| Latest Forum Topics / HongkongLand USD Last:7.45 -- |

|

|

Hongkong Land USD

|

|||

|

JurongW

Elite |

03-Jun-2026 17:49

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

03-Jun-2026 17:47

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

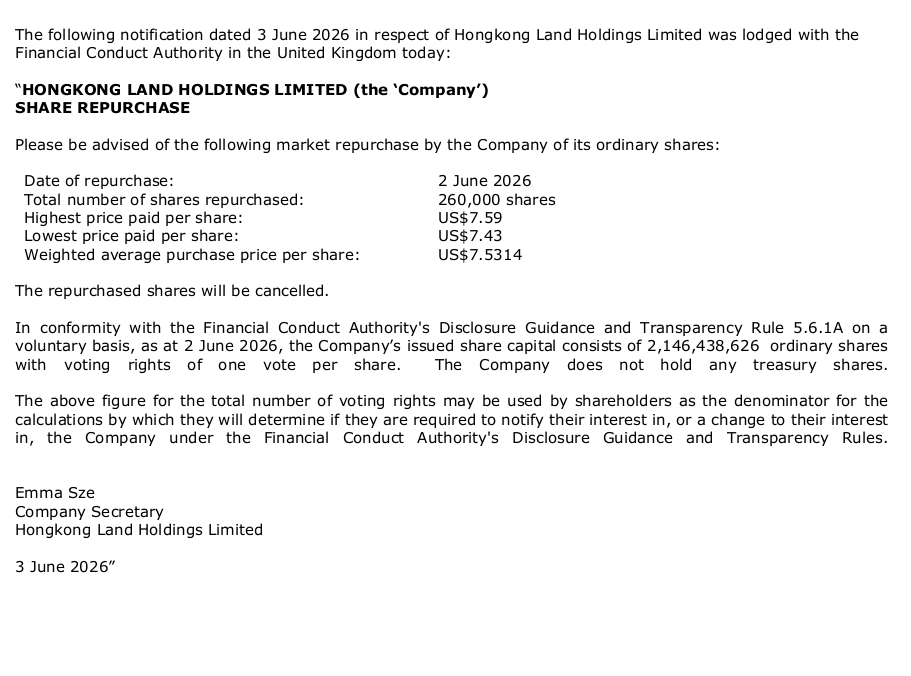

Key management personnel buy shares on 2 June https://links.sgx.com/1.0.0/corporate-announcements/UP3VLUO4YBHWEDJW/891268_2026-06-03_Purchase%20shares%20x3.pdf |

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

JurongW

Elite |

30-May-2026 15:58

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

30-May-2026 15:56

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

Price Targets by USB and JPM In a May 20 report, UBS points out that HKL 1QFY2026 operational update reported earnings rose 5% y-o-y, as lower net finance costs offset the loss of rental income following the disposal of MBFC Tower 3 and the formation of SCPREF. HKL also announced an upward revision to its FY2026 earnings guidance, reflecting improving sentiment in Hong Kong office leasing and proactive cost management. UBS calculates that HKL still has US$278 million of unutilised buyback capacity until mid-2027. It forecasts a 12-month target of US$10.96, based on a 15% discount to HKL estimated NAV per share. JPMorgan says the next catalysts for HKL are: further improvement in the Hong Kong office market capital recycling and more clarity on the investment in Suntec REIT, as well as leasing updates from Westbund Central. Share buybacks may also support the share price, the report adds. JPMorgan has a 12-month target of US$10.70, based on a 20% discount to its NAV estimate.

|

||

| Useful To Me Not Useful To Me | |||

|

Joelton

Supreme |

30-May-2026 13:38

|

||

|

x 0

x 0 Alert Admin |

Hongkong Land turns asset-lighter in growth push Hongkong Land (HKL), with investment properties last valued at US$34.6 billion ($44.2 billion) and a market cap of US$16.7 billion, is the largest listed developer on the Singapore Exchange. Within its portfolio, 53% of assets are in Hong Kong office, 13.5% in Hong Kong retail, 11.2% in Mainland China & Macau, 11.2% in property development, 9.2% in Singapore office and the rest in other assets. Since 2024, it has been headed by a Singaporean, Michael Smith, who was appointed CEO in April that same year. After HKL introduced a new strategy in October 2024, its share price has narrowed the discount to net asset value (NAV) by more than doubling to $8 as of May 25 from $3.89 as at Oct 29, 2024. In the same period, the price-to-NAV (P/NAV) has risen from 0.28 times on Oct 29, 2024 to 0.56 times as of May 25. Initially, the strategy involved divesting non-core assets, such as MCL Land, and other property development assets at or near book value, and using 20% of the proceeds to buy back shares at a discount to book value. The strategy also set new targets, including recycling up to US$10 billion of capital by 2035, with US$4 billion by the end of 2027, and doubling its profit before interest and tax (pbit) and dividends per share by 2035. In FY2023, pbit was US$844.6 million and dividend per share was 22 cents. To date, HKL has recycled further US$3.6 billion, or around 90% of the targeted US$4 billion by the end of 2027. On the asset management front, HKL set a target of US$100 billion in assets under management (AUM) by 2035, up from US$40 billion, to increase third-party capital to expand AUM and fee income. In February, HKL set up the Singapore Central Private Real Estate Fund (SCPREF) with AUM of $8 billion and Qatar Investment Agency and APG Asset Management as capital partners. Growing total shareholder returns Group CFO Craig Beattie has been with the Jardine Group for around 20 years, including two years at HKL. In a recent interview with The Edge Singapore, Beattie reveals that the targets in HKL&rsquo s new strategy were announced following what he describes as substantial research into which real estate companies had long-term market-leading returns and how they were achieved. &ldquo I had already been CFO for a couple of years at that point and I had a very strong sense as to what we needed to do to create value for shareholders. Michael kicked off a strategic review project, which I worked on closely with him and others,&rdquo Beattie recalls. The doubling of earnings and dividends was worked out mathematically. &ldquo As CFO, my role was to be able to articulate the types of TSR (total shareholder return) performance we needed. It was to model out the pathway to achieve that in terms of business growth,&rdquo he says. As with all good storytelling, investors need something easy to remember and simple to understand, given the complexity of any business strategy. &ldquo We spent a lot of time trying to understand and analyse what &lsquo good&rsquo looks like. We worked very hard to distil the stories. When you see the four targets, the doubling of pbit and dividends, the growth of the AUM and the recycling of capital, they were very deliberate they were not accidental targets,&rdquo Beattie explains. As he tells it, he and the HKL team analysed shareholder return performance to determine the TSR they wanted to achieve, then worked backwards from there. &ldquo This is where the role of the CFO comes in, because we had to model out if we want to hit these share price targets in the future,&rdquo Beattie adds. In 2021, HKL announced a US$500 million share buyback because Covid had negatively impacted the share price. &ldquo The board felt we were trading at a value way below our NAV per share. Tactically, we felt that investing US$500 million would create value over the longer term,&rdquo Beattie remembers. In a share buyback, the shares repurchased are cancelled, reducing the number of shares outstanding, thereby boosting earnings per share (EPS) and dividends per share (DPS). This time round, the strategy is different. Funding for share buybacks comes from 20% of capital recycling proceeds. The remaining 80% is earmarked for growth. &ldquo The number one driver of shareholder returns is earnings growth. The 80:20 allocation, between 80% to growth acquisitions and 20% to buybacks, was quite deliberate. The second driver is dividend growth, as most investors prefer dividends. The third driver is share buyback, but it tends to be more tactical and it&rsquo s also linked to what our share price is because we&rsquo re trying to close the gap between the value of our assets and the share price,&rdquo Beattie elaborates. Why now? In 2019, Ben Keswick took over as executive chairman of Jardine Matheson. By then, the landscape for investing in Asia across 30 years had changed in the aftermath of Covid. &ldquo Businesses, including family-controlled companies, needed to demonstrate the value that they add,&rdquo Beattie says. Ben and his cousin Adam were keen to demonstrate long-term value creation for investors, which includes the family. The value-creation campaign set off a chain reaction across the major parts of Jardines, with new executives appointed for HKL, Mandarin Oriental, DFI Retail and Jardine Matheson. Not solely asset-light According to Beattie, HKL&rsquo s strategy is not to be solely asset-light. &ldquo We want to continue to be an investor in real estate, we want to continue to be a developer, but we want to be an asset manager too. It&rsquo s more a natural evolution,&rdquo he adds. For instance, HKL has no plans to invest in logistics or data centres. &ldquo If we can replicate what we&rsquo ve achieved in Hong Kong and Singapore and take that to Shanghai or Sydney or Seoul, then I think that&rsquo s a competitive advantage,&rdquo Beattie points out. HKL&rsquo s choicest investment properties are in Marina Bay here and the Central District in Hong Kong. In December 2025, HKL divested Marina Bay Financial Centre (MBFC) Tower 3 to Keppel REIT for US$1.1 billion, or approximately $1.5 billion, at a 2% premium to its valuation as at June 30, 2025. Following the divestment, HKL launched SCREF on Feb 3, using its one-third stake in MBFC Towers 1 and 2 and One Raffles Quay, and 100% of One Raffles Link, as seed capital. A fourth property, Asia Square Tower 1, which QIA owned, was also placed in SCPREF, along with QIA and APG as capital partners. The initial fund size is $8.2 billion, with plans to grow it to $15 billion in the next five years. &ldquo The fund has a very particular focus. It&rsquo s Singapore-only and the assets must be located in Marina Bay or on Orchard Road. The fund is focused on prime commercial, office, retail or hospitality assets. It&rsquo s quite a particular narrow focus, which we deliberately want because that is what HKL knows best and we think there&rsquo s demand for a fund vehicle of this type,&rdquo Beattie emphasises. &ldquo Our focus is on the best assets. We&rsquo ve got the benefit of time to build a position. We&rsquo re not looking to do it all within the next six months. The growth ambition is over the next five years.&rdquo Landmark makeover HKL&rsquo s ultra-premium positioning is unique. For instance, in 2024, when Hong Kong&rsquo s retail sector was in a challenging period, HKL announced a US$1 billion makeover of Landmark, with US$400 million from HKL and US$600 million from its luxury tenant base. The leading luxury brands co-invested to create flagship stores, with some of them doubling in size with an eye to Hong Kong&rsquo s pool of ultra-high-net-worth individuals as customers. According to Beattie, 85% of Landmark&rsquo s sales are to local Hong Kong people. In its 1QFY2026 business update, HKL said Landmark&rsquo s retail portfolio&rsquo s rental contributions increased slightly compared with 1QFY2025 despite over 30% of lettable space under renovation as part of the ongoing Tomorrow&rsquo s Central transformation. &ldquo This performance underscores the resilience of ultra-high-net-worth spending and Landmark&rsquo s position as Asia&rsquo s premier luxury retail destination. Tenant sales and top-tier customer spend were both higher compared with the same period last year. Average effective rents were higher than in the first quarter of 2025 as new leases recently commenced for several flagship Maison stores,&rdquo the report added. Based on HKL&rsquo s business updates, the results of Landmark&rsquo s makeover are tracking ahead of expectations. &ldquo It&rsquo s a complex project which will take three years to complete. We&rsquo re doing it in phases. Sales, despite all the temporary disruption from the renovation works, are up. We are expecting sales in the Landmark mall to increase by well over 25% upon completion,&rdquo Beattie emphasises, adding: &ldquo We have demonstrated time and time again that we can execute on these ultra premium, integrated commercial properties.&rdquo Most of HKL&rsquo s Central portfolio is on 999-year leases and effectively freehold. &ldquo We have a competitive advantage by having such long tenure in our buildings. All of our buildings are in Central. We continue to believe that there&rsquo s a real benefit from being in the best real estate in any market, particularly given the flight quality trends that are prevalent around the world at the moment,&rdquo he adds. The Hong Kong office market has been in quite a difficult position over the past five years, but it appears to be turning the corner amid capital market activity. Property consultants are expecting rents to grow by 5%&ndash 10% this year. Shanghai assets In terms of gross floor area and net lettable area, China is by far HKL&rsquo s largest market. In Shanghai, HKL is building a mixed-use project spanning 18 million sq ft on the Huangpu River, called Westbund Central. Hong Kong Central is 4.6 million sq ft in comparison. The capital value of Westbund Central when completed is likely to be around US$8.5 billion. &ldquo In terms of potential, China is the number one growth market for Hongkong Land, because a lot of new projects are about to open, which will generate additional income,&rdquo Beattie notes. However, he acknowledges that the company&rsquo s The Ring series in cities such as Chengdu and Chongqing does not fit the description of ultra-high-premium investment properties. &ldquo It is the intention, over time, to recycle capital out of those projects,&rdquo Beattie says. Another investment that appears out of character is the purchase of a 10.8% stake in Suntec REIT for $541 million. &ldquo The Suntec block from ESR was a unique opportunity to acquire immediate, additional exposure to Singapore office assets through the REIT and we felt that the shares were undervalued relative to the underlying assets. We were aware that the manager was changing, with Gordon Tang coming in,&rdquo Beattie says. A strategic review of Suntec REIT&rsquo s portfolio is underway. HKL is not a sponsor of any REIT, but Beattie acknowledges that it may create a China REIT at some point. On geographical expansion, HKL has hired representatives in Sydney and Seoul who have been working with the group for more than six months, Beattie reveals. &ldquo We are working on market entry strategies, which is something that we are discussing with the HKL board. One of the appeals of entering these new markets is that asset yields are higher. The main takeaway is that HKL wants scale in these markets, so buying a single building by itself is not particularly appealing,&rdquo Beattie says. In a May 20 report, UBS points out that HKL&rsquo s 1QFY2026 operational update reported earnings rose 5% y-o-y, as lower net finance costs offset the loss of rental income following the disposal of MBFC Tower 3 and the formation of SCPREF. HKL also announced an upward revision to its FY2026 earnings guidance, reflecting improving sentiment in Hong Kong office leasing and proactive cost management. UBS calculates that HKL still has US$278 million of unutilised buyback capacity until mid-2027. It forecasts a 12-month target of US$10.96, based on a 15% discount to HKL&rsquo s estimated NAV per share. JPMorgan says the next catalysts for HKL are: further improvement in the Hong Kong office market capital recycling and more clarity on the investment in Suntec REIT, as well as leasing updates from Westbund Central. Share buybacks may also support the share price, the report adds. JPMorgan has a 12-month target of US$10.70, based on a 20% discount to its NAV estimate. Smith, Beattie and the new team at HKL have a long-term perspective compared to the shorter-term outlooks of analysts. &ldquo Hongkong Land has been in business for 137 years. By having a 10-year strategy and a 10-year goal was quite deliberate, because fundamentally, we are looking to create value over the long term,&rdquo Beattie concludes. |

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

JurongW

Elite |

22-May-2026 17:55

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

21-May-2026 18:10

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

21-May-2026 00:07

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

FY16 - 19 cents FY17 - 20 cents FY18 to FY23 - 22 cents FY24 - 23 cents FY25 - 25 cents Forecast FY26 - 27 cents. Full-year dividends expect to reach at least USD0.44 cents by 2035

|

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

JurongW

Elite |

20-May-2026 23:47

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

Recap - HKL Strategy Update announced on 29 Oct 2024 https://links.sgx.com/1.0.0/corporate-announcements/1JNZPJUTRWNWS53L/823339_HKLH1029.pdf |

||

| Useful To Me Not Useful To Me | |||

|

YewTee

Member |

20-May-2026 23:27

|

||

|

x 0

x 0 Alert Admin |

sbb....going private? | ||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

20-May-2026 17:53

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

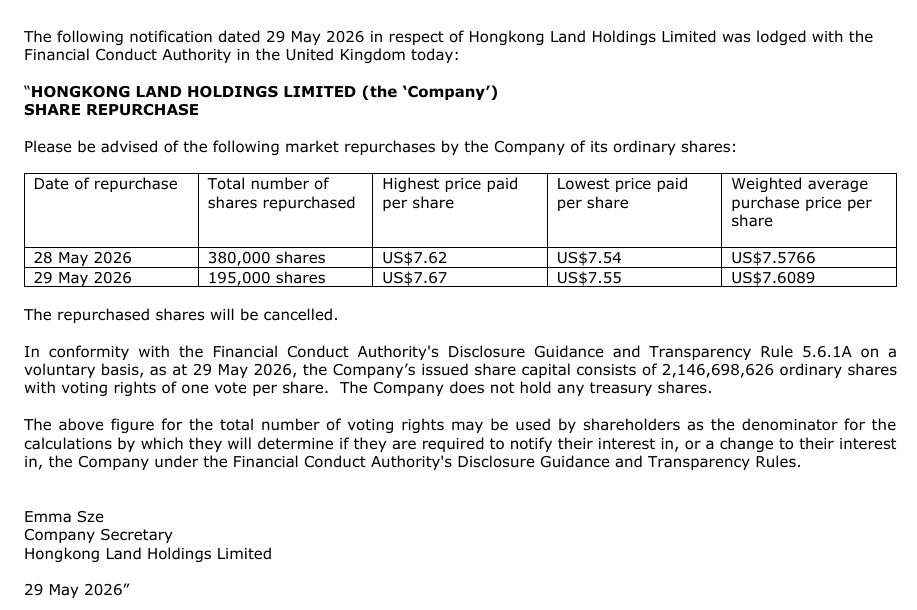

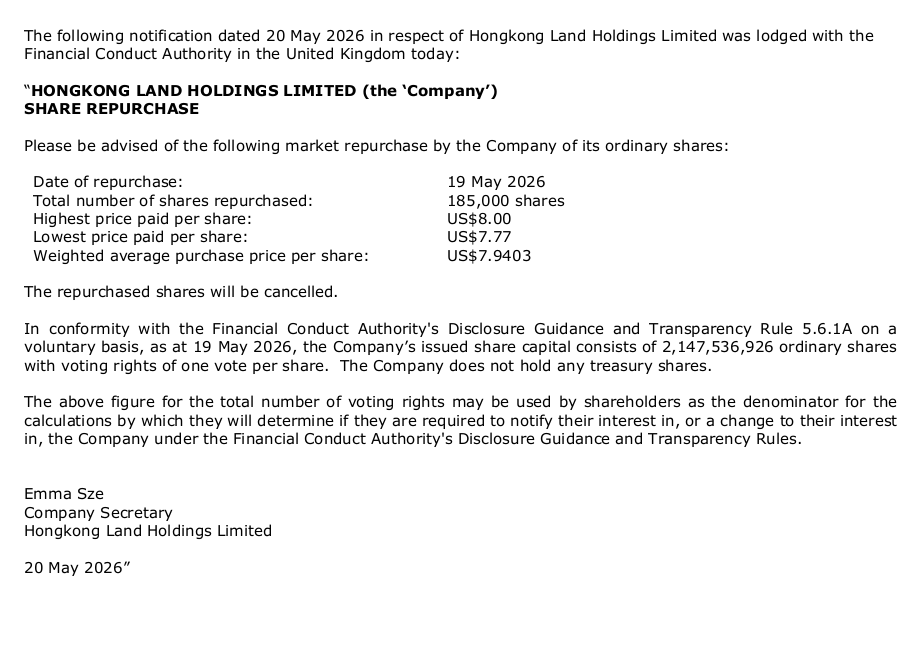

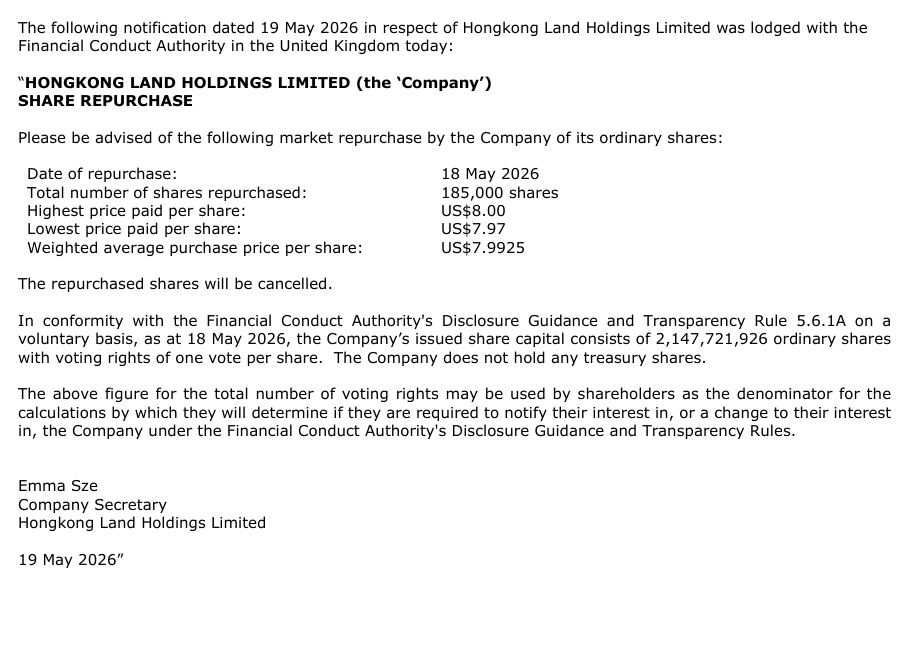

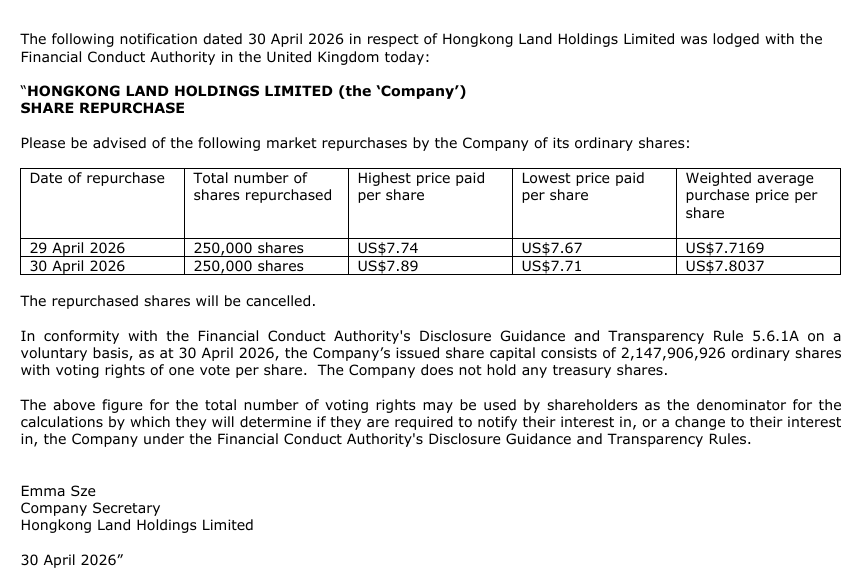

Extracted from Q1 update Since the announcement of the first tranche of the share buyback programme in April 2025, the Group has invested US$372 million in share buybacks and reduced shares in issuance by 2.7%. Approximately US$278 million of capacity remains to be invested through mid 2027.

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

20-May-2026 17:51

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

JurongW

Elite |

19-May-2026 19:49

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

1st Quarter update https://links.sgx.com/1.0.0/corporate-announcements/LYKCZJTGYUIITX6G/889429_HKLH0519%20SGX.pdf |

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

19-May-2026 19:20

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

Joelton

Supreme |

08-May-2026 10:24

|

||

|

x 0

x 0 Alert Admin |

Hongkong Land shares up 3.6% after report of multibillion-dollar Marina One bid The high-rise complex&rsquo s owner M+S has reportedly priced the asset at about S$5.7 billion [SINGAPORE] Shares of Hongkong Land : H78 +4.52%rose 3.6 per cent on Thursday (May 7), after a Bloomberg report that it and CapitaLand were among possible bidders for the Marina One high-rise complex. The counter rose to as high as US$8.26 as at 10.14 am, adding US$0.29, with more than one million shares changing hands. Marina One owner M+S, a joint venture between Temasek and Malaysian sovereign wealth fund Khazanah Nasional, has priced the asset at about S$5.7 billion, according to the Bloomberg report. The Business Times reported in January that Khazanah and Temasek were considering a sale at S$5 billion to S$6 billion. Marina One includes 1.88 million sq ft of office space as well as 140,000 sq ft of retail space. There are also apartments. Deliberations around Marina One are still at an early stage and may not result in a transaction. In March, Hongkong Land said it was ready to increase new investments after recycling US$3.6 billion of capital to boost earnings and shareholder returns. Speaking to BT, the property group&rsquo s chief financial officer Craig Beattie said it had ample balance-sheet headroom for new investments after recycling 90 per cent of its US$4 billion target and cutting net debt by 30 per cent. He added that Hongkong Land was &ldquo very positive&rdquo on Singapore and was looking to expand through its private fund or by pursuing development opportunities with a particular focus on &ldquo prime Central Business District (assets) in Singapore&rdquo . DBS in March set a US$10.17 target price for the property group. It stated that its share buyback programme and continued capital recycling was expected to provide near-term support to the share price. Hongkong Land has increased its share buyback programme by US$300 million to a total of US$650 million. DBS also noted that the development of a fund management platform could support a higher valuation over time. This followed Citi in February raising its target price for the stock from US$7.15 to US$9.75, in anticipation of Hongkong Land launching an S$8.2 billion Singapore private fund. The fund is focused on managing prime commercial property assets in the Republic. Hongkong Land seeded the Singapore Central Private Real Estate Fund with its interests in Marina Bay Financial Centre Towers 1 and 2, One Raffles Quay, One Raffles Link and Marina Bay Link Mall. Citi also said the fund was expected to bring in US$25 million to US$30 million in initial profit. However, Morningstar maintained a fair value estimate of US$7.40, believing that the then share price of US$8.67 was &ldquo overvalued&rdquo . It cited the 0.64 price-to-book ratio being above the 10-year historical average of 0.37. |

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

07-May-2026 17:39

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

Updated chart as of 7 May, 5pm Avg price target of USD10.21 based on price forecast of 10 analyst with min estimate of $9 to maximum of $11.

|

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

07-May-2026 14:04

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

cmengchan

Senior |

07-May-2026 10:52

|

||

|

x 0

x 0 Alert Admin |

Singapore&rsquo s Marina One office complex said to attract CapitaLand, Hongkong Landhttps://www.theedgesingapore.com/news/singapore-news/singapores-marina-one-office-complex-said-attract-capitaland-hongkong-land(May 5): CapitaLand Group Pte Ltd and Hongkong Land Holdings Ltd are among possible bidders for the Marina One high-rise complex in Singapore&rsquo s central business district, according to people familiar with the matter. Marina One is owned by M+S Pte Ltd, a joint venture of Malaysian sovereign wealth fund Khazanah Nasional Bhd and Singapore state investor Temasek Holdings Pte Ltd, who are seeking around $5.7 billion (US$4.5 billion) for the asset, some of the people said, asking not to be identified because the information is private. The high price target has been an obstacle to a sale of Marina One, which could also attract other suitors, possibly in a consortium, some of the people said. The Business Times reported in January that Khazanah and Temasek were considering a sale at $5 billion to $6 billion. Marina One includes 1.88 million square feet (175,000 square metres) of office space as well as 140,000 square feet of retail space, and there are also apartments in the complex. Deliberations around Marina One are still at an early stage and might not result in a transaction, the people said. Temasek declined to comment. Representatives for CapitaLand, which is owned by Temasek, and Hongkong Land didn&rsquo t respond to requests for comment. Khazanah and M+S also didn&rsquo t respond to requests for comment. Hongkong Land set up its Singapore Central Private Real Estate Fund this year to focus on high-end commercial property in the city-state. It already has assets in Asia Square and Marina Bay Financial Centre, as well as One Raffles Quay and One Raffles Link. Backers include Dutch pension fund APG Groep NV and the Qatar Investment Authority. CapitaLand has a private developer arm and listed asset manager with stakes in real estate investment trusts and private funds. |

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

05-May-2026 19:59

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

Purchase of shares at USD7.9287 by 3 key management staff on 4 May. https://links.sgx.com/1.0.0/corporate-announcements/1LRP7FL0VPKV8SJZ/887609_2026-05-04_Purchase%20shares.pdf |

||

| Useful To Me Not Useful To Me | |||

|

JurongW

Elite |

30-Apr-2026 18:54

Yells: "Earnings give weight, Chart give wings" |

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||