Take some profit 1st.

Sold trading portion, Keep holding portion (same old portion).

Sold trading portion, Keep holding portion (same old portion).

superstartup ( Date: 22-Jan-2026 12:37) Posted:

|

https://links.sgx.com/1.0.0/corporate-announcements/40LPI3APHMELU5E0/873118_Nam%20Cheong_Vessel%20Sales.pdf

Don' t like that.

I added more at 109.

But will be glad to collect more at lower price too (so long price not stagnant. movement either way is good).

I added more at 109.

But will be glad to collect more at lower price too (so long price not stagnant. movement either way is good).

melody88 ( Date: 22-Jan-2026 11:51) Posted:

|

cannot break 1.12.... coming down to 1.06

need to break 1.12, then next wave 1.17

Get Ready

| #4 Looking Toward a Normalised 2026 |

Investors tracking the 2025 performance may have noticed some weakness in charter income during the first half of the year.

Mr. Cheong clarified that the lower utilization rates in Q1 and Q2 were due to the company preparing vessels to commence long-term charter contracts.

This " downtime" was an investment in future stability.

By Q3 2025, revenue began to rise as these long-term contracts kicked in.

-

4Q 2025: Expected to reflect a more " normalised" operational state as the fleet fully engages with its secured contracts. -

2026 Outlook: With 60% of the fleet already secured under long-term contracts and six new vessels joining the fleet, 2026 is poised to be a year of high visibility and steady earnings.

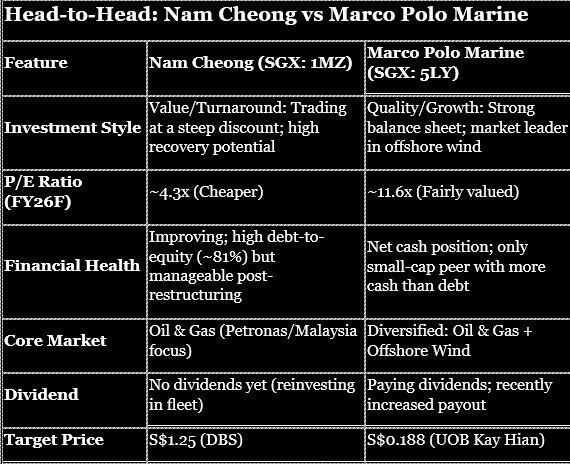

hope to see 1.12 soon next week. Target Price by DBS $1.25

Above $1.10 : )

Ah Cheong gonna to cheong and breakout...  WATCH :)

WATCH :)

WATCH :)| Solubl ( Date: 15-Jan-2026 10:50) Posted: |

i am gonna exit when it hits 130..

rising ships to track bullish oil markets, watch out for MPM too

there is no public information about any meeting. it has risen very rapidly, so good time to book some profit into it. sold 1/3rd of my position.

wondering how' s the meeting goes today? hope there is good news to break through 1.10

Understanding Nam Cheong as a Potential Multi-Bagger: A Beginner' s Guide

What is ROCE and Why Does It Matter?

Think of ROCE (Return on Capital Employed) as a report card for how efficiently a company uses the money invested in it to make profits. Imagine you gave a friend $100 to start a small business. ROCE tells you: for every dollar your friend has invested, how much profit are they actually generating?

In Nam Cheong' s case, they' re generating 24 cents of profit for every dollar invested&mdash which is excellent. To put this in perspective, other machinery companies on average only generate about 5.3 cents per dollar. So Nam Cheong is performing roughly 4.5 times better than its industry peers.

Nam Cheong' s Impressive Journey

From losses to profits: Five years ago, Nam Cheong was losing money. Now they' re profitable and generating substantial returns. This turnaround is significant because it shows the company has figured out how to operate successfully.

Reinvestment for growth: Nam Cheong has increased the capital (money) it' s investing in the business by 234%. This is actually a good sign&mdash it means the company found profitable opportunities worth investing in. Rather than hoarding cash, they' re putting money back into the business, which is what you want to see in a potential multi-bagger stock (a stock that could multiply in value several times over).

The " Compounding Machine" Concept

The article describes what analysts look for in potential multi-baggers:

-

High ROCE ✓ (Nam Cheong has this at 24%) -

Growing capital employed ✓ (Nam Cheong is expanding operations)

When you combine these two factors, you get what' s called a " compounding machine" &mdash a business that earns great returns and continuously reinvests those profits to earn even more returns. It' s like a snowball rolling downhill, getting bigger and bigger over time.

Financial Health Indicator

The article also notes that Nam Cheong' s reliance on short-term creditors decreased to 18% of total assets. In simpler terms: the company is becoming less dependent on borrowing or owing suppliers for operational money. Instead, it' s self-funding its growth through its own profits. This is a positive sign of financial stability.

The Caution

While the trends are promising, the article mentions there are 3 warning signs worth investigating before investing. The article doesn' t spell out what these are, so you' d need to research those separately. No company is risk-free, and even strong fundamentals don' t guarantee future success.

Bottom Line

Nam Cheong appears to fit the profile of a potential growth opportunity: it' s turned around from unprofitable to highly profitable, it' s reinvesting in expansion, and it' s doing so from a position of financial strength. The stock price has already reflected some of this optimism over the past year, so investors are already aware of these positive trends. The key question for any potential investor is whether the company can maintain and improve these trends going forward&mdash which is why the article recommends digging deeper into future analyst forecasts and understanding those warning signs.

melody88 ( Date: 12-Jan-2026 11:29) Posted:

|

hopefully tmr meeting will bring good news and bring nam cheong to next level & break 1.10

https://uk.finance.yahoo.com/news/investors-encouraged-nam-cheongs-sgx-221503402.html

Just to clarify if you' re unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Nam Cheong, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.24 = RM256m ÷ (RM1.3b - RM245m) (Based on the trailing twelve months to September 2025).

Therefore, Nam Cheong has an ROCE of 24%. In absolute terms that' s a great return and it' s even better than the Machinery industry average of 5.3%.

We' re delighted to see that Nam Cheong is reaping rewards from its investments and is now generating some pre-tax profits. Shareholders would no doubt be pleased with this because the business was loss-making five years ago but is is now generating 24% on its capital. In addition to that, Nam Cheong is employing 234% more capital than previously which is expected of a company that' s trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you' re unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Nam Cheong, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.24 = RM256m ÷ (RM1.3b - RM245m) (Based on the trailing twelve months to September 2025).

Therefore, Nam Cheong has an ROCE of 24%. In absolute terms that' s a great return and it' s even better than the Machinery industry average of 5.3%.

We' re delighted to see that Nam Cheong is reaping rewards from its investments and is now generating some pre-tax profits. Shareholders would no doubt be pleased with this because the business was loss-making five years ago but is is now generating 24% on its capital. In addition to that, Nam Cheong is employing 234% more capital than previously which is expected of a company that' s trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

me too also added some last friday and this morning. hope it will hit to the target price set bu DBS @ $1.26.

Added more today.

For tomorrow SIAS briefing.

Hopefully DBS and other brokerage houses also attend. And we can have upgrade by DBS / initiation of coverage by other houses.

For tomorrow SIAS briefing.

Hopefully DBS and other brokerage houses also attend. And we can have upgrade by DBS / initiation of coverage by other houses.

Slow & steady.

superstartup ( Date: 07-Jan-2026 09:50) Posted:

|