| Latest Forum Topics / CreditBureauAsia Last:1.14 -- |

|

|

creditbureauasia

|

||||||||

|

john_ric

Supreme |

23-Feb-2023 18:22

|

|||||||

|

x 0

x 0 Alert Admin |

xd = 4may pay on 19 may |

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

spursfan

Supreme |

23-Feb-2023 17:29

|

|||||||

|

x 0

x 0 Alert Admin |

NEWS RELEASE All Credit Bureau Asia&rsquo s operating entities delivered positive growth in FY2022. Final dividend of 1.70 Singapore cents, bringing full year dividend to 3.40 Singapore cents. FY2022 Revenue grew 7% to S$ 48.6 million FY2022 Net Profit Before Tax grew 5% to S$22.9 million FY2022 PATMI grew 7% to S$8.4 million Recommending a final dividend of 1.70 Singapore cent per share, bringing the full dividend for FY2022 to 3.40 Singapore cents per share. https://links.sgx.com/1.0.0/corporate-announcements/Q4KCH9FTEIYJ2N2A/747473_CBA%20FY2022%20Results%20Media%20Release.pdf |

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

|

||||||||

|

Joelton

Supreme |

01-Aug-2022 16:27

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia aims for &lsquo multiplier effect&rsquo with digital banks

CREDIT Bureau Asia (CBA), which runs the largest consumer credit bureau in Singapore, is eager for the local digital banks to finally launch.

CBA&rsquo s growth is linked to the growth of its member network. The inclusion of a new financial institution in Credit Bureau (Singapore)&rsquo s (CBS) platform has a ripple effect, amplifying the data pool for all members while creating more revenue opportunities for the group.

CBS' fees are based on how many reports it generates for its customers (the banks), whether each report comes with a score, the size of the portfolio the customer is monitoring, and the number of triggers or alerts sent out.

When an individual signs up for a new credit card or loan with a digital bank, the bank uses CBS&rsquo platform to generate a credit report.

But it is not only the digital banks that will generate these reports. If the consumer has existing relationships with other banks, CBS&rsquo monitoring system alerts them to the consumer&rsquo s increased credit exposure. The banks might decide to review that customer&rsquo s status, prompting them to pull reports of their own.

Lenders may also place certain consumers within a portfolio with a higher frequency of reviews, due to higher credit exposures.

&ldquo It becomes a multiplier effect,&rdquo said CBA&rsquo s executive director, William Lim, in an interview with The Business Times.

There are 5 digital banks that can operate in Singapore. Sea&rsquo s Maribank, Grab and Singtel&rsquo s GXS, and Standard Chartered and the National Trades Union Congress (NTUC)&rsquo s Trust Bank are digital full banks. Ant Group&rsquo s ANext and Green Link Digital Bank operate under a digital wholesale bank licence.

One of the banks &ndash Lim declined to say which &ndash signed up as a customer in Q1 this year, and CBA has started recognising revenue from the deal. &ldquo They signed a volume purchase and bulk review agreement, so as to enjoy slightly better pricing. Typically, such contracts are for 2 or 3 years and may come with a fixed monthly spend for certain agreements,&rdquo Lim said.

CBS drives the lion&rsquo s share of CBA&rsquo s revenue. During the year ended Dec 31, 2021, the subsidiary accounted for about 43 per cent of CBA&rsquo s S$45.4 million topline. Group net profit was S$7.8 million, rising 14.6 per cent from a year ago.

CGS-CIMB analyst Andrea Choong said the ramp-up of digital banks in Singapore is key to progressive earnings accretion for CBA. &ldquo This will depend greatly on the type of products rolled out and the adoption of both DFBs (digital full banks) and DWBs (digital wholesale banks) by the marketplace,&rdquo she wrote in a Jun 12 report.

She added, however, that earnings visibility for the group is likely to emerge only in the medium term, once the banks firm up their growth strategies.

Resilient model

CBA has plans to deepen its regional presence, but rising interest rates could have an immediate impact on its business as consumers scale back on borrowing.

Lim said new credit card applications fell 30-40 per cent during the pandemic, as consumer sentiment took a hit. According to figures from the Monetary Authority of Singapore, credit card transactions dropped from S$67 billion in 2019 to S$56.7 billion in 2020.

Still, Lim believes the company will get through the downturn relatively unscathed. &ldquo New applications will get hit, but reviews will get a kick,&rdquo he said.

Lim expects portfolio monitoring frequency to increase and the number of reviews to jump as banks tighten their risk monitoring. He noted that the group&rsquo s revenue continued to grow even throughout the global financial crisis, the outbreak of Sars (severe acute respiratory syndrome) and the Covid-19 pandemic.

As at December 2021, CBA&rsquo s financial institution (FI) data business serves more than 200 FI members across Singapore, Cambodia and Myanmar, including banks, microfinance institutions, leasing companies and rural credit operators.

In Singapore and Malaysia, the group has joint ventures with American analytics company Dun & Bradstreet to provide a wide range of business information and risk management services under the non-FI data business.

Although CBA&rsquo s regional expansion is in its early stage, the company has a first-mover advantage. It operates the only credit bureaus in Cambodia and Myanmar. In FY2021, revenue from its joint venture Credit Bureau (Cambodia) grew 24.9 per cent to S$12.5 million.

CBA expects its bureau in Myanmar to begin generating revenue soon, following a prolonged delay indirectly caused by the political situation in the country. It now has 31 banks uploading data to its platform, up from 10 a year ago when the bureau was announced.

Lim said the company is evaluating acquisition opportunities within South-east Asia and North Asia, Japan, South Korea and certain parts of Australia and New Zealand. It will focus on complementary businesses instead of credit bureaus. As at Dec 31, 2021, CBA had cash and bank balances of S$53.5 million and no debt.

The company&rsquo s share price has fallen 2.94 per cent since it debuted on the Singapore Exchange in December 2020, to close at S$0.99 on Jul 29. That is still 6.5 per cent above its initial public offering price of S$0.93, and gives the counter a market capitalisation of S$227 million and a price-to-earnings ratio of 29.1 times.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

john_ric

Supreme |

23-Feb-2022 18:02

|

|||||||

|

x 0

x 0 Alert Admin |

fy results: FY2021 Revenue grew 5% to S$45.4 million - FY2021 Net Profit Before Tax grew 5% to S$21.7 million - FY2021 PATMI grew 15% to S$7.8 million - Declares a final dividend of 1.70 Singapore cent per share, bringing the full dividend for FY2021 to 3.40 Singapore cents per share. |

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

john_ric

Supreme |

08-Feb-2022 13:38

|

|||||||

|

x 0

x 0 Alert Admin |

last year this crap share only gives one div.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

|

||||||||

|

Joelton

Supreme |

24-Jan-2022 09:34

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia, UOL and MediNex chairs add to stakes

FOR the 5 trading sessions that spanned Jan 14 to 20, the Straits Times Index (STI) gained 1.2 per cent, with the FTSE China A50 Index gaining 1.9 per cent, the Hang Seng Index gaining 2.1 per cent and the FTSE Bursa Malaysia KLCI declining 2.6 per cent.

Within the STI, OCBC, OCBC Bank: O39 +0.08% UOB, UOB: U11 +0.23% Singapore Telecommunications, Singtel: Z74 +0.4% DBS DBS: D05 -1.22% Group Holdings and Sembcorp Industries Sembcorp Ind: U96 0% received the highest net institutional inflows for the 5 sessions.

Outside the STI, Singapore Press Holdings, SPH: T39 -0.43% Keppel Infrastructure Trust, Kep Infra Tr: A7RU -0.89% Ascott Residence Trust, Ascott Trust: HMN -0.94% AEM Holdings AEM SGD: AWX -2.37% and Suntec Reit Suntec Reit: T82U +0.65% received the highest net institutional inflows for the period.

Overall, institutions were net buyers over the 5 sessions, with S$256 million of net inflow, while UMS Holdings, UMS: 558 -2.22% Nanofilm Technologies International Nanofilm: MZH -1.34% and Keppel DC Reit Keppel DC Reit: AJBU -0.44% reported the highest net institutional outflows.

Share buybacks

There were 14 primary-listed stocks conducting share buybacks over the 5 sessions with a total consideration of S$18.0 million, up from S$12.0 million during the previous corresponding period.

OCBC led the consideration tally, buying 800,000 shares at an average price of S$12.30 per share.

SHS Holdings SHS: 566 0% led the buyback consideration of non-STI stocks, buying back 12.5 million shares at an average price of 15.5 cents per share.

Secondary-listings Hongkong Land HongkongLand USD: H78 +0.37% and Jardine Matheson Holdings JMH USD: J36 +0.81% also bought back shares over the 5 sessions.

Director and substantial shareholder transactions

The 5 trading sessions saw more than 60 changes in director interests and substantial shareholdings filed for close to 30 primary-listed stocks.

This included 13 company director acquisitions with 2 disposals filed, while substantial shareholders filed 3 acquisitions and 7 disposals.

Credit Bureau Asia

On Jan 18, Credit Bureau Asia CreditBureauAsia: TCU 0% founder, executive chairman and CEO Koo Chiang acquired 1,425,000 shares of the company for a consideration of S$1,482,000 at an average price of S$1.04 per share.

This increased his direct interest in the company from 63.40 per cent to 64.00 per cent.

His preceding acquisition of Credit Bureau Asia shares was between Nov 26 and Dec 2, which saw him acquire 537,300 shares at S$1.21 per share.

Since establishing the credit information business in Singapore in 1993, Koo has over 20 years of experience in the credit information industry and has been instrumental to the success and expansion of the group over the past 2 decades.

On Dec 24, Credit Bureau (Cambodia) announced a commitment of US$1 million in support of the National Financial Inclusion Strategy to promote and strengthen financial inclusion over the next 5 years in Cambodia.

The company noted back in April that as part of its efforts in advocating for greater economic inclusion, it had taken part in various initiatives through Credit Bureau (Cambodia) to help equip families, students and individuals in the country with financial knowledge and to improve financial literacy.

Credit Bureau Asia is expected to report its FY21 (ended Dec 31) results towards the end of February, after reporting in August that its H1FY21 (ended Jun 30) revenue grew 8.5 per cent to S$22.3 million.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

civicavantae

Member |

10-Jan-2022 16:55

|

|||||||

|

x 0

x 0 Alert Admin |

Hi, just like to know why this counter dont really go up? Thanks. | |||||||

| Useful To Me Not Useful To Me | ||||||||

|

Joelton

Supreme |

06-Dec-2021 10:40

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia

Between Nov 26 and Dec 2, Credit Bureau Asia CreditBureauAsia: TCU -1.6% founder, executive chairman and CEO Koo Chiang acquired 537,300 shares of the company for a consideration of S$651,479 at an average price of S$1.21 per share.

This increased his direct interest from 68.10 per cent to 68.30 per cent.

His preceding acquisitions included 53,200 shares at S$1.16 per share, between Nov 17 and 22 and 138,300 shares at S$1.15 per share between Nov 11 and 16.

Since establishing the credit information business in Singapore in 1993, he has over 20 years of experience in the credit information industry and has been instrumental in the success and expansion of the group over the past 2 decades.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

|

||||||||

|

Joelton

Supreme |

29-Nov-2021 09:28

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia

Between Nov 17 and 22, Credit Bureau Asia CreditBureauAsia: TCU -2.59% founder, executive chairman and CEO Koo Chiang acquired 53,200 shares of the company for a consideration of S$61,750, at an average price of S$1.16 per share. Koo' s direct interest in Credit Bureau Asia is 68.10 per cent.

His preceding acquisitions included 138,300 shares at S$1.15 per share between Nov 11 and 16 and 7,600 shares acquired at S$1.25 per share on Sep 10.

In August, Credit Bureau Asia noted that its subsidiary, Credit Bureau Singapore, had commenced operations of the Moneylenders Credit Bureau, with a positive contribution to the group expected in the next financial year.

In addition, the company noted that Credit Bureau Singapore was close to finalising agreements with the digital bank licensees and will make the necessary announcements at the appropriate time.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

Joelton

Supreme |

22-Nov-2021 09:42

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia

Between Nov 11 and 16, Credit Bureau Asia CreditBureauAsia: TCU -0.86% founder, executive chairman and CEO Koo Chiang acquired 138,300 shares of the company for a consideration of S$159,482, at an average price of S$1.15 per share.

This took his direct interest in Credit Bureau Asia from 68.00 per cent to 68.10 per cent.

His preceding acquisition in the credit information business was on Sep 10, with 17,600 shares acquired at S$1.25 per share.

Since establishing the credit information business in Singapore in 1993, Koo has over 20 years of experience in the credit information industry and is responsible for the group' s strategic direction and overseeing its overall growth and performance.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

civicavantae

Member |

09-Nov-2021 14:55

|

|||||||

|

x 0

x 0 Alert Admin |

Why is CBA dropping sharply?

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

Shane1702

Member |

22-Sep-2021 13:36

|

|||||||

|

x 0

x 0 Alert Admin |

Why this counter just keep dipping?

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

|

||||||||

|

Joelton

Supreme |

21-Sep-2021 09:49

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia unit partners with Quantexa to introduce AI-driven compliance and risk solutions

Credit Bureau Asia has announced that its subsidiary Dun & Bradstreet (Singapore) (D& B) is collaborating with data and analytics firm Quantexa to introduce compliance and risk solutions targeted at financial institutions, insurance companies, government entities and multinational corporations in Singapore.

According to a news release by CBA on Sept 20, the solutions introduced by D& B and Quantexa will enable companies to leverage on contextual decision intelligence to increase investigation efficiency, optimize their compliance processes and better address regulatory demands.

Audrey Chia, CEO of D& B, highlights the importance of establishing robust, digitally-enabled and data-driven compliance programmes in the face of growing compliance risk and fraud globally.

&ldquo Combining Quantexa&rsquo s advanced solutions and D& B&rsquo s comprehensive data, we believe we can help companies automate their compliance processes through artificial intelligence, reduce losses arising from compliance risks and keep their compliance efforts sustainable in the long-term,&rdquo she says.

Through the partnership, D& B and Quantexa will provide a single contextual view of data across directors, shareholders, and beneficial owners in their global dataset. Quantexa&rsquo s software enables Network Linking, applying AI and graph-based analytics to discover hidden risk which improves trusted operational decision making across areas such as Know Your Customer (KYC), anti-money laundering and counter fraud.

&ldquo We&rsquo re delighted to expand our relationship with CBA and D& B as we widen our footprint in Southeast Asia. Jointly, we are able to offer ground-breaking data and analytics capabilities for organizational risk identification accuracy and efficiency,&rdquo says Mark McNerney, director of alliances at Quantexa.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

PhillipTan

Supreme |

21-Sep-2021 05:45

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia unit partners with Quantexa to introduce AI-driven compliance and risk solutionsCredit Bureau Asia has announced that its subsidiary Dun & Bradstreet (Singapore) (D& B) is collaborating with data and analytics firm Quantexa to introduce compliance and risk solutions targeted at financial institutions, insurance companies, government entities and multinational corporations in Singapore.According to a news release by CBA on Sept 20, the solutions introduced by D& B and Quantexa will enable companies to leverage on contextual decision intelligence to increase investigation efficiency, optimize their compliance processes and better address regulatory demands. Audrey Chia, CEO of D& B, highlights the importance of establishing robust, digitally-enabled and data-driven compliance programmes in the face of growing compliance risk and fraud globally. " Combining Quantexa' s advanced solutions and D& B' s comprehensive data, we believe we can help companies automate their compliance processes through artificial intelligence, reduce losses arising from compliance risks and keep their compliance efforts sustainable in the long-term," she says. Through the partnership, D& B and Quantexa will provide a single contextual view of data across directors, shareholders, and beneficial owners in their global dataset. Quantexa' s software enables Network Linking, applying AI and graph-based analytics to discover hidden risk which improves trusted operational decision making across areas such as Know Your Customer (KYC), anti-money laundering and counter fraud. " We' re delighted to expand our relationship with CBA and D& B as we widen our footprint in Southeast Asia. Jointly, we are able to offer ground-breaking data and analytics capabilities for organizational risk identification accuracy and efficiency," says Mark McNerney, director of alliances at Quantexa. |

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

Joelton

Supreme |

20-Sep-2021 10:38

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia

On Sept 10, Credit Bureau Asia CreditBureauAsia: TCU +0.81% founder & executive chairman Koo Chiang acquired 17,600 shares of the company for a consideration of S$21,977, at an average price of S$1.25 per share.

Mr Koo maintains a direct interest in Credit Bureau Asia of 68.00 per cent.

Since establishing the credit information business in Singapore in 1993, Mr Koo has been instrumental to the success and expansion of the group.

On Aug 5, the leading player in credit and risk information solutions in South-east Asia, reported that its H1FY21 (ended June 30) revenue increased 8.5 per cent from H1FY20 to S$22.26 million, with net profit before tax increasing 0.5 per cent from H1FY20, to S$10.95 million.

With the results, Mr Koo highlighted that going forward, the company is working on a series of projects such as the Moneylenders Credit Bureau and potential digital bank customers, which will continue to drive its business forward.

Mr Koo added that Credit Bureau Asia is also in dialogue with several parties in the region to forge alliances to bring the business to greater heights.

The Board of Credit Bureau Asia also declared an interim dividend of 1.70 cents per share for its H1FY21, which went ex-dividend on Aug 26, with a payment date of Sept 15.

The interim dividend represented about 100 per cent of the group' s PATMI, exceeding the group' s stated dividend policy in the Nov 2020 prospectus that recommended at least 90.0 per cent of net profit after tax attributable to its shareholders for FY21 and FY22.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

PhillipTan

Supreme |

11-Aug-2021 02:32

|

|||||||

|

x 0

x 0 Alert Admin |

CGS-CIMB lowers TP on Credit Bureau Asia to $1.43 on lower growth assumptions post-1H21 resultsDespite missing revenue expectations in 1HFY2021, Credit Bureau Asia (CBA) has initiatives in the pipeline that will drive a stronger latter half of the year, say CGS-CIMB Research analysts Andrea Choong and Darren Ong.In an Aug 6 note, Choong and Ong are maintaining " add" on the company with a lowered target price of $1.43 from $1.53 on Aug 2. The new target price represents an upside of 10.9%. Listed on the Singapore Exchange (SGX) since Dec 3, 2020, CBA operates as a credit and risk information solutions (CRIS) provider. It aggregates and repackages credit information into useable reports and data packets for sale to its customers, which span both financial institutions (FI) and non-FI clientele. Their products include one-off reports for loan applications, pre-employment checks and pre-screening of business partners, as well as customised monitoring services for higher-risk exposures. CBA delivered a 1HFY2021 revenue growth of 8.5% to $22.3 million but missed Choong and Ong' s expectations by 8%. Adjusting for one-off items (listing expenses, job support scheme grants, disposal of Credit Bureau Malaysia), 1HFY2021 profit after tax (PAT) rose 15% y-o-y to $8.8 million, forming 43% of their FY2021F forecast. " The miss came mainly from a relatively slower pace of revenue growth in the non-FI data business, which expanded 4.9% y-o-y to $12.6 million in 1HFY2021 nonetheless. Earnings growth from the FI data segment rose comparably faster at 13.4% y-o-y to $9.7 million in 1HFY2021, supported by stronger demand for new credit applications and reviews," write Choong and Ong. CBA declared its inaugural interim dividend per share (DPS) of 1.7 cents, implying a 100% dividend payout ratio &mdash ahead of management' s 90% guidance for FY2021F-22F. " However, we cut our DPS estimates to 3.7 cents in FY2021F, in line with our lower earnings estimates," say Choong and Ong. Choong and Ong expect a stronger 2HFY2021F for CBA from sustained volume growth in bulk risk reviews and new credit applications from its FI data business (higher profit margins) and new initiatives, such as cross-selling credit information and product development using data from the Moneylenders Credit Bureau, and leveraging on its current data pool to develop analytics solutions. The Credit Bureau Act came into effect in May 2021, allowing the Monetary Authority of Singapore to license and supervise credit bureaus in Singapore. To this end, CBA will apply (by end-2021) for the sole licence to collect and use commercial credit information from FIs. Discussions are underway to sign on all four new digital banks in Singapore as members of Credit Bureau Singapore. " While providing volume upside, we are cognisant that two of the four new licences issued are digital wholesale banks, which would garner lower (although higher-valued) volumes. CBA' s Cambodian operations continued to execute well in 1HFY2021, with higher credit report sales. In Myanmar, CBA has signed up some 30 FIs as bureau members and hopes to be operational by end-FY2021F." As at 3.56pm, shares in Credit Bureau Asia are trading flat at $1.29, or 31.35 times CGS-CIMB' s price-to-earnings forecast for the year. |

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

royalrumble

Member |

10-Aug-2021 00:02

|

|||||||

|

x 0

x 0 Alert Admin |

The profit for the period is Less than previous quarter The profit for the period is Less than previous quarter

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

Shane1702

Member |

09-Aug-2021 14:44

|

|||||||

|

x 0

x 0 Alert Admin |

Is this results and dividend disappointing? The stock seems to go down instead.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

Joelton

Supreme |

06-Aug-2021 10:20

|

|||||||

|

x 0

x 0 Alert Admin |

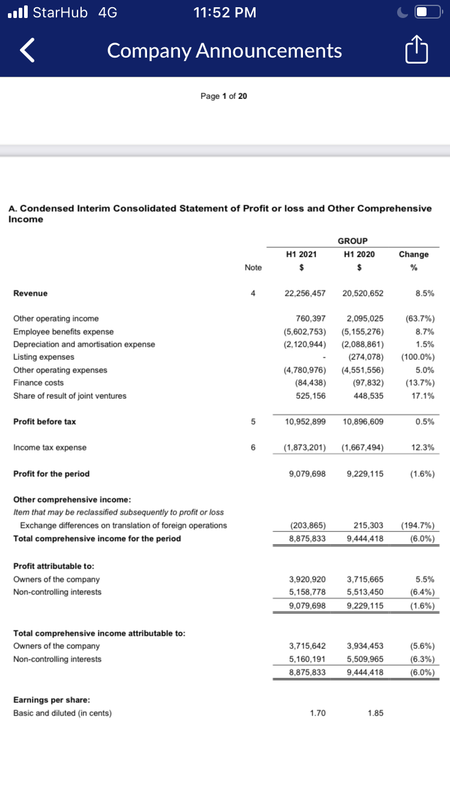

Credit Bureau Asia sees 5.5% rise in 1H2021 earnings declares maiden dividend of 1.7 cents

Credit Bureau Asia (CBA) reported earnings of $3.9 million in its 1HFY21 ended June, a 5.5% increase from the $3.7 million posted in the year before.

On a fully diluted basis, this translates to earnings per share of 1.70 cents, compared to 1.85 cents in 1HFY20.

With this, the group&rsquo s net asset value per ordinary share came in at 20.54 cents on Jun 30, up from 18.93 cents on Dec 30.

Revenue for the first six months of the year grew 8.5% to $22.3 million on the back of strong performance of both its financial institution (FI) and non-financial (non-FI) institution data businesses.

Revenue from the group&rsquo s FI data segment was up 13.4% to $9.7 million thanks to strong demand from the financial industry such as in new credit card applications and credit reviews.

As at June 30, CBA&rsquo s cash and cash equivalents stood at $50.6 million, up from $24.5 million in the year before.

The group has declared an interim dividend of 1.7 cents per share &ndash which represents about 100% of its PATMI of $3.9 million.

The maiden pay out exceeds the group&rsquo s dividend policy stated in its prospectus of recommending at least 90.0% of net profit after tax attributable to its shareholders for the financial years ending FY2021 and FY2022.

Going forward, CBA says its &ldquo business model is defensive to business cycles and pandemics and despite Covid-19, our business continues to grow and perform well during this period&rdquo .

It notes that travel restrictions could present some inconvenience as it looks to forge alliances and expand its business and footprint in the region.

Still it expects positive contributions from it' s the commencement of its subsidiary&rsquo s operations at Moneylenders Credit Bureau.

The subsidiary &ndash Credit Bureau Singapore - is now close to finalising agreements with the Digital Bank Licensees.

As for its investments in Myanmar, the group says it is working closely with the relevant stakeholders and preparing Myanmar Credit Bureau to be fully operational before the end of FY2021.

|

|||||||

| Useful To Me Not Useful To Me | ||||||||

|

PhillipTan

Supreme |

06-Aug-2021 01:38

|

|||||||

|

x 0

x 0 Alert Admin |

Credit Bureau Asia sees 5.5% rise in 1H2021 earnings declares maiden dividend of 1.7 centsCredit Bureau Asia (CBA) reported earnings of $3.9 million in its 1HFY21 ended June, a 5.5% increase from the $3.7 million posted in the year before.On a fully diluted basis, this translates to earnings per share of 1.70 cents, compared to 1.85 cents in 1HFY20. With this, the group' s net asset value per ordinary share came in at 20.54 cents on Jun 30, up from 18.93 cents on Dec 30. Revenue for the first six months of the year grew 8.5% to $22.3 million on the back of strong performance of both its financial institution (FI) and non-financial (non-FI) institution data businesses. Revenue from the group' s FI data segment was up 13.4% to $9.7 million thanks to strong demand from the financial industry such as in new credit card applications and credit reviews. Similarly, revenue from its non-FI data segment was up 4.9% to $12.6 million. A key lift was from its global credit risk management solutions (+4.5% to $7.2 million) that was driven mainly by demand from increased compliance and risk management requirements from both local and global customers. Aside from this, the segment saw an increase in the sale of reports under the Singapore Commercial Credit Bureau (SCCB) and other bureaus (+1.8% to $3.7 million) as well as higher revenue from other non-ancillary non-FI data services (+14.2% to $1.7 million). In this time, the group' s employee benefits expenses were up by 8.7% to $5.6 million, due to an increase in headcount in the IT and data analytics function of its FI data business. Meanwhile depreciation and amortisation expenses were stable at $2.1 million. Other operating expenses were up by 5% to $4.78 million in 1HFY21. Such expenses from the FI data business was up 2.8% to $1.39 million due to increase in royalty expenses following the acquisition of a subsidiary as well as higher customer entertainment and administrative expenses. Other operating expenses from its non-FI data business was up 6% to $3.4 million on the back of higher IT security related expenses and foreign exchange losses. CBA' s share of joint ventures was up 17.1% to $0.53 million in 1HFY21. " Our share of results related to our Cambodia investment increased by $0.12 million, driven by increase in quantity of credit reports sold to bureau members due to the picking up of credit activities and the introduction of K-Score in the end of last year," the group explains in its results filing. Over in Myanmar, its share of losses was up $0.04 million following higher operating costs. As at June 30, CBA' s cash and cash equivalents stood at $50.6 million, up from $24.5 million in the year before. The group has declared an interim dividend of 1.7 cents per share &ndash which represents about 100% of its PATMI of $3.9 million. The maiden pay out exceeds the group' s dividend policy stated in its prospectus of recommending at least 90.0% of net profit after tax attributable to its shareholders for the financial years ending FY2021 and FY2022. Going forward, CBA says its " business model is defensive to business cycles and pandemics and despite Covid-19, our business continues to grow and perform well during this period" . It notes that travel restrictions could present some inconvenience as it looks to forge alliances and expand its business and footprint in the region. Still it expects positive contributions from it' s the commencement of its subsidiary' s operations at Moneylenders Credit Bureau. The subsidiary &ndash Credit Bureau Singapore - is now close to finalising agreements with the Digital Bank Licensees. As for its investments in Myanmar, the group says it is working closely with the relevant stakeholders and preparing Myanmar Credit Bureau to be fully operational before the end of FY2021. Shares in CBA closed down 2 cents or 1.52% at $1.30 on Aug 5, before its results announcement. |

|||||||

| Useful To Me Not Useful To Me | ||||||||