean ( Date: 17-Mar-2026 09:48) Posted:

Will this be a full acquisition ?

JurongW ( Date: 16-Mar-2026 18:13) Posted:

Here&rsquo s a concise summary of the article you&rsquo re viewing:

Main Points

- Corporate Monitor&rsquo s Report: Highlights concerns about Hong Fok Corporation&rsquo s executive pay being disproportionate to its performance.

- Family Control: The Chong family owns ~70% of the company and dominates management, with six family members among the top 10 highest-paid staff.

- High Executive Compensation: In 2024, the two co-presidents earned over S$9.9 million combined, nearly 10% of company revenue &mdash far higher than peers. Including other family members, total pay reached ~16% of annual revenue.

- Profit vs. Revenue: FY2025 net profit rose 116% to S$30.6 million, but revenue fell 6%. Gains were largely from property revaluation (International Building, Yotel Hotel), not cash inflows.

- Weak Operational Performance: Stripping out revaluation gains, operating revenue and margins have declined. Gross yield (2%) and net operating yield (1%) are well below industry averages (4.5% and 3.3%).

- Share Price Lag: While peers&rsquo stocks surged 30&ndash 100% in the past year, Hong Fok&rsquo s rose only ~5%.

- Governance Concerns: Heavy reliance on revaluation gains, lack of clawback provisions, and high bonuses raise fairness issues for shareholders.

- Historical Disputes: Executive pay has been contentious since at least 2012, leading to shareholder walkouts and SGX inquiries. The company later set up a remuneration committee and hired consultants.

Overall takeaway: The report questions whether Hong Fok&rsquo s high executive pay is justified, given weak operational efficiency, reliance on passive asset revaluation, and shareholder value concerns.

|

|

|

|