| Latest Forum Topics / Zhongxin Fruit Last:0.033 -- |

|

|

0005hk

|

|||||

|

piscesmonkey

Supreme |

29-Jul-2025 16:43

|

||||

|

x 0

x 0 Alert Admin |

Hmm maybe later zhongxin report out later suddenly got people buy up 500lots

|

||||

| Useful To Me Not Useful To Me | |||||

|

Kilatkilat

Veteran |

29-Jul-2025 16:21

|

||||

|

x 0

x 0 Alert Admin |

Yes. Switched from Zixin to here. Apples are better than potatoes

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

piscesmonkey

Supreme |

29-Jul-2025 16:19

|

||||

|

x 0

x 0 Alert Admin |

Buyer coming to push up 50?

|

||||

| Useful To Me Not Useful To Me | |||||

|

piscesmonkey

Supreme |

29-Jul-2025 11:08

|

||||

|

x 0

x 0 Alert Admin |

Still waiting for annoucement😁

|

||||

| Useful To Me Not Useful To Me | |||||

|

piscesmonkey

Supreme |

28-Jul-2025 13:04

|

||||

|

x 0

x 0 Alert Admin |

FY result out on 22aug. so Profit Guidance should be soon annouce. TP 70 liao | ||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Kilatkilat

Veteran |

03-Jul-2025 08:01

|

||||

|

x 0

x 0 Alert Admin |

My fund all stuck at Zicxin. ZHONGXIN IS A VERY VERY GOOD STOCK.

|

||||

| Useful To Me Not Useful To Me | |||||

|

TraderBen

Supreme |

03-Jul-2025 05:41

|

||||

|

x 0

x 0 Alert Admin |

I thought u staying at sweet potato bro?

|

||||

| Useful To Me Not Useful To Me | |||||

|

Kilatkilat

Veteran |

02-Jul-2025 12:52

|

||||

|

x 0

x 0 Alert Admin |

Agreed. Appke juice is selling like hot cake. In such hot summer, fruit juice is juicy. A very very good opportunity to break 40 and move towards 50!!

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Newbie85

Veteran |

02-Jul-2025 10:49

|

||||

|

x 0

x 0 Alert Admin |

Fruits counter very hot in China market now... https://www.businessinsider.com/china-economy-consumer-spending-if-coconut-water-beverage-ifbh-ipo-2025-6 |

||||

| Useful To Me Not Useful To Me | |||||

|

tofudidi

Supreme |

28-May-2025 09:36

|

||||

|

x 0

x 0 Alert Admin |

summer season. fruit and juice going up. may break 40

|

||||

| Useful To Me Not Useful To Me | |||||

|

wooncs8870

Veteran |

22-May-2025 08:54

|

||||

|

x 0

x 0 Alert Admin |

Zhongxin Fruit and Juice Ltd (SGX:5EG) is a small-cap company listed on the Singapore Exchange, primarily engaged in the production and sale of fruit and vegetable juice concentrates and beverages, mainly in the People' s Republic of China.SG Investors+3Simply Wall St+3GuruFocus+3 📊 Current Stock Performance

|

||||

| Useful To Me Not Useful To Me | |||||

|

Newbie85

Veteran |

09-Mar-2025 09:43

|

||||

|

x 0

x 1 Alert Admin |

Gave my insight on previous 2 threads. bought Yoma at 74 and sold near 100. bought yzj and sold 10 pips higher. Looking to buy some of Zhongxin below 30. |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Joelton

Supreme |

12-Feb-2025 12:28

|

||||

|

x 0

x 0 Alert Admin |

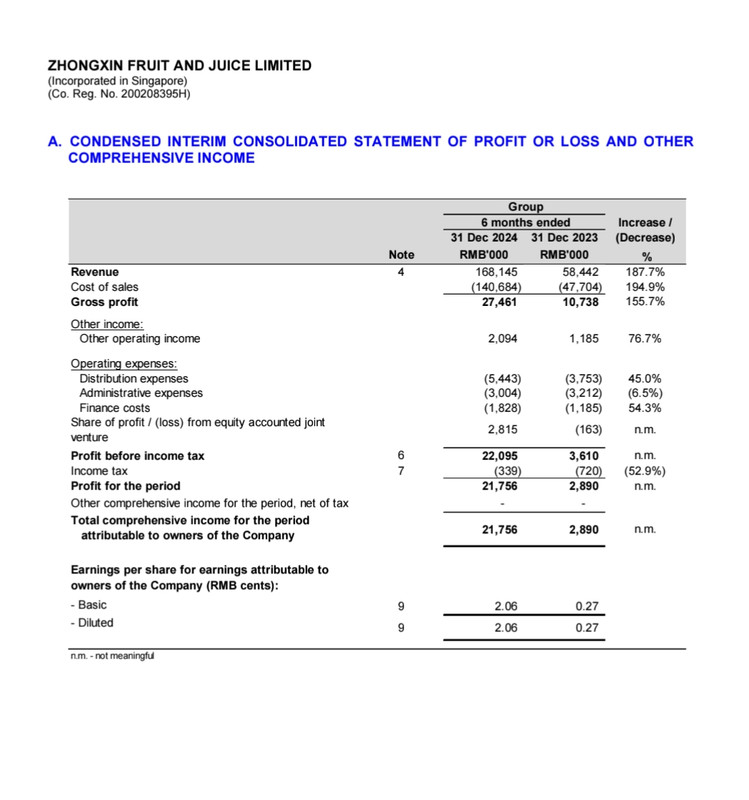

Zhongxin Fruits reports earnings surge of RMB21.76 mil, as customers look to increase inventory holdings

Zhongxin Fruits has reported earnings of RMB21.76 million ($4.04 million) for the 1HFY2025 ended Dec 31, 2024, a surge in earnings from the same period a year before which saw earnings of RMB2.9 million.

For the reporting period, earnings per share grew to RMB2.06, up from RMB0.27 from the same period a year ago.

The company recorded a 187.7% y-o-y increase in revenue for the 1HFY2025 to RMB168.14 million, from RMB58.44 million a year ago. Meanwhile, gross profit grew 155.7% y-o-y to RMB27.46 million in the 1HFY2025.

However, the group saw a decrease in gross profit margin from 18.4% in 1HFY2024 to 16.3% in 1HFY2025, mainly due to lower average selling prices of the concentrated fruit juices and fructose.

The group says that the fruit juice industry is cyclical in nature, and the harvest season of the group&rsquo s raw materials such as apples and pears is during the first half of its financial year. The group&rsquo s subsidiary Yuncheng Zhongxin Fruit & Juice Company generally produces fruit juice concentrate during this period for this annual supply.

The increase in revenue for the group is due to the substantial increase in purchasing activity from the end customers which are multinational F& B corporations in overseas markets such as the US. Zhongxin says that these customers may be looking to increase their inventory holding levels to maintain a stable supply chain.

Profit from Zhongxin&rsquo s equity-accounted joint venture, Linyi SDIC Zhonglu Fruit Juice of RMB2.8 million compared to the loss of RMB163,000 in the same period a year ago is due to higher sales volume from increased customer demand.

Cash and cash equivalents decreased by about RMB30.1 million. Net cash used in operating activities of RMB97.6 million in 1HFY2025 was mainly due to the positive cash flows before working capital changes and the changes in working capital outflow largely from the increase in notes receivables and receivable from immediate holding company, and offset by the decrease in inventories.

Current assets increased to RMB271.1 million as at Dec 31, 2024 compared to RMB181.3 million as at Jun 30, 2024 due to trade receivables and notes receivables from its subsidiaries.

In its outlook, Zhongxin said that while its significant growth in revenue and profitability in 1HY2025 could be attributable to end customers looking to increase its inventory levels, the group is cognisant that there is significant uncertainty as to whether this performance can be sustained in the next reporting period.

Zhongxin says that it will continue to face challenges which include fluctuating market demand, trade tensions, market competition as well as unpredictable climate change that adversely affects the harvesting conditions and causes reduction in the supply of quality raw materials and drives volatility of raw material prices.

The ability to procure sufficient raw materials during the harvesting seasons will impact the group&rsquo s ability to maximise the utilisation of the production capacity for economies of scale and cost competitiveness of the products produced by the group.

|

||||

| Useful To Me Not Useful To Me | |||||

|

eric998

Supreme |

12-Feb-2025 11:07

|

||||

|

x 0

x 0 Alert Admin |

Can short?

|

||||

| Useful To Me Not Useful To Me | |||||

|

piscesmonkey

Supreme |

12-Feb-2025 08:50

|

||||

|

x 0

x 0 Alert Admin |

May get lower? Up too much before result. Means sell on result?

|

||||

| Useful To Me Not Useful To Me | |||||

|

Johnsnow

Elite |

11-Feb-2025 19:32

|

||||

|

x 0

x 0 Alert Admin |

Wasted 50 did not get | ||||

| Useful To Me Not Useful To Me | |||||

|

Everyday

Elite |

11-Feb-2025 19:18

|

||||

|

x 0

x 0 Alert Admin |

Significant Net profit increase from 2.8m( 6mths ending Dec 23) to 21.7m( 6mths ending Dec 24). See how market will react tmr |

||||

| Useful To Me Not Useful To Me | |||||

|

Everyday

Elite |

11-Feb-2025 17:49

|

||||

|

x 0

x 0 Alert Admin |

Good news come early!

|

||||

| Useful To Me Not Useful To Me | |||||

|

sklong138

Elite |

11-Feb-2025 17:30

|

||||

|

x 0

x 0 Alert Admin |

|

||||

| Useful To Me Not Useful To Me | |||||

|

tofudidi

Supreme |

11-Feb-2025 16:49

|

||||

|

x 0

x 0 Alert Admin |

Sell or news or gap up news ? | ||||

| Useful To Me Not Useful To Me | |||||