Latest Forum Topics /

Valuetronics

Last:1.13

+0.04

+0.04

|

|

|

Buoyant outlook

|

||||||

|

Caesar

Master |

13-Nov-2025 14:28

|

|||||

|

x 0

x 0 Alert Admin |

Nice. Extra cash for Christmas shopping ...

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

spursfan

Supreme |

13-Nov-2025 12:03

|

|||||

|

x 0

x 0 Alert Admin |

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

|

||||||

|

spursfan

Supreme |

12-Nov-2025 08:43

|

|||||

|

x 0

x 0 Alert Admin |

Valuetronics? improved profitability in 1H FY2026 reflects strategic focus on higher margin products - Net profit attributable to Owners of the Company up 2.7% to HK$93.0 million despite 3.0% dip in revenue to HK$836.6 million. -Gross profit margin up 2.0% points to 18.8%, lifting gross profit 8.6% yoy to HK$157.3 million. - Declares interim dividend of 4.0 Hong Kong cents per share and special interim dividend of 4.0 Hong Kong cents per share bringing total dividend for 1H FY2026 to 8.0 Hong Kong cents per share. https://links.sgx.com/1.0.0/corporate-announcements/WV3570S00XME12YX/866678_20251111-VHL-HY2026-Media%20Release.pdf |

|||||

| Useful To Me Not Useful To Me | ||||||

|

lifeisgood

Supreme |

17-Sep-2025 09:37

|

|||||

|

x 0

x 0 Alert Admin |

Just announced, apparently its new business joint venture Trio not doing so well, so downsizing and reducing its stake from 51% to 26.6%. New venture should probably change name to Quad... | |||||

| Useful To Me Not Useful To Me | ||||||

|

hotelgrand

Master |

18-Aug-2025 09:29

|

|||||

|

x 0

x 0 Alert Admin |

no trading today?? quarterly results?

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

|

||||||

|

stlimst

Master |

08-Aug-2025 11:33

|

|||||

|

x 0

x 0 Alert Admin |

Buy from short-sellers and those who contra players.

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

hotelgrand

Master |

08-Aug-2025 11:29

|

|||||

|

x 0

x 0 Alert Admin |

Ex D today | |||||

| Useful To Me Not Useful To Me | ||||||

|

hotelgrand

Master |

07-Aug-2025 10:59

|

|||||

|

x 0

x 0 Alert Admin |

81.5 cts done today 7th August | |||||

| Useful To Me Not Useful To Me | ||||||

|

|

||||||

|

hotelgrand

Master |

06-Aug-2025 09:34

|

|||||

|

x 0

x 0 Alert Admin |

Divudend payabke 22nd August..when ex now 80cts | |||||

| Useful To Me Not Useful To Me | ||||||

|

lifeisgood

Supreme |

21-Jul-2025 14:03

|

|||||

|

x 0

x 0 Alert Admin |

Any potential for HK listing for Valuetronics? |

|||||

| Useful To Me Not Useful To Me | ||||||

|

hotelgrand

Master |

17-Jul-2025 17:08

|

|||||

|

x 0

x 0 Alert Admin |

Hit.79 cents high for 2025..

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

skbeng

Member |

17-Jul-2025 02:50

|

|||||

|

x 0

x 0 Alert Admin |

Holding since 2010, average cost $0.15 after dividends, still not selling. See $1 then consider. | |||||

| Useful To Me Not Useful To Me | ||||||

|

|

||||||

|

Solubl

Member |

06-Jul-2025 17:08

|

|||||

|

x 0

x 0 Alert Admin |

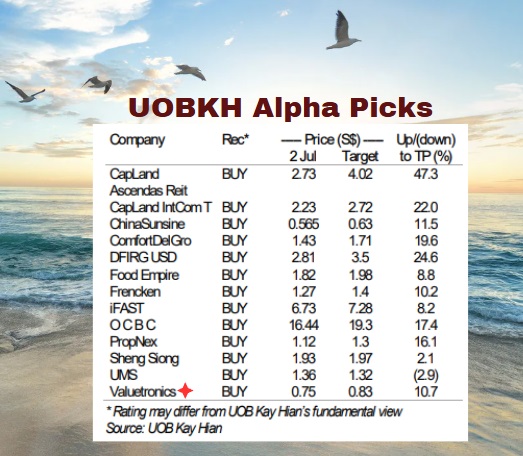

valuetronics is part of UOB KH alpha portfolio. Also a pick of DBS Research.  https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16226-this-company-is-classic-value-play-it-offers-consistent-dividends-robust-balance-sheet-margin-upside#google_vignette |

|||||

| Useful To Me Not Useful To Me | ||||||

|

Cadence88

Veteran |

27-Jun-2025 15:18

|

|||||

|

x 0

x 0 Alert Admin |

Probably due to the so-called US-China trade truce signing. | |||||

| Useful To Me Not Useful To Me | ||||||

|

hokpin

Supreme |

27-Jun-2025 15:04

|

|||||

|

x 0

x 0 Alert Admin |

No idea. Bro! Someone know what we don' t know!

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

Caesar

Master |

27-Jun-2025 14:02

|

|||||

|

x 0

x 0 Alert Admin |

Congrats, bro ... wonder why it is so strong today ... anyway, nice .... waiting happily for the coming dividends ...

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

Caesar

Master |

27-Jun-2025 13:54

|

|||||

|

x 0

x 0 Alert Admin |

Bro, fret not, as long as you have profits ... opportunity will come again ... any idea why it is so strong today?

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

hotelgrand

Master |

27-Jun-2025 13:10

|

|||||

|

x 0

x 0 Alert Admin |

73cts new high for 2025's..Ever hit $1.08 when 10 forv1 bonus previously

|

|||||

| Useful To Me Not Useful To Me | ||||||

|

hokpin

Supreme |

27-Jun-2025 10:04

|

|||||

|

x 0

x 1 Alert Admin |

Sold too much early...Regreting... | |||||

| Useful To Me Not Useful To Me | ||||||

|

spursfan

Supreme |

30-May-2025 16:08

|

|||||

|

x 0

x 0 Alert Admin |

dividend payment info https://links.sgx.com/1.0.0/corporate-announcements/E60C120QGORTUR7M/f65cdba8c25f7bb8bb25eafd4ef2728ac9a3f1ad24a6475b4cb2e2bc56712362 https://links.sgx.com/1.0.0/corporate-announcements/IIE93P684GOFV359/d51fd65f1f90b0838fccb5c29a91d688eb9883dab069e2f7f3d6169533b738d7 |

|||||

| Useful To Me Not Useful To Me | ||||||