HPH Trust (HPHT) stood out as one of a potential laggard. It last traded at US$0.130.

Read on to see why it interests me.

Interesting points on HPH Trust

A) Low valuations with P/BV 0.35x

Based on Bloomberg, HPHT trades at 0.35x FY24F P/BV, 1.0x standard deviation below its average 10Y P/BV of 0.6x. Based on Shareinvestor, NAV / share is around US$0.367.

B) Staggering yield of 12.5%!

Based on Bloomberg, HPHT has a staggering yield of 12.5%. If I just annualise its 1HFY24 DPU (adjusted in SGD terms) of 0.8338 SG cents, its dividend yield is 12.8%. Based on Shareinvestor, 2H DPU is usually higher than 1H DPU from 2020 to 2023.

C) Technical chart outlook looks positive

Based on Chart 1 below, it is noteworthy that HPHT&rsquo s volume has consistently traded above its average past 30 day volume of around 4.3m shares for the past seven trading sessions (including today). At the time of writing, HPHT&rsquo s volume traded for today amounts to 7.6m shares.

Indicators such as MACD, OBV, RSI and MFI are strengthening. In fact, OBV has already surpassed the previous peak last seen on 15 and 24 Jul even though HPHT&rsquo s share price has not moved above US$0.135 last closing price on 15 Jul. Furthermore, ADX has risen to around 22.0 amid positively placed DI, signifying the onset of a trend. Based on chart and my manual observation, there seems to be accumulation in this share.

Near term supports: US$0.128 / 0.125 &ndash 0.126 / 0.122 / 0.120

Near term resistances: US$0.132 / 0.134 &ndash 0.136 / 0.140 &ndash 0.141 / 0.145

A sustained breach above US$0.136 with volume expansion is extremely positive and points to an eventual technical measured target of around US$0.150. Conversely, a sustained break below US$0.120 with volume expansion is negative.

D) Downside likely capped around US$0.120 with total potential return at around 47%!

In the previous sell off in Aug, HPHT last traded to a closing low of US$0.120. This was also the low last seen 20 Mar 2024 and 15 Sep 2020. Barring unforeseen circumstances, it is likely that downside may be capped around that level. Based on average analyst target price (by polling HSBC and DBS report), average analyst target price for HPHT is around US$0.175. Together with an estimated dividend yield of around 12.5%, total potential return for HPHT is around 47%! Readers can refer to DBS Research report dated 27 Aug 2024 HERE.

E) Share price laggard compared to other reits

With reference to Table 1 below, HPHT&rsquo s share price is an apparent laggard. It lags behind FTSE ST REIT index and even specific reits with foreign asset exposure. For example, Manulife US Reit has soared 86% over the same period. It is noteworthy that HPHT&rsquo s valuations are on par with Manulife US Reit but Manulife US Reit has no dividends at the moment.

Table 1: HPH Trust share price against others

Source: Ernest&rsquo s compilations

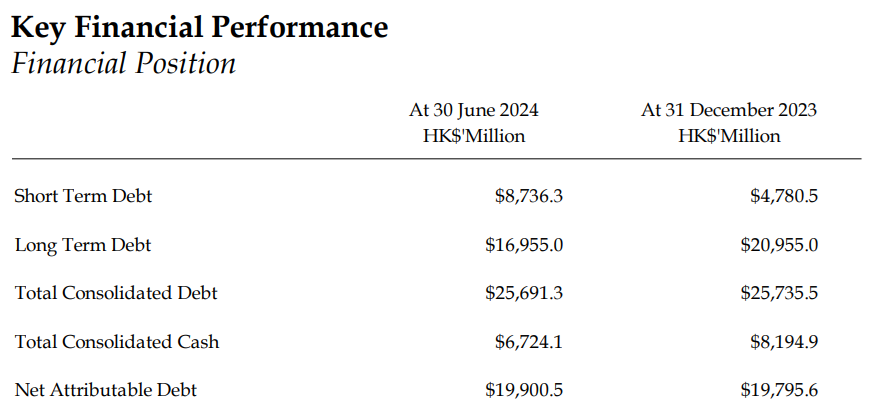

F) Potential rate cut beneficiary

Based on Table 2 below, HPHT has net attributable debt of HKD19.9b. Generally speaking, if interest rates continue to be on a downward trend in the next 1-2 years, it should generally have a positive impact. As at 30 June 2024, 64% of HPH Trust&rsquo s debts are on fixed interest rate. For every 25 basis point decrease in the interest rate, HPHT&rsquo s monthly interest expense would decrease by approximately HK$1.9m.

However, in 1HFY24 results, HPHT mentions that when it refinances its debts amounting to approximately HK$7.8b in Nov 2024 to Mar 2025, the refinancing interest rate may be significantly higher compared to the relatively low interest rate that HPHT currently enjoys from loans drawn 4 &ndash 5 years ago, given the currently high interest rate environment.

To the above point, DBS Research argues that there is a possibility that the decrease in the floating rates may offset the increase in refinancing interest rates. If this happens, it may even reduce overall interest costs, resulting in a DPU increase.

Table 2: HPHT&rsquo s 1HFY24 financial position

Source: Company

As with almost all investments, there are definitely risk factors be aware of.

Possible risk factors to be cautious

A) Weaker than expected economic growth

As HPHT is one of two port operators covering both Hong Kong and Shenzhen, weaker than expected economic growth resulting in less throughput will likely to have an adverse impact on HPHT.

B) FX risks

As HPHT&rsquo s distributions are given out in HK$, a strengthening of SGD against HKD is likely to have an adverse effect on its distributions received in SGD. Since 30 Jun 2024, SGD has strengthened 5.0% against HK$ from 5.7581 to 6.0443.

C) Interest rate risk

Given the amount of debt on its balance sheet and the upcoming HK$7.8b of refinancing in Nov 2024 to Mar 2025, coupled with 36% of their debts are on floating rates, a scenario of higher for longer interest rates is likely to have a negative impact on HPHT.

D) I am not exactly familiar with HPHT

As its my first time looking into HPHT, I may not be exactly familiar in their business and may not have appreciated the risks fully yet.

Conclusion

The above is just my personal write-up on my observation that HPHT seems to be a laggard with attractive valuations of 0.35x FY24F P/BV and 12.5% FY24F dividend yields. As this is my first time looking into HPHT, I may not have fully appreciate the risks yet. Nevertheless, in this market FOMO to buy interest rate cut beneficiaries, one can consider to take a look at HPHT.