If $0.755 support cannot hold then it will be quite scary...

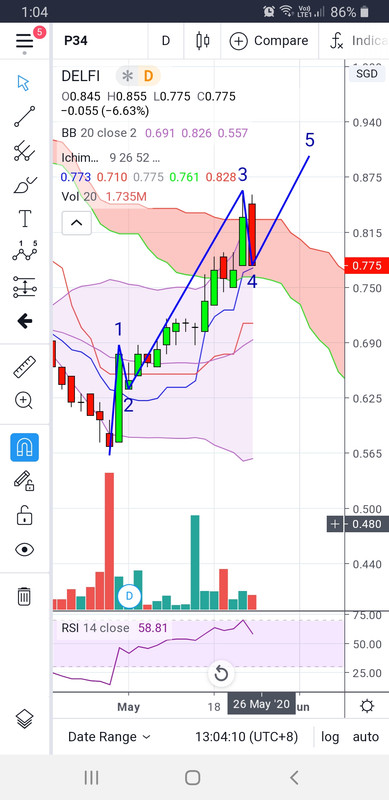

w4 tgt 775

px hit 760 delta 110 dn 49%

day mid bollinger 755 support cannot break

ew still not break but over corrected

cloud baseline support 710

if uturn at 760

then w5 tgt 885

px hit 760 delta 110 dn 49%

day mid bollinger 755 support cannot break

ew still not break but over corrected

cloud baseline support 710

if uturn at 760

then w5 tgt 885

Acewind ( Date: 04-Jun-2020 19:16) Posted:

|

Hi master yuan, is w5 still valid ?

px hit low of 760 today.

px hit low of 760 today.

SgYuan ( Date: 25-May-2020 13:08) Posted:

|

Very cheap...market sure notice soon esp the private funds...we just entered BULL MARKET last..no hurry

Huge emerging consumer Indonesia market....where esle to find such cheap stocks but in SGX...

pay dividends every year....please dont delist...nothing left here

Huge emerging consumer Indonesia market....where esle to find such cheap stocks but in SGX...

pay dividends every year....please dont delist...nothing left here

It' s closest peer Mayora is at year high and almost at 52-wk high with the reopening of Indonesia. USD/IDR has also corrected substantially, with rupiah rallying > 2% today to be one of the top performing EM currencies. Cocoa prices remain depressed so effectively all macro tailwinds are in their favour yet market is not pricing them fairly at all. Don' t forget the Raya effect which should boost 2Q performance given that they guided at AGM that their distribution channels to minimarts had limited impact.

Should be a matter of time that market appreciates this undervalued stock. Being Indonesia' s leading player, it trades at less than 12x PE with EV/EBITDA of ~5x. It also maintained free cash flow positive consistently for the last 4 years since the restructuring - quite frankly, it probably makes sense for the Chuang family to just privatise the stock and go elsewhere since the local market don' t appreciate its value.

Should be a matter of time that market appreciates this undervalued stock. Being Indonesia' s leading player, it trades at less than 12x PE with EV/EBITDA of ~5x. It also maintained free cash flow positive consistently for the last 4 years since the restructuring - quite frankly, it probably makes sense for the Chuang family to just privatise the stock and go elsewhere since the local market don' t appreciate its value.

Delfi seems like a good, sound company with good prospects. I wonder why its liquidity and price are always so poor and it rarely seems to rally with the broader market.

$0.76 support line must hold strong...

Good observation and thanks for highlighting - guess the support line remains defended at this point. The stock looks slightly exhausted from the good rally over the past weeks, we could probably see some consolidation at present levels?

Acewind ( Date: 28-May-2020 11:28) Posted:

|

Thank you sir for sharing

SgYuan ( Date: 28-May-2020 11:22) Posted:

|

Today is t+4 of last week high 86. Those who cannot hold is selling , which is why there is a selldown. Dyodd

cloud support 761

- see the ichi cloud red shaded 761

- next support cloud baseline red line 710

- see the ichi cloud red shaded 761

- next support cloud baseline red line 710

n3wbie ( Date: 28-May-2020 11:02) Posted:

|

Thanks for sharing - if 775 is breached, any indication on where the next level of support might be?

SgYuan ( Date: 25-May-2020 13:10) Posted:

|

day chart

day chart

ew on w4 tgt 774 dn 38.2%

- px hit 775

- conversion line 773

- cloud 710

- support cannot break then w5 come

w5 125 tg 900

ew on w4 tgt 774 dn 38.2%

- px hit 775

- conversion line 773

- cloud 710

- support cannot break then w5 come

w5 125 tg 900

DBS TP better than ours expectation😁 $1.00 first then move up to their TP

bluetoes ( Date: 22-May-2020 13:03) Posted:

|

DBS Group Research . Equity 22 May 2020

Sweetly valued

Maintain BUY with lower TP of S$1.08. We maintain our positive stance on DELFI as we see resilient earnings despite the impact from COVID-19. Although COVID-19 has brought about lower production volumes in recent months, its business as a food staple producer remains on-going, with decent demand expected during the Lebaran period and production leaning towards higher-margin ones. We believe recent FX weakness of IDR against USD would have minimal impact on margins as raw materials have been secured for up to 18 months. Factoring regional disruptions to businesses due to governmental laws to curb the virus regionally, we impute in lower sales volume in FY20F and a gradual recovery for FY21F. Nonetheless, we expect earnings growth in FY21F to remain strong, led by a recovery from recent months&rsquo disruptions and its premiumisation strategy. Valuations remain compelling at 11.9x FY20F earnings or -1.5 SD of is 4-year historical mean and below 20-22x peer average. Dividend yield is attractive at 4.2%.

Where we differ: We believe sustained EPS growth will lead to the resumption of the relationship between its trailing-12- months (TTM) EPS and share price. Potential catalysts: We have always seen DELFI as a strong takeover candidate due to its strong general trade market share in Indonesia and low trading liquidity.

Valuation: Maintain BUY with a lower TP of S$1.08. Our TP is based on a blended FY20-21F PE of 18x, which is -1.0SD below its 4-year historical mean.

https://s3-ap-southeast-1.amazonaws.com/investingnote-production-webbucket/attachments/6cd4ed68a9a6612e41256186d073a3a7f3b9053e.pdf?1590122899

Sweetly valued

Maintain BUY with lower TP of S$1.08. We maintain our positive stance on DELFI as we see resilient earnings despite the impact from COVID-19. Although COVID-19 has brought about lower production volumes in recent months, its business as a food staple producer remains on-going, with decent demand expected during the Lebaran period and production leaning towards higher-margin ones. We believe recent FX weakness of IDR against USD would have minimal impact on margins as raw materials have been secured for up to 18 months. Factoring regional disruptions to businesses due to governmental laws to curb the virus regionally, we impute in lower sales volume in FY20F and a gradual recovery for FY21F. Nonetheless, we expect earnings growth in FY21F to remain strong, led by a recovery from recent months&rsquo disruptions and its premiumisation strategy. Valuations remain compelling at 11.9x FY20F earnings or -1.5 SD of is 4-year historical mean and below 20-22x peer average. Dividend yield is attractive at 4.2%.

Where we differ: We believe sustained EPS growth will lead to the resumption of the relationship between its trailing-12- months (TTM) EPS and share price. Potential catalysts: We have always seen DELFI as a strong takeover candidate due to its strong general trade market share in Indonesia and low trading liquidity.

Valuation: Maintain BUY with a lower TP of S$1.08. Our TP is based on a blended FY20-21F PE of 18x, which is -1.0SD below its 4-year historical mean.

https://s3-ap-southeast-1.amazonaws.com/investingnote-production-webbucket/attachments/6cd4ed68a9a6612e41256186d073a3a7f3b9053e.pdf?1590122899

You means today reach 90cts? If cross 88cts I will top up some more😁

Sgvale ( Date: 21-May-2020 15:29) Posted:

|

0.90 can reach?

$1.00 is getting nearer and nearer😯

Something brewing?