| Latest Forum Topics / China Sunsine |

|

|

China sunsine

|

|||||

|

Joelton

Supreme |

02-May-2026 12:50

|

||||

|

x 0

x 0 Alert Admin |

China Sunsine reports 6% y-o-y increase in sales revenue for 1QFY2026

China Sunsine has reported sales revenue of RMB890 million for 1QFY2026 ended March 31, up 6% y-o-y, driven by higher sales volume.

For 1QFY2026, China Sunsine sold 60,916 tonnes of products, 15% higher y-o-y and hits another record high for its quarterly sales volume.

Gross profit margin declined by 2.7 percentage points to 21.4% in 1QFY2026, mainly due to lower average selling price (ASP). Net profit for the same period was at RMB69.5 million.

Although the company adjusted upwards its ASP due to higher raw materials, it was constrained by pre-agreed lower quarterly prices which accounted for approximately half of 1QFY2026 orders.

As a result, ASP declined 7% y-o-y to RMB14,511 per tonne, despite increasing by 4% on a q-o-q basis. China Sunsine expects an increase in its ASP in the next quarter due to the recent increase in raw materials prices.

Looking ahead, beyond market expansion and enhancing internal efficiency, China Sunsine aims to maintain its market leadership position and remains confident on its profitability and future growth.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Sgvale

Supreme |

06-Mar-2026 13:59

|

||||

|

x 0

x 0 Alert Admin |

Today looks good to recovery

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Sgvale

Supreme |

06-Mar-2026 11:30

|

||||

|

x 0

x 0 Alert Admin |

Bought at 0.775. Don't know when will return?

|

||||

| Useful To Me Not Useful To Me | |||||

|

Sgvale

Supreme |

06-Mar-2026 10:55

|

||||

|

x 0

x 0 Alert Admin |

Bought when call for TP 0.95. Keep for dividend now.

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

05-Mar-2026 15:17

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

See latest research report from UOBKH.

|

||||

Sgvale ( Date: 05-Mar-2026 15:00) Posted:

|

Supreme

x 0

Alert Admin

Supreme

x 0

Alert Admin

Establishment of dividend policy sparks re-rating for China Sunsine, UOBKH raises TP to 95 cents

For 9MFY2024, China Sunsine reported revenue 7% lower y-o-y at RMB2.4 billion and earnings 17% higher y-o-y of RMB330 million, which forms 70% and 76% of UOB KayHian analysts&rsquo full year forecast respectively.

&ldquo The revenue decline reflects softer ASPs amid heightened industry competition. Sales volumes remained resilient at 163,999 tonnes (+3% y-o-y), underscoring stable demand despite pricing pressure,&rdquo the team adds.

Mo and Cheong, in their report dated Nov 21, note that China Sunsine&rsquo s management introduced a formal dividend policy committing to a minimum 40% payout of core net profit for FY2025 and FY2026, paid semi-annually.

&ldquo This exceeds the group&rsquo s historical high payout of 36% in FY2024, signalling management&rsquo s strengthened confidence in earnings visibility. This is supported by its strong net cash position of RMB2.2 billion (approximately $410 million or 43 cents per share ) as at June 30,&rdquo write Mo and Cheong.

The team also highlighted that end-markets remain supportive, with China&rsquo s auto sales rising 13% y-o-y and new energy vehicle sales surging 35% y-o-y in 9MFY2025. Tyre production also grew modestly (+2% y-o-y).

&ldquo As China Sunsine supplies over 75% of the world&rsquo s top 75 tyre makers, this provides a solid foundation for firm demand across accelerators, insoluble sulphur and anti-oxidants,&rdquo Mo and Cheong add.

Both Mo and Cheong are positive on the company&rsquo s expansion programme as it remains on schedule, with key projects set to commence trial runs between end of 2025 and early 2026. Upon completion, total annual capacity will rise to 272,000 tonnes in 2026, supporting volume growth and enhancing operational efficiency.

The higher target price reflects China Sunsine&rsquo s strong balance sheet, improved dividend under the new 40% payout policy, and benefits from the upcoming capacity expansion.

Member

x 0

Alert Admin

Senior

x 0

Alert Admin

Senior

x 0

Alert Admin

Supreme

x 0

Alert Admin

Nice. Another high goes higher stock like HL Asia, Food Empire, OKP, Oiltek etc

Senior

x 0

Alert Admin

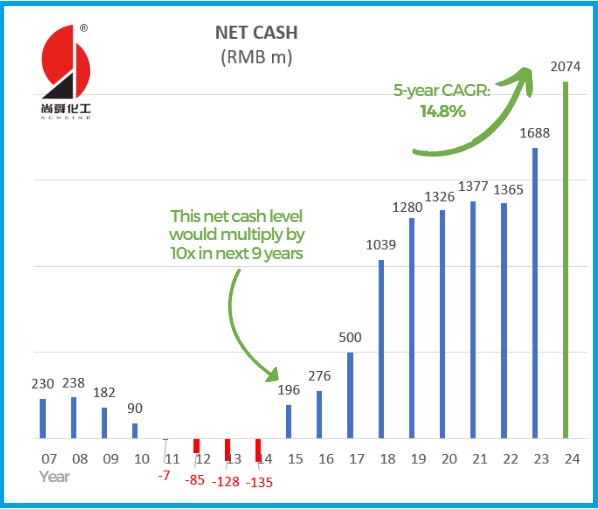

On 18-year journey Since IPO, One Company Grows A Cash Mountain. Stock Trades ... at 1X PE ex-cash!

... a long-time shareholder of China Sunsine Chemical analyses the growth of the company since its listing on the Singapore Exchange in 2007.

China Sunsine instead has demonstrated an enduring vigour.

If there' s one metric that reflects that, it is its cashpile which has risen steeply (chart below).

Article link: https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16060-on-18-year-journey-since-ipo-one-company-grows-a-cash-mountain-stock-trades-at-1x-pe-ex-cash

Supreme

x 0

Alert Admin

China Sunsine Chemical&rsquo s profit spread to remain firm in 4QFY2024, CGSI keeps &lsquo buy&rsquo

CGS International analysts Kenneth Tan and Ong Khang Chuen have kept &ldquo buy&rdquo on China Sunsine Chemical with a target price of 47 cents following the company&rsquo s 3QFY2024 ended September results release.

For its 3QFY2024, China Sunsine posted net profit of RMB93 million, up 43% y-o-y. This is largely in line with expectations, the analysts note. Revenue grew slightly by 1% y-o-y to RMB884 million as stronger average selling prices (ASPs) was slightly offset by weaker volumes.

While China Susine did not disclose its gross profit margin (GPM), the analysts estimate that it likely came in at 21%-22%.

Citing latest prices from chemical data provider Sci99, Tan and Ong note that rubber accelerator ASPs remained on a downtrend throughout October to November, down 15%-20% y-o-y.

To this end, the analysts believe that China Sunsine&rsquo s 4QFY2024 GPM could remain flat or decline slightly on a q-o-q basis, with the full year&rsquo s GPM coming in at around 23%.

The analysts also point out that China&rsquo s industrial tyre production grew well in 3QFY2024, rising 2% q-o-q and 10% y-o-y. With China Sunsine likely maintaining its flexible pricing strategy in FY2025, Tan and Ong think efforts to proactively defend and grow market share could weigh on meaningful GPM upside.

&ldquo Potential ramp-up in industry capacity in FY2025 could also be an impediment to margin expansion, in our view,&rdquo they add.

CGSI continues to like China Sunsine for its undemanding valuations at 1.5x 2025 ex-cash P/E, decent FY2025 yield of about 6% and increased focus on share buybacks.

Supreme

x 0

Alert Admin

China Sunsine Chemical Holdings

On May 14, China Sunsine Chemical Holdings : QES 0% independent director Koh Choon Kong purchased 50,000 shares at S$0.39 per share.

He maintains a 0.89 per cent deemed interest in the rubber chemicals enterprise.

His preceding acquisition was back in May 2023, with 20,000 shares bought at S$0.415 per share.

In a business update on May 3, China Sunsine Chemical Holdings reported an 8 per cent increase in product sales volume for Q1 2024 over Q1 2023.

This was despite a slight decrease in sales revenue due to a lower average selling price influenced by reduced raw material costs and a flexible pricing strategy.

The company&rsquo s gross profit margin improved by one percentage point, and net profit rose to 85 million yuan (S$15.8 million).

Concurrently, vehicle sales in China&rsquo s automotive industry grew 10.6 per cent, with new-energy vehicles accounting for 31.1 per cent of total sales, indicating a significant shift towards sustainable transportation.

Koh&rsquo s long-standing role within the company has evolved from that of non-executive director to independent director since 2009.

He has more than 20 years of experience in audit, accounting, corporate finance and business, and now on the management team of the largest independent power producer in Bangladesh, Summit Power International.

Koh also served as group chief financial officer in several SGX-listed corporations, and has worked in organisations ranging from Citicorp Investment Bank (Singapore) and EtonHouse International to ICH Capital and Price Waterhouse.

Supreme

x 0

Alert Admin

UOBKH lowers China Sunsine Chemical&rsquo s TP to 46 cents with lowered earnings expectations

UOB Kay Hian analysts Heidi Mo and John Cheong have kept their &ldquo buy&rdquo call on China Sunsine Chemical although they have lowered their target price to 46 cents from 57.5 previously.

The target price is pegged to a multiple of 6 times the company&rsquo s FY2024 P/E, which is its long-term average mean.

Referring to China Sunsine&rsquo s business update for the 3QFY2023 ended Sept 30, the analysts note that the lower quarterly revenue was due to lower average selling prices (ASPs) of rubber accelerators and the company&rsquo s newly-adopted flexible pricing strategy. This was partly mitigated by a record-high quarterly sales volume, which grew by 16.3% y-o-y to 56,114 tonnes.

For the 3QFY2023, China Sunsine&rsquo s revenue fell by 5% y-o-y to RMB875 million ($166.4 million). The ASP in the 3QFY2023 fell by some 18% y-o-y to RMB15,430 per tonne.

The company&rsquo s net profit fell by 49.2% y-o-y to RMB65 million for the 3QFY2023, bringing its 9MFY2023 net profit to RMB259.6 million, or 53% of the analysts&rsquo FY2023 estimate.

In their report dated Dec 14, Mo and Cheong see positives for the company including a potential near-term benefit from the higher ASPs of rubber accelerators, higher vehicle sales and continuous expansion projects undertaken, as well as the company maintaining its market leadership and strong balance sheet.

However, they have lowered their gross margin assumptions for FY2023 to FY2025 to 23% to 24% from 29% on account of price adjustments in the face of competitive pressures in the industry. As a result, their earnings estimates have also been lowered by 34%, 33% and 27% for the FY2023, FY2024 and FY2025 to RMB324 million, RMB388 million and RMB426 million respectively.

Veteran

x 0

Alert Admin

Elite

x 0

Alert Admin

old already

ash902 ( Date: 07-Sep-2018 07:14) Posted:

|

Veteran

x 0

Alert Admin

ash902 ( Date: 16-Aug-2018 10:19) Posted:

|

Veteran

x 0

Alert Admin

Supreme

x 0

Alert Admin