Latest Forum Topics /

HongkongLand USD

Last:7.4

-0.05

-0.05

|

|

|

Hongkong Land USD

|

|||||

|

JurongW

Elite |

29-Apr-2026 02:04

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

27-Apr-2026 18:35

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

JurongW

Elite |

24-Apr-2026 18:13

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

23-Apr-2026 18:00

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

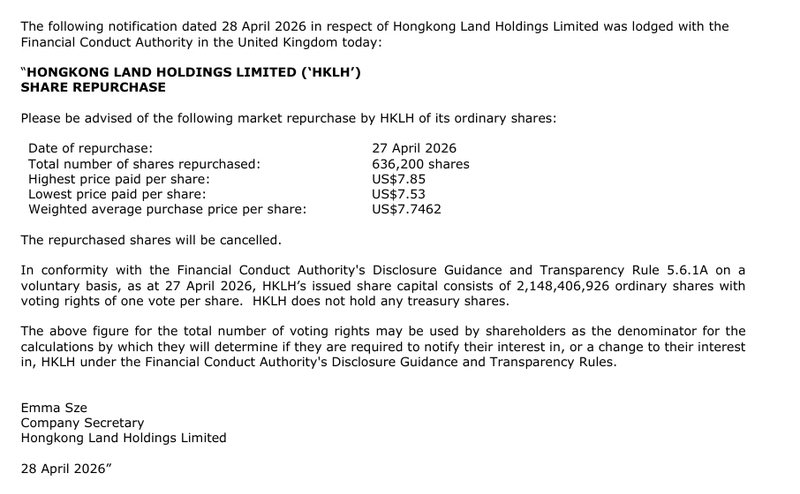

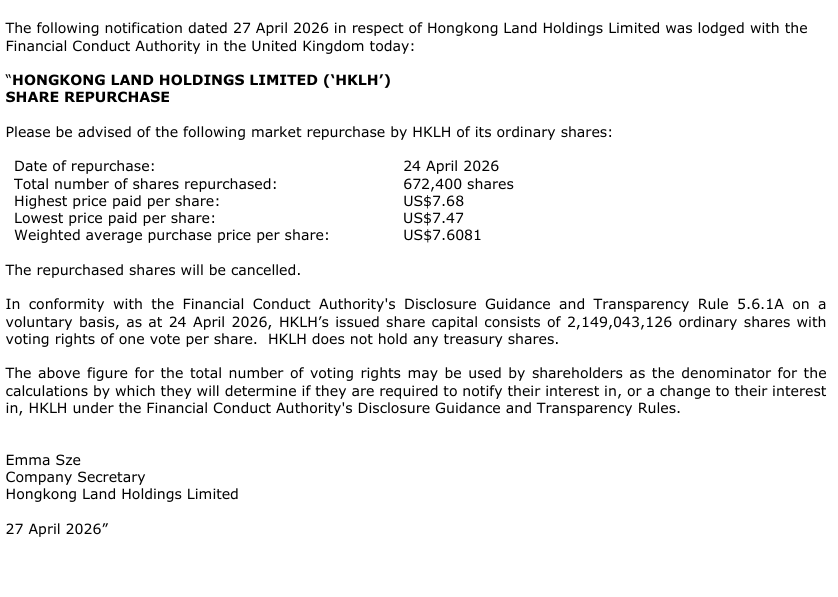

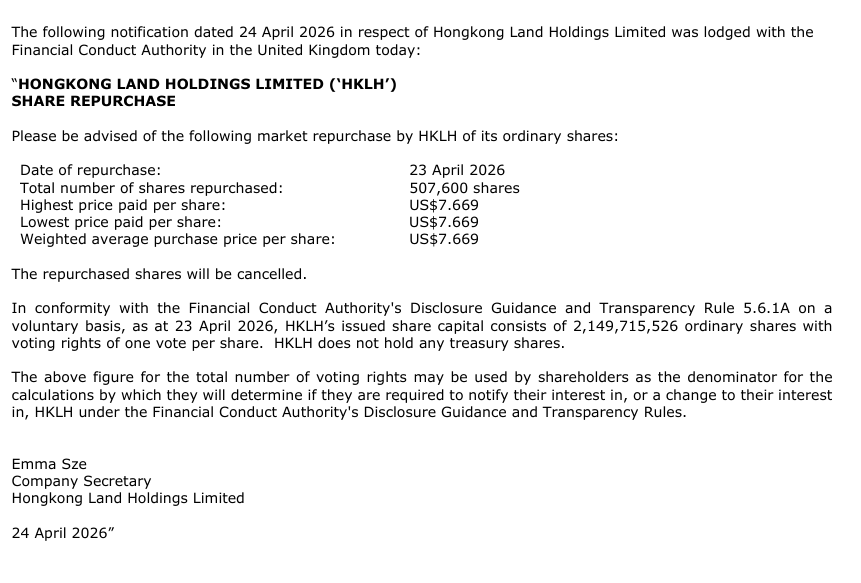

HK Land finally resumed SBB after taking a short break. 350,000 shares bought at average price of USD7.8994. https://links.sgx.com/1.0.0/corporate-announcements/HOJO6MYXV2LMT7NG/885316_2026-04-22%20Share%20Repurchase.pdf |

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

08-Apr-2026 18:46

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

Key management team bought shares of HongKong Land on 2 April. Details as follows: https://links.sgx.com/1.0.0/corporate-announcements/BS0OR8J9R5V6XWML/882578_0402b-SGXNET.pdf |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

JurongW

Elite |

20-Mar-2026 20:19

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

DBS Research

News alert: Strategic Investment in Suntec REIT

Investment in Suntec REIT Hongkong Land has acquired a 10.8% stake in Suntec Real Estate Investment Trust (Suntec REIT) from ESR Group for SGD541m (USD422m), at SGD1.70 per unit on 19 March 2026. The purchase price represents a 21.4% premium to the closing price on 18 March 2026, but a 16% discount to the REIT&rsquo s net asset value (NAV) as of December 2025. Suntec REIT owns a portfolio of strategically located commercial assets in Singapore, including Suntec City, as well as one-third interests in Marina Bay Financial Centre (Towers 1 & 2) and One Raffles Quay, which together account for c.75% of its portfolio valuation. The remainder of its assets are located in Australia and the United Kingdom. This acquisition aligns with Hongkong Land&rsquo s strategy of redeploying recycled capital into prime, income-generating commercial assets, with Singapore remaining its core market. Multiple benefits derived from the investment Suntec REIT offers an estimated distribution yield of 4.4% for FY26, making the investment immediately earnings accretive. In addition, the REIT manager, under the Tang Organization, has indicated plans to conduct a strategic review of its portfolio. Any value-unlocking initiatives arising from this review could support unit price appreciation and generate potential capital gains for Hongkong Land. Furthermore, Suntec REIT co-owns Marina Bay Financial Centre (Towers 1 & 2) and One Raffles Quay with the newly established Singapore Central Private Real Estate Fund (SCPREF), which is majority-owned and managed by Hongkong Land. This presents potential opportunities for collaboration in the future. Hongkong Land is trading at a 29% discount to our assessed current NAV. We remain constructive on the company&rsquo s evolving corporate strategy to enhance returns. Ongoing share buybacks should provide near-term price support. We maintain our BUY rating with a target price of USD10.17. |

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

20-Mar-2026 10:11

|

||||

|

x 0

x 0 Alert Admin |

Hongkong Land acquires 10.8% stake in Suntec Reit for S$541 million

It says the move aligns with its &lsquo positive outlook and conviction in Singapore&rsquo s prime commercial property market&rsquo

[SINGAPORE] Property developer Hongkong Land : H78 -4.17% has acquired a 10.8 per cent stake in Suntec Real Estate Investment Trust : T82U +4.29% (Reit) for S$541 million in its drive to grow its presence in Singapore&rsquo s prime commercial sector.

In a statement on Thursday (Mar 19), Hongkong Land said the acquisition will enable the group to deploy recently recycled capital into prime, income-producing commercial assets in the city-state.

&ldquo This aligns with the company&rsquo s positive outlook and conviction in Singapore&rsquo s prime commercial property market,&rdquo it said. &ldquo The yield derived from the company&rsquo s stake in Suntec Reit will contribute to the diversification of Hongkong Land&rsquo s earnings profile.&rdquo

In a bourse filing the same evening, Hongkong Land said it had initially entered a sale-and-purchase agreement to acquire 145.8 million units in Suntec Reit. This represented a 4.9 per cent interest in the trust.

The company, which later eyed the acquisition of more units, amended the agreement to acquire just under 318 million units of Suntec Reit instead.

Its wholly owned subsidiary ESR Real Estate Investors has been nominated to hold the units once the acquisition is completed.

Hongkong Land said its investment in Suntec Reit was made at a discount to the trust&rsquo s net asset value of S$2.03 a unit as at Dec 31, 2025.

&ldquo The company recognises Suntec Reit&rsquo s strategic potential to unlock value across its portfolio and (its) commitment to driving sustainable long-term growth for all unitholders,&rdquo it added.

The move follows the announcement of a comprehensive strategic review of Suntec Reit&rsquo s portfolio by its new sponsor, Tang Organization. The review was carried out to strengthen the performance of the portfolio and to enhance capital efficiency, while also exploring &ldquo disciplined approaches to asset optimisation and recycling&rdquo .

Tang Organization said these would support higher distributions in the coming years, and balance the Reit&rsquo s capital management needs and long-term sustainability.

Assets under Suntec Reit&rsquo s portfolio include a 33.3 per cent interest in Marina Bay Financial Centre Towers 1 and 2, and One Raffles Quay &ndash the same assets that Hongkong Land&rsquo s new private fund, Singapore Central Private Real Estate Fund, holds a 33.3 per cent interest.

In an interview with The Business Times in early March, Hongkong Land chief financial officer Craig Beattie said that having recycled 90 per cent of its US$4 billion target and cut net debt by 30 per cent, the group now has ample balance-sheet headroom for new investments.

Last September, it sold its Singapore and Malaysian property arm MCL Land for S$738.7 million in cash. Most of the proceeds went into building a &ldquo war chest for future endeavours&rdquo .

|

||||

| Useful To Me Not Useful To Me | |||||

|

cmengchan

Senior |

20-Mar-2026 10:09

|

||||

|

x 0

x 0 Alert Admin |

https://www.businesstimes.com.sg/companies-markets/hongkong-land-acquires-10-8-stake-suntec-reit-s541-millionHongkong Land acquires 10.8% stake in Suntec Reit for S$541 millionIt says the move aligns with its &lsquo positive outlook and conviction in Singapore&rsquo s prime commercial property market&rsquo[SINGAPORE] Property developer Hongkong Land : H78 -2.66% has acquired a 10.8 per cent stake in Suntec Real Estate Investment Trust : T82U +2.05% (Reit) for S$541 million in its drive to grow its presence in Singapore&rsquo s prime commercial sector. In a statement on Thursday (Mar 19), Hongkong Land said the acquisition will enable the group to deploy recently recycled capital into prime, income-producing commercial assets in the city-state. &ldquo This aligns with the company&rsquo s positive outlook and conviction in Singapore&rsquo s prime commercial property market,&rdquo it said. &ldquo The yield derived from the company&rsquo s stake in Suntec Reit will contribute to the diversification of Hongkong Land&rsquo s earnings profile.&rdquo |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

JurongW

Elite |

13-Mar-2026 16:51

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

As at 4.50pm, Hongkong Land is up by 28 cents, top gainers among the STI constituents. Prospects looks good with their Strategic Vision 2035! |

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

13-Mar-2026 14:49

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

Hope the 4 CEs can deliver a performance as good as Black Pink  Alvin, Graeme, Pei Teng and Stuart are proven leaders in commercial real estate. They bring the experience and judgement needed to further drive our performance across each of our core portfolios. By putting decision-making closer to our assets and our customers, we will be better positioned to deliver long-term value across all our core markets.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

13-Mar-2026 13:49

|

||||

|

x 0

x 0 Alert Admin |

Hongkong Land appoints four portfolio Chief Executives to accelerate Strategic Vision 2035 On March 12, Hongkong Land announced the appointment of four Portfolio Chief Executives and the establishment of a revised Management Committee. These changes took effect March 1 and are part a new portfolio-led operating model designed to drive growth across the group&rsquo s core markets. The updated operating model follows a year into Hongkong Land&rsquo s Strategic Vision 2035 which was announced in Oct 29, 2024. The group has achieved 90% of its 2027 capital recycling target, as well as launching the Singapore Central Private Real Estate Fund (SCPREF). Each Portfolio Chief Executive will have direct responsibility for the strategic direction and performance of their portfolio. They will report directly to Group Chief Executive Michael Smith. Alvin Kong, Chief Executive, China Integrated Properties, will lead the strategic direction and performance of Hongkong Land&rsquo s Mainland China-based assets, excluding Westbund Central. Graeme Torre, Chief Executive, Hong Kong Central, will be responsible for strengthening Hong Kong Central&rsquo s position as the leading ultra-premium integrated commercial portfolio in the market. Foo Pei Teng, Chief Executive, SCPREF will manage and grow Hongkong Land&rsquo s ultra-premium integrated commercial portfolio in Singapore through SCPREF, which is Singapore&rsquo s largest office-focused private real estate fund. Stuart Grant, Chief Executive, Westbund Central, will lead the development and performance of Westbund Central, a mega integrated development project in Shanghai. Smith says: &ldquo These appointments are an important step in our next chapter. Alvin, Graeme, Pei Teng and Stuart are proven leaders in commercial real estate. They bring the experience and judgement needed to further drive our performance across each of our core portfolios. By putting decision-making closer to our assets and our customers, we will be better positioned to deliver long-term value across all our core markets.&rdquo |

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

09-Mar-2026 18:12

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

CE bought 356,900 shares at $8.15 on 6 Mar 26. https://links.sgx.com/1.0.0/corporate-announcements/GSD6PJXBQXFRY0NV/877814_HKLH0306.pdf |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

JurongW

Elite |

07-Mar-2026 19:25

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

DBS Research - A Pleasant Dividend Surprise FY25 underlying profit from prime properties investment fell 8% y/y to USD458m, broadly in line with our estimate.

Final DPS rose 12% y/y to USD0.19, ahead of our estimate. c.90% of the 2027 capital recycling target has been achieved. Ongoing share buybacks provide additional support. Maintain BUY with USD10.17 TP Lower contributions from rental and build-to-sell businesses. Hongkong Land reported FY25 underlying profit of USD461m (+12% y/y), which included property provisions of USD371m and net gains of USD247m on reclassification of properties for sale to investment properties and fixed assets. Excluding these non-cash items, underlying profit would have declined 19% y/y, reflecting weaker contributions from both rental and build-to-sell segments. Stripping out earnings from the build-to-sell business, underlying profit from prime properties investment fell 8% y/y to USD458m. Despite softer earnings, final DPS increased 12% y/y to USD0.19, bringing full-year DPS to USD0.25. Improving office vacancy. Attributable gross rental receipts declined 2% y/y, primarily due to reduced contributions from the Central portfolio. On a committed basis, vacancy in the Central office portfolio improved to 6.0% as of Dec-25, down from 6.9% in Jun-25, supported by strengthening leasing demand amid solid equity market performance and a robust IPO pipeline. This compares favourably with the broader Central office market vacancy of 11% as of Dec-25, according to Jones Lang LaSalle. However, negative rental reversions continued to flow through the Central portfolio, resulting in average office rents declining 7% y/y to HKD94 psf. With spot rents in Central showing signs of stabilisation, rental reversions are expected to turn less negative over the coming year. Growing retail rents. The transformation of the LANDMARK retail portfolio remains ongoing, with more than 30% of retail space under renovation in 2025. This led to retail rental contributions declining 8% y/y in FY25. While overall tenant sales declined 5%, top-tier customers increased spending by 8% in 2025. Rental reversions remained positive, supported by tenant mix upgrades. Together with a number of new long-term leases commencing during the year, average retail rents increased 12% y/y to HKD236 psf. Singapore portfolio remains a bright spot. The Singapore office portfolio continues to perform strongly, supported by tight supply conditions and ongoing flight-to-quality demand. On a committed basis, vacancy stood at 2.7% as of Dec-25. Average rents rose to SGD11.5 psf, up from SGD11.1 psf in 2024, supported by positive rental reversions. On the other hand, investment properties in Mainland China and Macau recorded weaker contributions, mainly due to pre-opening costs for pipeline projects in China and lower rents in Macau arising from ongoing renovations and planned tenant movements. Meanwhile, Ph 2 of Westbund Central in Shanghai was completed during the year. The office component (78,000 sqm) has been fully committed, with anchor tenants including Adidas and Lululemon. The retail component is scheduled to open in mid-2026, with pre-leasing exceeding 75%. Sharply lower profits from build-to-sell segment. Hongkong Land has been winding down its build-to-sell portfolio, realising some USD800m from inventory sales, mainly in Mainland China. However, segment contributions declined 44% y/y to USD127m, excluding property provisions. Strong financial position supports acquisitions. As of Dec-25, Hongkong Land reported total borrowings of USD6.14bn (Jun-25: USD6.03bn), with an average debt tenor of 5.8 years. 59% of total debt was fixed-rate (Jun-25: 70%) Weighted average borrowing costs improved slightly to 3.3% in Dec-25, from 3.6% in Dec-24. Following the divestment of MCL Land and partial disposal of MBFC Tower 3, net debt declined to USD3.58bn, from USD4.92bn in Jun-25, despite ongoing share buyback activities. This translated into a comfortable gearing ratio of 12% (Jun-25: 17%). With capital recycled from the establishment of the Singapore Central Private Real Estate Fund, Hongkong Land&rsquo s financial flexibility should strengthen further, enabling the company to raise dividends and pursue prime investment opportunities. Ongoing share repurchase. Since 2024, Hongkong Land has recycled a total of USD3.6bn, achieving c.90% of its USD4bn capital recycling target by 2027. The share buyback programme was upsized from USD350m to USD650m, representing approximately 20% of recycled capital. Since its launch in Apr-25, the company has repurchased over USD340m worth of shares, reducing the number of outstanding shares by c.2.5%. BUY with TP of USD10.17. Over the past three months, Hongkong Land&rsquo s share price has appreciated by 22%. The stock is trading at a 30% discount to our appraised current NAV. We believe the Central office market is bottoming out, supported by improving leasing demand amid stronger capital market activity. In addition, ongoing share buybacks and continued asset recycling should provide near-term share price support, while the development of a fund management platform could justify a higher long-term valuation. By applying a 15% target discount to our Dec-26 NAV estimate, we derive a target price of USD10.17, and maintain our BUY rating. |

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

07-Mar-2026 11:24

|

||||

|

x 0

x 0 Alert Admin |

From war chest to growth: Hongkong Land eyes new investments after US$3.6 billion capital recycling

The group is &lsquo very positive&rsquo on the Singapore market, and looks to expand its presence through the new private fund or development opportunities

[SINGAPORE] Hongkong Land is preparing to ramp up new investments after recycling US$3.6 billion of capital as the property group moves to boost earnings and shareholder returns.

Speaking to The Business Times, Hongkong Land chief financial officer Craig Beattie said that having recycled 90 per cent of its US$4 billion target and cut net debt by 30 per cent, the group now has ample balance-sheet headroom for new investments.

In September last year, it sold its Singapore and Malaysian property arm MCL Land for S$738.7 million in cash. Most of the proceeds went to building a &ldquo war chest for future endeavours&rdquo , such as growing its ultra-premium integrated commercial projects in Hong Kong, Shanghai, Singapore and other Asian gateway cities.

The group expects to see another US$1.5 billion from winding down the remainder of its build-to-sell business over the next three to four years, said Beattie.

Hongkong Land is &ldquo very positive&rdquo on Singapore, and is looking to expand through its private fund or by pursuing development opportunities. &ldquo The fund is quite clearly focused on prime central business district (assets) in Singapore, so anything within that broader area, we are positive about because of the supply and demand dynamics,&rdquo he said.

Among office assets reportedly on the market is Khazanah Nasional and Temasek&rsquo s Marina One, which is said to be asking between S$5 billion and S$6 billion.

Beattie acknowledged that any prime asset in the Marina Bay area would naturally undergo due diligence. &ldquo We&rsquo ll just need to see how things play out,&rdquo he said.

Other markets Hongkong Land hopes to expand into include Seoul, Tokyo and Sydney.

The group is working on &ldquo some early stage opportunities&rdquo , and &ldquo hopefully we can make some positive announcements later this year&rdquo , he added.

Hongkong Land launches S$8.2 billion private fund with portfolio including Asia Square Tower 1 and One Raffles Link

An internal restructuring, announced last week, will focus strategy on four core portfolios: the Singapore fund, Hong Kong Central, West Bund in Shanghai, and assets in mainland China.

Each portfolio now has its own chief executive, Beattie said, and some could be structured into funds. These include a private or listed fund in China as assets stabilise.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

06-Mar-2026 10:34

|

||||

|

x 0

x 0 Alert Admin |

Hongkong Land&rsquo s underlying profit down 8% at US$458 million for FY2025

Earnings per share stood at US$0.5785 from a loss per share of US$0.6276 in the year before

[SINGAPORE] Property developer Hongkong Land : H78 +2.52% on Thursday (Mar 5) posted an underlying profit of US$458 million for the financial year ended Dec 31, down 8 per cent from US$499 million in the previous financial year.

The lower underlying profit was primarily due to decreased contributions from the Hong Kong Central portfolio, said the company on Thursday.

It noted that rental reversions for Hong Kong offices were negative in 2025, although leasing sentiment steadily improved as capital market activity picked up.

Contributions for the group&rsquo s Landmark retail portfolio, Hongkong Land&rsquo s flagship retail space, declined 8 per cent from the year prior on lower customer spending, though the ultra-high-net-worth segment logged an 8 per cent year-on-year increase in customer spending, reflecting the continued appeal of Landmark as a premier luxury destination, the group said.

Performance for the Singapore office portfolio was supported by tight supply and sustained flight-to-quality demand in the central business district. Average rents in 2025 rose to S$11.50 per square foot (psf) from S$11.10 psf in 2024, amid positive rental reversions.

The company highlighted a shift in its economic interest in its Singapore portfolio in February 2026, with the launch of Singapore&rsquo s largest commercial real estate private fund, the S$8.2 billion Singapore Central Private Real Estate Fund (SCPREF).

The fund&rsquo s establishment marked a shift in the group&rsquo s strategy towards fund management. In October 2024, Hongkong Land said that it would exit the build-to-sell residential development business and move towards fund management, with a focus on ultra-premium integrated commercial properties in Asian gateway cities.

The mainland China and Macau portfolio logged lower contributions in 2025 due to pre-opening costs incurred for a number of pipeline projects on mainland China, set to launch from 2027 onwards, and lower rents in Macau due to ongoing renovation works and planned tenant movements.

Hongkong Land launches S$8.2 billion private fund with portfolio including Asia Square Tower 1 and One Raffles Link

Net profit stood at US$1.3 billion, reversing from a net loss of US$1.4 billion in FY2024.

Earnings per share stood at US$0.5785, against a loss per share of US$0.6276 in the year before.

The board is proposing a final dividend of US$0.19 a share, payable on May 13, subject to approval at the group&rsquo s upcoming annual general meeting on May 7.

If approved, it would take the full-year dividend to US$0.25, up 9 per cent from US$0.23 in the year before.

Hongkong Land expects positive momentum in Hong Kong and Singapore to continue into 2026, though trading conditions in mainland China are likely to remain challenging.

The group noted that rental reversions for the Hong Kong office portfolio are set to remain negative, although the magnitude of decline is expected to narrow.

In Singapore, it intends to pursue growth through the SCPREF, while managing costs and improving the operating efficiency of its existing portfolio. It is &ldquo actively assessing&rdquo new integrated commercial property projects alongside acquisition opportunities to grow the SCPREF.

The group expects 2026&rsquo s underlying profit to remain &ldquo largely unchanged&rdquo from 2025.

Part of the Jardine Matheson Group, Hongkong Land has a primary listing on the London Stock Exchange and secondary listings in Singapore and Bermuda.

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

05-Mar-2026 22:16

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

HONGKONG LAND HOLDINGS LIMITED 2025 PRELIMINARY ANNOUNCEMENT OF RESULTS Highlights &bull Strong momentum on Strategic Vision 2035 transformation &bull Cumulative capital recycled reached US$3.6 billion, 90% of 2027 target &bull Net debt significantly reduced, primed to capture growth opportunities &bull Total Prime Properties portfolio valuation up 3% net of disposals &bull Adjusted free cash flow remained strong despite lower contributions from Hong Kong &bull Full-year dividend at US¢ 25.0 per share, up 9% 2025 was a landmark year for Hongkong Land. The Group made significant progress on the initial phases of execution of its new strategy, having delivered on a number of portfolios recycling initiatives, evolving our capital allocation framework to focus on creating shareholder value, and establishing its inaugural private real estate fund. Overall trading performance for the year was solid despite underlying profits being impacted by lower contributions from Hong Kong. The Group continues to wind-down its build-to-sell business with lower profits in 2025 and impairment of Chinese mainland inventory amidst challenging market conditions. We expect underlying results to remain largely unchanged in 2026, with future growth to come from improved market sentiment in Hong Kong, a growing Chinese mainland portfolio and the Singapore fund management business. The Group&rsquo s financial position remains strong and is well positioned to take advantage of potential new investment opportunities in selected Asia gateway cities. Michael T. Smith Chief Executive https://links.sgx.com/1.0.0/corporate-announcements/WZ22K55DD7M9AFXC/877593_SGX.pdf |

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

05-Feb-2026 14:01

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

DBS Group Research - Marching ahead Investment Overview Premium landlord in key gateway cities across Asia. In Oct 24, the company unveiled its new corporate strategy, focusing on ultra-premium integrated commercial projects in Asia&rsquo s gateway cities. The company expects to expand IP assets under management (AUM) to USD100bn by 2035. Achieved c.85% of its 2027 capital recycled target of USD4bn. In Feb-26, Hongkong Land launched its private real estate fund, the Singapore Central Private Real Estate Fund (SCPREF) with AUM of SGD8.2bn at inception. Hongkong Land is the General Partner and Manager of the fund, holding > 50% with an intention to maintain at least 30% going forward. Total net proceeds from the establishment of SCPREF, including the disposal of a one-third stake in MBFC Tower 3, amounted to USD1.3bn. Since 2024, the company has recycled a total of USD3.4bn, achieving c.85% of its 2027 USD4bn target. Upsized share buyback to support share price. The company has increased its share buyback programme by USD300m to USD650m, with an extension to Jun-27. This should provide strong support to its share price. BUY with TP of USD10.13. The stock trades at a 25% discount to our appraised current NAV. The ongoing share buyback programme and continued asset recycling help to support its share price, while the formation of a fund management business should justify a higher valuation for the stock over time. Based on a narrower 15% discount to our Dec-26 NAV estimate, we maintain BUY with higher TP of USD10.13. |

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

04-Feb-2026 11:36

|

||||

|

x 0

x 0 Alert Admin |

Hongkong Land launches $8.2 billion private real estate fund in Singapore SINGAPORE - Property developer Hongkong Land has launched a private real estate fund with $8.2 billion of assets under management (AUM) at inception. The Singapore Central Private Real Estate Fund (SCPREF) is the largest office-focused private investment fund in the Republic and among the largest Asia-focused funds by AUM in the market, according to the company on Feb 3. The fund will focus primarily on managing prime commercial assets and acquire additional high-quality, income-producing commercial assets in Singapore&rsquo s Central Business District and Orchard Road precinct. SCPREF&rsquo s initial portfolio comprises Asia Square Tower 1 (100 per cent interest), Marina Bay Financial Centre (MBFC) Tower 1 and Tower 2 and Marina Bay Link Mall (33.3 per cent interest), One Raffles Quay (33.3 per cent interest) and One Raffles Link (100 per cent interest). The fund is part of Hongkong Land&rsquo s strategy announced in October 2024 to recycle capital from its prime real estate assets, in turn providing a platform to acquire new ultra-premium integrated commercial properties in Singapore. Hongkong Land, holding a majority stake at inception, will act as fund manager, responsible for executing SCPREF&rsquo s investment mandate, and as property manager, overseeing day-to-day operations. Along with Hongkong Land, Qatar Investment Authority and APG Asset Management are also founding investors in the fund. Another investor is a South-east Asia sovereign wealth fund, which Hongkong Land declined to name. |

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

04-Feb-2026 11:35

|

||||

|

x 0

x 0 Alert Admin |

Hongkong Land' s SCPREF is uniquely Singapore, as share buyback programme increases by US$300 million On Dec 12, Hongkong Land announced the formation of the Singapore Central Private Real Estate Fund (SCPREF) with $8.2 billion of assets under management at inception. Hongkong Land will be the general partner and manager of the Fund, and hold a majority stake in SCPREF at inception, as a founding investor along with Qatar Investment Authority (QIA) and APG Asset Management (APG). Other investors in SCPREF include an established Southeast Asia sovereign wealth fund. During a media briefing, Hongkong Land&rsquo s group CEO, Michael Smith points out that his capital partners in SCPREF &ldquo are very focused on having a uniquely Singapore exposure. This vehicle is just Singapore, so we have no intention of expanding this vehicle, and our partners in the fund have no intention to expand.&rdquo The initial portfolio comprises a one-third stake in Marina Bay Financial Tower (MBFC) 1 and 2, 100% of One Raffles Quay (ORQ) and 100% of Asia Square Tower 1. " The investment is anchored by Asia Square Tower 1, which QIA has owned and actively invested in since 2016, and reflects QIA&rsquo s long-standing conviction in Singapore as a leading global gateway city, underpinned by strong occupier demand, transparent regulation and long-term economic resilience, says QIA via a press release. This initial portfolio collectively represents 2.6 million square feet of effective net lettable area (NLA), and had a gross asset value (GAV) of $8.2 billion as at December 2025, making SCPREF the largest private real estate fund focused on Singapore. It is also among the largest Asia-focused funds by AUM, according to Hongkong Land. According to Smithh, MBFC Tower 3 was meant to be included in this fund, and it would have been injected at the same price that was it was acquired by Keppel REIT for. " Given the circumstances of our historic joint venture, we had to make these assets available to our partners, and in the case of Keppel REIT deciding to acquire Tower 3, the price that they paid would have been the same price that we injected into the fund. " We do have validation by APG, for instance, and this unnamed sovereign wealth fund validating that independent valuation by injecting cash into the vehicle,&rdquo says Smith. Post-launch, SCPREF has an investment mandate to acquire additional high-quality, income-producing commercial assets in Singapore&rsquo s Central Business District and Orchard Road District. The assets are likely to be integrated developments with office and retail. SCPREF is an open ended fund, that is, it doesn&rsquo t have a fixed life like so many other private equity funds where assets have to be sold at the end of the fund' s life. &ldquo Because of its open ended nature, when we have other investors who are keen on joining us, we can basically put them in a queue," says Smith. " And when we make future acquisitions, they will make their capital available to us at that point. We have good capital partners with very low cost of capital, and a few different opportunities that we can explore,&rdquo Smith elaborates. According to him, of the $8.2 billion in AUM, 50% is gearing, leaving $4.1 billion of equity, of which Hong Kong Land has just over 50% and the rest is between its capital partners. &ldquo This is a core, open ended vehicle, so it has return targets of 8% over time. That' s total return, not yield. It&rsquo s yield plus growth 8% is a sort of IRR type equivalent by investing in this fund, and it would have the typical liquidity features. " However, we do have, in terms of our initial founding investor bench and the investors that are at the table with us today, they' re all committed to growing and supporting the fund so there will be a lock up, which will enable the vehicle to go all the way to $15 billion,&rdquo Smith adds. &ldquo The reason we mentioned that number is that we have the support of our partners to continue to grow to that size and beyond. We are in a pretty unique position right now where there seems to be assets which haven' t been on the market for many years suddenly coming onto the market.&rdquo When asked about the identity of the Southeast Asian SWF, Smith cites confidentiality agreements. Market observers have wondered whether the SWF could be Khazanah or Temasek, or both, as they own Marina One, which could be the pipeline asset for SCPREF. Hongkong Land has also announced that its share buyback programme will be increased by an additional US$300 million, bringing the total amount allocated to the programme to US$650 million (since 2024), reflecting approximately 20% of the US$3.4 billion capital recycled to date. This extended buyback programme will continue through to June 30 2027 and will be activated after the company&rsquo s 2025 annual results which are scheduled to be released on March 5. The company intends to cancel any shares which are repurchased, reducing the number of outstanding shares issued.. HongKong Land shares closed at US$8.67 on Feb 3, up 4.71% for the day, having doubled in the past year. |

||||

| Useful To Me Not Useful To Me | |||||

|

cmengchan

Senior |

03-Feb-2026 22:07

|

||||

|

x 0

x 0 Alert Admin |

Asked AI and these are the possible ones. However, I think its unlikely from Singapore, otherwise, it could just name it.

Major Southeast Asia Sovereign Wealth Funds:

|

||||

| Useful To Me Not Useful To Me | |||||