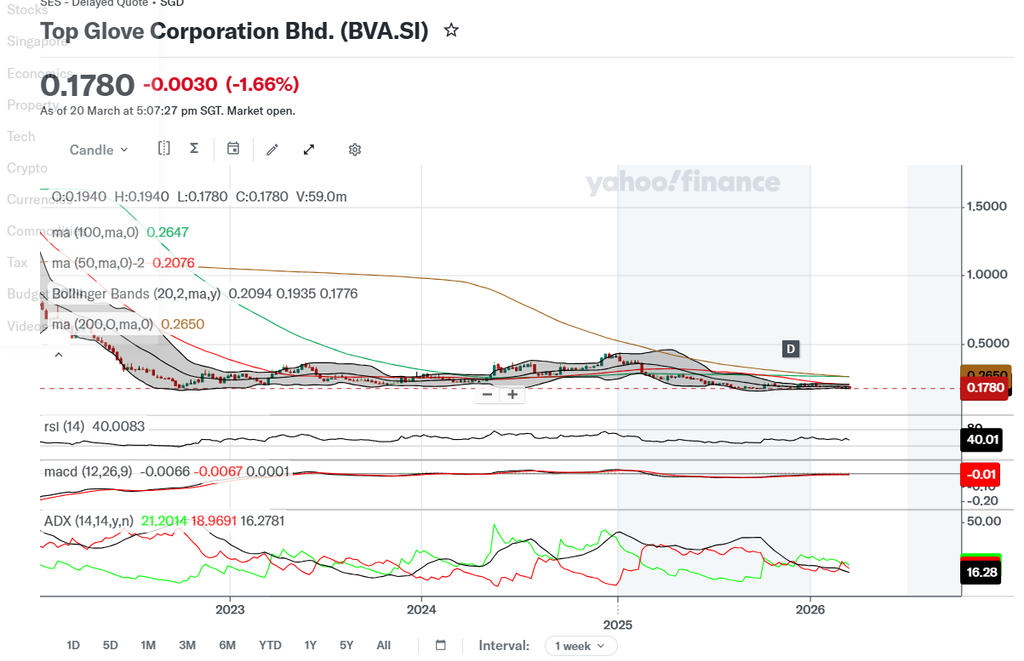

Double divergence in CCI/ Likely to cheong

Here&rsquo s a structured breakdown of the Top Glove (BVA.SI) chart you shared:

📊 Price & Trend Context

- Current Price: 0.178 SGD (down 1.66%).

- Moving Averages:

- MA(50) = 0.208

- MA(100) = 0.265

- MA(200) = 0.265

- Price is well below all major moving averages, confirming a long-term downtrend.

📈 Momentum & Strength

- RSI (14) = 40

- Weak momentum, leaning toward oversold but not extreme.

- MACD (12,26,9):

- MACD Line = -0.0066, Signal = -0.0067, Histogram = +0.0001

- Flat and negative, showing lack of bullish momentum.

- ADX (14) = 21.2

- Weak trend strength overall.

- +DI (18.97) > -DI (16.28) &rarr slight bullish bias, but not convincing.

📉 Volatility & Risk

- Bollinger Bands (20,2):

- Upper = 0.209, Middle = 0.194, Lower = 0.178

- Price closed right at the lower band (0.178) &rarr suggests oversold conditions, possible short-term bounce.

- Multi-year context: Chart shows a persistent decline since 2022, with only brief consolidations.

🧭 Key Takeaways

- Bearish long-term: Price below all major moving averages, weak momentum, declining trend.

- Short-term oversold: Closing at the lower Bollinger Band could trigger a technical rebound.

- Weak conviction: ADX shows trend strength is not powerful any bounce may be limited unless volume picks up.

🎯 Levels to Watch

- Support: 0.177 (lower Bollinger band), 0.170 (psychological).

- Resistance: 0.194 (middle Bollinger), 0.208 (50-day MA).

- Breakout trigger: Sustained close above 0.21 would be first sign of trend reversal.

👉 In short: Top Glove remains in a long-term downtrend, but the stock is oversold near the lower Bollinger Band, which could spark a short-term rebound. Without strong volume or a break above 0.21, the broader trend remains bearish.

Looking at the chart you shared for Top Glove (BVA.SI), the price at 0.178 SGD is indeed hovering around a multi‑ year low.

📊 Evidence from the Chart

- The stock has been in a persistent downtrend since 2022, sliding from much higher levels.

- Current price (0.178) is below the 50‑ day, 100‑ day, and 200‑ day moving averages, which are all clustered around 0.21&ndash 0.26.

- The Bollinger lower band is at 0.1776, and the price closed right at that level &mdash showing it&rsquo s pressing against the lowest volatility boundary.

- Over the multi‑ year span shown, this is the lowest point reached, with no prior candles closing lower.

🧭 Interpretation

- Yes, it&rsquo s at a multi‑ year low &mdash the chart confirms this.

- Bearish bias remains intact: long‑ term trend is still downward.

- Short‑ term oversold: RSI at 40 and price hugging the lower Bollinger band suggest a possible technical rebound, but without strong volume or a break above 0.21, the broader trend won&rsquo t reverse.

👉 In short: Top Glove is trading at its lowest levels in years, which makes it technically oversold but still structurally weak. Any bounce from here would likely be corrective unless fundamentals or volume shift decisively.

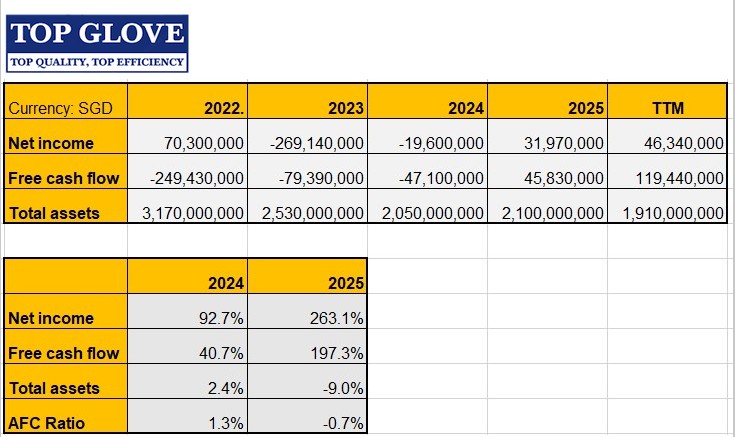

Top Glove' s FY2025 shows that it has turned around, returning to profitability with a net profit of RM109 million, compared to a net loss of RM64.9 million in FY2024. The full-year revenue surged 39% to RM3.49 billion and sale volume grew 55%. The US tariffs on Chinese competitors favored them.

The first half of the 2026 financial year (1HFY2026) performance is good as wwell. Net Profit (PATAMI) surged by approximately 92% to RM69.34 million, up from RM35.76 million in the previous year.

The AFC ratio or the Accrual Free cash ratio is impressive. The figure is definitely better than FY24, improved from 1.3% to -0.7% compare to previous years. This indicates that TG has had a good quality earning in FY25 compared to last years.

The first half of the 2026 financial year (1HFY2026) performance is good as wwell. Net Profit (PATAMI) surged by approximately 92% to RM69.34 million, up from RM35.76 million in the previous year.

The AFC ratio or the Accrual Free cash ratio is impressive. The figure is definitely better than FY24, improved from 1.3% to -0.7% compare to previous years. This indicates that TG has had a good quality earning in FY25 compared to last years.

Think it is just the public awareness. Also think many retail investors were spooked by TG' s price performance in 2021 and 2022 when the China manufacturers " sapu" all their markets with gloves at cheap and " lelong" price and kept TG high and dry with very poor revenues for 2 years. Fortunately, they have a good financial backgrounds to ride over the raining days,

This chart is telling us that now that its revenue has picked up with reasonably good earnings. The price should not have kept dropping much when it is at the bottom unless there are other good unknown reasons.

This chart is telling us that now that its revenue has picked up with reasonably good earnings. The price should not have kept dropping much when it is at the bottom unless there are other good unknown reasons.

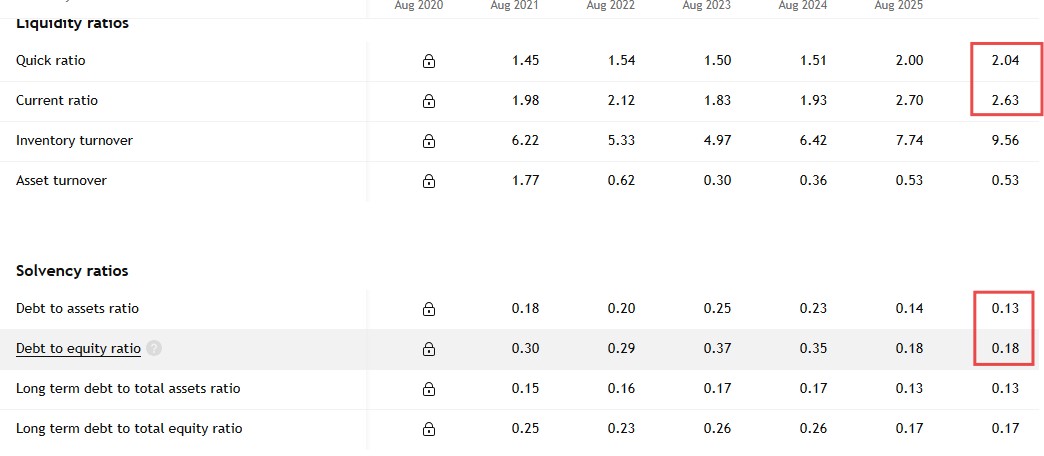

TG has had two years of bad time, In 2022 and 2023, there was a glut of glove with China manufacturers taking over all their businesses away after the Covid subsided in China. They only started to recover in 2024 and 2025 especially after the tariff war started. Given time, TG should regain all its power going up as it has a good financial standing. It now has a quick and current ratio above 2.0 and very low debt, It just lack 2 thing expansioin and plenty of publicity. They were caught unfortunately by the glut of caused by Chinese Manufacturers capturing all the market after the Covid.

https://i.postimg.cc/8ccFKWcL/Screenshot-2026-03-19-075850.jpg

https://i.postimg.cc/8ccFKWcL/Screenshot-2026-03-19-075850.jpg