| Latest Forum Topics / Sri Trang Agro Last:0.705 -- |

|

|

SRI TRANG GLOVES, A NEW BEGINNING ON 10 MAY 2021

|

|||

|

limjoeseph

Supreme |

24-Aug-2021 20:27

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

24-Aug-2021 10:14

|

||

|

x 0

x 0 Alert Admin |

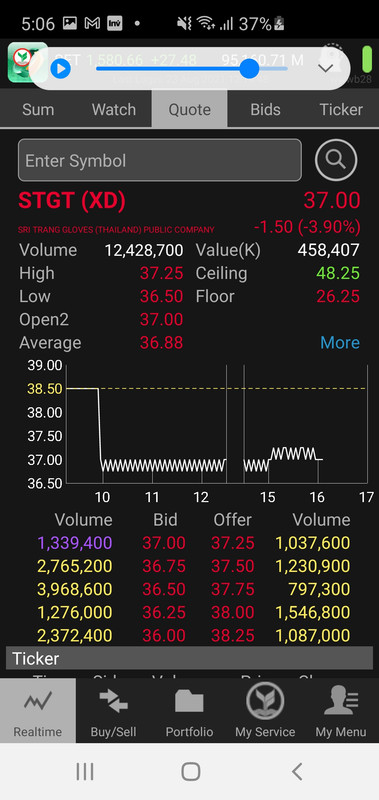

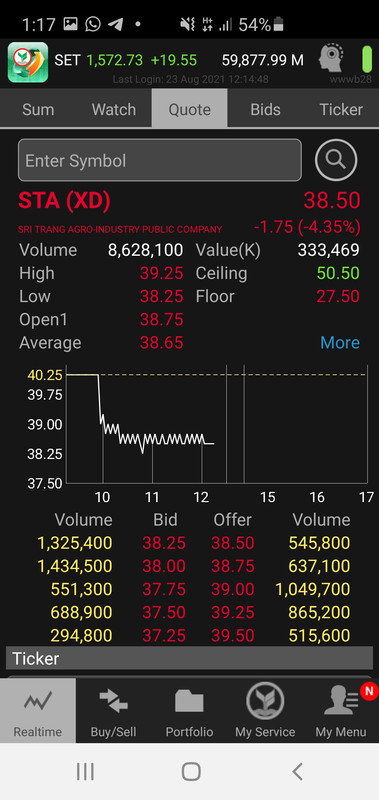

Daily Update on My STA Proprietory Short Term Buying Zone Pivot at 32.46 Bahts ($1.325) and STA closing at 38.50 Bahts ($1.570) on 23rd August 2021 is below Neutral Zone of 39.11 Bahts ($1.595) as STA Thai is the Lead Market but 2nd Quarter Rubber Results including Profits from Associates and Joint Ventures of

US$30 million much Better than 1st Quarter Results of US$10 Milllion. Understand 3rd Quarter Results STA will have a Marked to Market Inventory Gain which cannot be realised in 2nd Quarter Results of US$26.20 Million (839.1 Million Bahts) as per SET's Accounting Practice. Had the Marked to Market Inventory Gain been Realised in 2nd Quarters Profits, STA would have enjoyed higher Rubber Profits inclusive of Profits from Associates and Other Joint Venture Contributions of US$56.20 deriving at a Profits of US$186.20 which only Marginally Lower than 1st Quarter Results of US$191.00. But Overall 2nd Quarters STA Results including Gloves Contribution came in at US$160 Million compared to First Quarter Results of US$191 Million (5959 Million Bahts) well below my Expectations of US$194.98 Million (6083 Million Bahts) due to Loss of Gloves Production of 900 million Gloves from Shutting Down of 2 Gloves Factories and Freight Issues Resulting in Delayed Shipment of Gloves beyond shipment month June. STGT 2nd Quarters Profits of US$231 Million (7.28 Billion Bahts) well below 1st Quarter Results of US$322 Million (10,051 Million Bahts) Below my Expectations of US$290 Million (8845 Million Bahts) and Below Market Expectations of Some Analysts. On 23rd August 2021, STA's NVDR Foreign Institutions Showing 3.85 Million+ Shares Net Sellers whilst STGT Showing Million 0.14 Shares Net Buyers. For the Month of January 2021 to date STA NVDR Foreign Institutions showing 39.12 Million+ Shares Net Sellers (Shortist's Included 209.44 Million+) and STGT NVDR showing 20.49 Million+ Shares Net Buyers (Shortists Included 105.23 Million+). NVDR STA Foreign Institutions/Local Individuals were Sellers whilst Local Institutions/Proprietory Trade were Buyers (SHORTISTS Included). Short Term to Intermediate Term (Less Volatility): Corrective Downside Possibly Over with Potential Rebounce if STA Price Action can close 2 consecutive days above 42.50 Bahts. Consolidation Range between 36.25 Bahts ($1.500) and 50.50 Bahts ($2.095). Please Note that STA's Price Action can only Reclaim its Short Term/Intermediate UPTREND provided STA can close above 50.50 bahts on 2 consecutive days. Medium (Less Volatility) to Long Term (High Volatility): Underlying Primary Uptrend on Earnings Visibility (Profit Making Company) for the Rest of 2021. Negative Rubber/Gloves News Events or Even Rotation Play Between STA (Selling) and STGT (Buying) can Cause a Correction in the Market at Any Point in Time which Potentially can be Worse than Non Rubber/Gloves News Events like Global Stock Market Drop. Other than that, Profit Taking in a Technically Overbought Market is Healthy to Correct Any Market Excesses but when Market Propels Higher in the Short Term with High Volatility, Correction may Potentially be Deeper than We may Think in the Event of Unsuspecting Servere Driven Negative News. Into every Short Term/Intermediate Term New High, STA may Attract Profit Taking but we must be Realistic that any STA's Price Rise is Never Linear and will be Subjected to Drawdown at Any Point in Time Along Its Upside Short/Intermediate Term Trend. As Always, Due Diligence is Warranted on Judgemental Call to Suit Own Risk Appetite. NB: As Much as I can Tell, Short/Intermediate Term Technicals ABC Pattern is trying to Form its (C) Low but Nobody Knows where is the Technical Low. Whether 36.25 Bahts is the (C) Low of ABC Pattern has yet to be confirmed. I Must Admit that the Further Price Drop in STA from the 42.00 bahts Support Mentioned recently has been Exercerbated by the Drop in Shanghai Rubber Futures Price to Test the Fibonacci 61.80% thereabout at 36.50 Bahts which STA tested a low of 36.25 Bahts on 13th July. STA's price drop to date to Recent Low is also partly being Influenced by the Recent Corrective Fall in Copper Prices as Evident by China's Releasing Copper into the Market by China State Reserve Coupled with Falling Latex Demand Due to M'sian MCO Affecting Gloves Counters As Gloves Production Being Affected Dampening Rubber Sentiment but Recently Rubber Futures Prices have Rebounded from its Recent Low Price Low being Undepinned by Physical Tyre Grade Rubber Demand which has been Quite Strong to Date Resulting in Decent Margin for STA's Rubber Division which is Expected to Continue for this 3rd Quarter July to September Rubber Sales Period. According to Elliott Wave Theory the Wave 4 is Clearly Corrective. Prices may Meander Sideways for an Extended Period which is often Frustrating because of Lack of Progress in the Larger Trend. As per Elliott Wave Theorist's Rule of Thumb, if any Wave Labelling has been Violated, the Chart's Techincian has to Relabel the Price Action to Reflect Realistic Market Direction (Please Note that Elliott Wave Reading is Not Engraved in Stone) as in Any Medium to Long Term Share Counter Outlook, Earnings will Still Hold the Key to STA's Market Direction. Yesterday was Ex- Dividend Day and yet STA's Price dropped more than 1.25 Dividend Payout hitting a low of 38.00 Bahts before Closing Slightly Firmer at 38.50 bahts At Present Juncture of STGT 37.25 Bahts and STA at 38.50 Bahts Closing, STA's Intrinsic Value is 39.14 Bahts which now STA's Price Action is at a Discount even though STA's EPS of 3.28 Much Higer than STGT's EPS of 2.50. STGT 38.25 Bahts × 2.872 Billion Issued Shares x 0.562% (STGT Earnings Contribution to STA) ÷ 1.536 Billion Issued Shares of STA to Derive at Intrinsic Value of STA at 39.14 Bahts. On Top of STA's Intrinsic Value of 39.14 Bahts, STA Midstream Natural Rubber Assets including 30+ Factories/Plantations/Land are being Valued at "ZERO". I do not View STA's 2nd Released Result that Bad to Warrant Me to Make the Necessary Adjustment to My STA's Portfolio Presently After having Analysed STA's Financial Results Thoroughly. The Mere Mention of HEMP's Project Materialising by Year End 2021 by Few Thai Analysts Could have Fuelled this Slight Rebounce After Checking With STA's Investor's Department Who Confirmed the Project is Moving Along Fine but Yet Much Leg Work Needs to be Done as Mr Market is Normally Forward Looking. Could the Mention of the HEMP's Project by Management be the Catalyst for STA to Stage the Slight Rebounce Few Days Ago When Foreign NVDR Buyers bought 11.58 Million Shares on 11th August which I Shall Leave to Market Participants to Make Their Own Decision Whether This Rebounce Can be Sustained Leading to a Recovery in STA's Short Term Price Action which had Yet to Be Determined by Mr Market. Besides, STA's Price has already Reacted Downwards to the 36.25 Bahts Level before Rebouncing but Its Results is not as Bad as most Analysts may have thought as yet STA 2nd Quarter Result is still Above One or Two Market Analysts' Expectations. Only a US$31 Million down for 2nd Quarters Results compared to 1st Quarter Results but yet a Money Making company with Decent Dividend Payout to Date. From My Priveleged Thai Informant, a Fair Value for STA's Rubber Assets of Minimum 5 Bahts on Top of Its Intrinsic Value, has been Ascribed to STA's Rubber Division. Yet, as a Medium to Long Term Investor, I am the least not Perturbed by any STA's Short Term/Intermediate Term Whipsawing Price Action as I am Invested in a Fundamentally Sound Growth Stock with Potential Decent Dividend Payout for the 3rd Quarter Reporting as STGT specifically Expounded in their 2nd Quarter Results Report that Dividend will be paid out as well by STGT and I believe so as STA will enjoy likewise as it earns 56.2% contributions from STGT. I still view STA will Enjoy Decent Profits and not a Loss Making Company for 3rd Quarter Results Reporting. Idealistically, let's hope all STA's Iron Hand Medium to Long Term Investors Remain Steadfast to their 2 Cs (Conviction and Confidence) on the Improved Earnings Results of STGT on Resumption of their 2 Factories Operations Hit By Covid Spread Shutdown Recently and One Factory's Expansion Coupled with another New Factory Fully Operational by 3rd Quarter and Another One in 4th Quarter to add Extra Gloves Capacity Moving Forward. As Always, Due Diligence is Warranted to Suit Risk Appetite on Own Judgemental Call as Own Money, Own Target. |

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

limjoeseph

Supreme |

24-Aug-2021 08:35

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

24-Aug-2021 08:31

|

||

|

x 0

x 0 Alert Admin |

Stock futures edged higher in Asian trading following a broad-based rally on news that U.S. regulators granted full approval for Pfizer-BioNTech?s Covid vaccine.

Futures on the Dow Jones Industrial Average rose 73 points. S&P 500 futures and Nasdaq 100 futures both rose 8 points and 25 points respectively. The market started the week on a high note as shares sensitive to an economic recovery jumped on optimism that the vaccine approval would clear path for more mandates in the face of the spread of the delta variant. ?Considering the recent spike in cases and some of the disappointing economic data, this is another step in the right direction, and it helps give confidence to those who might still be holding out on getting the vaccine,? said Ryan Detrick, chief market strategist at LPL Financial. The S&P 500 closed Monday?s session 0.8% higher after touching an intraday record high. The tech-heavy Nasdaq Composite rose about 1.5% to hit a record closing high. The Dow Jones Industrial Average gained more than 200 points on Monday. Investor are eyeing the Jackson Hole symposium later this week, which is expected to be a market-moving event where central bankers could detail their plans for tapering monetary stimulus. The Federal Reserve has started discussions to pull back its $120 billion a month bond-buying program by the end of this year. The summit takes place virtually on Thursday and Fed Chairman Jerome Powell will give a speech on Friday. ?The Fed may make a taper announcement in September or November, but it will probably be a slow taper with no commitment over interest rate hikes.? said Edward Moya, senior market analyst at Oanda. The second-quarter earnings season is winding down with more than 90% S&P 500 companies having reported results. S&P 500 is poised to grow its earnings by 94.7% year over year, according to Refinitiv. |

||

| Useful To Me Not Useful To Me | |||

|

yerongtian

Member |

24-Aug-2021 01:12

|

||

|

x 0

x 0 Alert Admin |

又 有 多 一 个 泰 国 🧤 , 果 然 有 tony这 个 人 物 存 在 否 则 那 个 123真 的 胡 说 八 道 |

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

limjoeseph

Supreme |

23-Aug-2021 21:18

|

||

|

x 0

x 0 Alert Admin |

A GOOD RESD ON THE US STOCK MARKET BY A 3RD PARTY ANALYST:

"The markets finished higher on Friday, but lower for the week. Stocks have been on a tear recently, helped by a stellar Q2 earnings season, and a better than expected employment report. But as earnings season winds down, and the latest jobs report becomes more distant in the rearview mirror, stocks took a pause. There is no doubt the economy is strong. Even with renewed concerns over increasing virus cases threatening to slow the reopening. One look at the jobs picture shows that. And with more jobs available than there are unemployed people to fill them, it looks like the robust pace of hiring will continue for quite some time. But while economic growth is all around, some numbers have slipped a bit. Still growing, but maybe not quite as fast as had been expected. Some of this was brought on by supply chain disruptions and worker shortages. But with the enhanced unemployment benefits, which incentivized some workers to stay at home, expiring in September, we should soon see millions of new workers joining the workforce in the months ahead, and that should begin to bring relief to both of the aforementioned concerns, along with some inflation relief as well. We should also soon get some insight on the fate of the $1.2 trillion infrastructure bill, and the $3.5 trillion budget framework, with the House returning to session this week. That could inject another massive dose of spending into the economy. But, of course, that will also likely come with tax proposals as well. So traders will be watching these developments carefully. In the meantime, we have a full slate of economic reports on deck this week starting with today's Chicago Fed National Activity Index, the PMI Composite Flash report, and Existing Home Sales. Tomorrow we'll get the Redbook retail sales report, New Home Sales, and the Richmond Fed Manufacturing Index. On Wednesday its MBA Mortgage Applications, Durable Goods Orders, and the State Street Investors Confidence Index. Thursday we'll get another look at Q2 GDP, Weekly Jobless Claims, Corporate Profits, and the Kansas City Fed Manufacturing Index. And then of Friday, we'll finish up with Personal Income and Outlays, Retail and Wholesale Inventories, and Consumer Sentiment. We'll also hear from Fed Chair Jerome Powell on Friday morning, as he speaks at the Jackson Hole, WY Economic Symposium, which has been moved online. His speech on 'The Economic Outlook' will be closely watched. Should be a busy week. And with stocks trading near their all-time highs, it won't take much to see them break out even higher." As always, due diligence will prevail. NB: Correction from previous SNP 500 high of 4480 may be tested again. Failing which, SNP 500 may fall back 200 to 300 points to test between 4180 to 4280 range. Yet major support lies between 4100 and 4150. All said, SNP 500 is still in a SECULAR BULL market and that any short term drawdown between 5% to 8% drop will not even derial its Primary Uptrend to eventually test Fibonacci 1% extension minimum 4600 and above by year end. |

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

23-Aug-2021 17:07

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

23-Aug-2021 13:19

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

limjoeseph

Supreme |

23-Aug-2021 13:16

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

22-Aug-2021 09:56

|

||

|

x 0

x 0 Alert Admin |

Daily Update on My STA Proprietory Short Term Buying Zone Pivot at 32.48 Bahts ($1.325) and STA closing at 40.25 Bahts ($1.640) on 20th August 2021 is Above Neutral Zone of 39.04 Bahts ($1.593) as STA Thai is the Lead Market but 2nd Quarter Rubber Results including Profits from Associates and Joint Ventures of

US$30 million much Better than 1st Quarter Results of US$10 Milllion. Understand 3rd Quarter Results STA will have a Marked to Market Inventory Gain which cannot be realised in 2nd Quarter Results of US$26.20 Million (839.1 Million Bahts) as per SET's Accounting Practice. Had the Marked to Market Inventory Gain been Realised in 2nd Quarters Profits, STA would have enjoyed higher Rubber Profits inclusive of Profits from Associates and Other Joint Venture Contributions of US$56.20 deriving at a Profits of US$186.20 which only Marginally Lower than 1st Quarter Results of US$191.00. But Overall 2nd Quarters STA Results including Gloves Contribution came in at US$160 Million compared to First Quarter Results of US$191 Million (5959 Million Bahts) well below my Expectations of US$194.98 Million (6083 Million Bahts) due to Loss of Gloves Production of 900 million Gloves from Shutting Down of 2 Gloves Factories and Freight Issues Resulting in Delayed Shipment of Gloves beyond shipment month June. STGT 2nd Quarters Profits of US$231 Million (7.28 Billion Bahts) well below 1st Quarter Results of US$322 Million (10,051 Million Bahts) Below my Expectations of US$290 Million (8845 Million Bahts) and Below Market Expectations of Some Analysts. On 20th August 2021, STA's NVDR Foreign Institutions Showing 0.22 Million+ Shares Net Sellers whilst STGT Showing Million 0.61 Shares Net Sellers. For the Month of January 2021 to date STA NVDR Foreign Institutions showing 35.27 Million+ Shares Net Sellers (Shortist's Included 205.30 Million+) and STGT NVDR showing 20.66 Million+ Shares Net Buyers (Shortists Included 104.65 Million+). NVDR STA Foreign Institutions were Sellers whilst Local Institutions/Proprietory Trade/Local Individuals were Buyers (SHORTISTS Included). Short Term to Intermediate Term (Less Volatility): Corrective Downside Possibly Over with Potential Rebounce if STA Price Action can close 2 consecutive days above 42.50 Bahts. Consolidation Range between 36.25 Bahts ($1.500) and 50.50 Bahts ($2.095). Please Note that STA's Price Action can only Reclaim its Short Term/Intermediate UPTREND provided STA can close above 50.50 bahts on 2 consecutive days. Medium (Less Volatility) to Long Term (High Volatility): Underlying Primary Uptrend on Earnings Visibility (Profit Making Company) for the Rest of 2021. Negative Rubber/Gloves News Events or Even Rotation Play Between STA (Selling) and STGT (Buying) can Cause a Correction in the Market at Any Point in Time which Potentially can be Worse than Non Rubber/Gloves News Events like Global Stock Market Drop. Other than that, Profit Taking in a Technically Overbought Market is Healthy to Correct Any Market Excesses but when Market Propels Higher in the Short Term with High Volatility, Correction may Potentially be Deeper than We may Think in the Event of Unsuspecting Servere Driven Negative News. Into every Short Term/Intermediate Term New High, STA may Attract Profit Taking but we must be Realistic that any STA's Price Rise is Never Linear and will be Subjected to Drawdown at Any Point in Time Along Its Upside Short/Intermediate Term Trend. As Always, Due Diligence is Warranted on Judgemental Call to Suit Own Risk Appetite. NB: As Much as I can Tell, Short/Intermediate Term Technicals ABC Pattern is trying to Form its (C) Low but Nobody Knows where is the Technical Low. Whether 36.25 Bahts is the (C) Low of ABC Pattern has yet to be confirmed. I Must Admit that the Further Price Drop in STA from the 42.00 bahts Support Mentioned recently has been Exercerbated by the Drop in Shanghai Rubber Futures Price to Test the Fibonacci 61.80% thereabout at 36.50 Bahts which STA tested a low of 36.25 Bahts on 13th July. STA's price drop to date to Recent Low is also partly being Influenced by the Recent Corrective Fall in Copper Prices as Evident by China's Releasing Copper into the Market by China State Reserve Coupled with Falling Latex Demand Due to M'sian MCO Affecting Gloves Counters As Gloves Production Being Affected Dampening Rubber Sentiment but Recently Rubber Futures Prices have Rebounded from its Recent Low Price Low being Undepinned by Physical Tyre Grade Rubber Demand which has been Quite Strong to Date Resulting in Decent Margin for STA's Rubber Division which is Expected to Continue for this 3rd Quarter July to September Rubber Sales Period. According to Elliott Wave Theory the Wave 4 is Clearly Corrective. Prices may Meander Sideways for an Extended Period which is often Frustrating because of Lack of Progress in the Larger Trend. As per Elliott Wave Theorist's Rule of Thumb, if any Wave Labelling has been Violated, the Chart's Techincian has to Relabel the Price Action to Reflect Realistic Market Direction (Please Note that Elliott Wave Reading is Not Engraved in Stone) as in Any Medium to Long Term Share Counter Outlook, Earnings will Still Hold the Key to STA's Market Direction. At Present Juncture of STGT 38.50 Bahts and STA at 40.25 Bahts Closing, STA's Intrinsic Value is 40.45 Bahts which now STA is slightly discounted to STGT and yet STA's EPS of 3.28 Much Higer than STGT's EPS of 2.50. STGT 38.50 Bahts × 2.872 Billion Issued Shares x 0.562% (STGT Earnings Contribution to STA) ÷ 1.536 Billion Issued Shares of STA to Derive at Intrinsic Value of STA at 40.45 Bahts. On Top of STA's Intrinsic Value of 40.45 Bahts, STA Midstream Natural Rubber Assets including 30+ Factories/Plantations/Land are being Valued at "ZERO". I do not View STA's 2nd Released Result that Bad to Warrant Me to Make the Necessary Adjustment to My STA's Portfolio Presently After having Analysed STA's Financial Results Thoroughly. The Mere Mention of HEMP's Project Materialising by Year End 2021 by Few Thai Analysts Could have Fuelled this Slight Rebounce After Checking With STA's Investor's Department Who Confirmed the Project is Moving Along Fine but Yet Much Leg Work Needs to be Done as Mr Market is Normally Forward Looking. Could the Mention of the HEMP's Project by Management be the Catalyst for STA to Stage the Slight Rebounce Few Days Ago When Foreign NVDR Buyers bought 11.58 Million Shares on 11th August which I Shall Leave to Market Participants to Make Their Own Decision Whether This Rebounce Can be Sustained Leading to a Recovery in STA's Short Term Price Action which had Yet to Be Determined by Mr Market. Besides, STA's Price has already Reacted Downwards to the 36.25 Bahts Level before Rebouncing but Its Results is not as Bad as most Analysts may have thought as yet STA 2nd Quarter Result is still Above One or Two Market Analysts' Expectations. Only a US$31 Million down for 2nd Quarters Results compared to 1st Quarter Results but yet a Money Making company with Decent Dividend Payout to Date. From My Priveleged Thai Informant, a Fair Value for STA's Rubber Assets of Minimum 5 Bahts on Top of Its Intrinsic Value, has been Ascribed to STA's Rubber Division. Yet, as a Medium to Long Term Investor, I am the least not Perturbed by any STA's Short Term/Intermediate Term Whipsawing Price Action as I am Invested in a Fundamentally Sound Growth Stock with Potential Decent Dividend Payout for the 3rd Quarter Reporting as STGT specifically Expounded in their 2nd Quarter Results Report that Dividend will be paid out as well by STGT and I believe so as STA will enjoy likewise as it earns 56.2% contributions from STGT. I still view STA will Enjoy Decent Profits and not a Loss Making Company for 3rd Quarter Results Reporting. Idealistically, let's hope all STA's Iron Hand Medium to Long Term Investors Remain Steadfast to their 2 Cs (Conviction and Confidence) on the Improved Earnings Results of STGT on Resumption of their 2 Factories Operations Hit By Covid Spread Shutdown Recently and One Factory's Expansion Coupled with another New Factory Fully Operational by 3rd Quarter and Another One in 4th Quarter to add Extra Gloves Capacity Moving Forward. As Always, Due Diligence is Warranted to Suit Risk Appetite on Own Judgemental Call as Own Money, Own Target. |

||

| Useful To Me Not Useful To Me | |||

|

limjoeseph

Supreme |

22-Aug-2021 09:15

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

leroy55

Veteran |

22-Aug-2021 00:16

|

||

|

x 0

x 0 Alert Admin |

Please teach me how to upload. Thanks

|

||

| Useful To Me Not Useful To Me | |||

|

|

|||

|

limjoeseph

Supreme |

21-Aug-2021 23:28

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

16-Jul-2021 22:11

|

||

|

x 0

x 0 Alert Admin |

https://www.globaltimes.cn/page/202107/1228783.shtml Chinese glove makers see rising orders from overseas

By Yin Yeping Published: Jul 15, 2021 08:48 PM

An employee works at a medical glove factory in Luannan county, North China' s Hebei Province. The county, with an annual output of over 4 billion yuan ($619.13 million) worth of medical gloves, has in recent years aimed to build itself into a manufacturing base for this product. Photo: cnsphoto Chinese glove makers are meeting rising demand from the US and Europe, with new order inquiries jumping by 10-20 percent in weeks, amid production disruption caused by a flare-up of epidemic in Malaysia, the world' s largest rubber-glove supplier. In the face of the new orders, major industry players have been working at their full swing to expand production capacity, the Global Times learned. A person with Blue Sail Group, a leading glove maker based in East China' s Shandong Province, told the Global Times on Thursday that it had received rising orders these days, after production was suspended at factories in Malaysia. More than 90 percent of the orders come from developed countries, including the US and some European countries. The orders are in line with the company' s expansion plan, with a new production line with capacity of 20 billion gloves annually to go into operation this month. Another production line with a capacity of 10 billion gloves is under construction in Weifang, Shandong Province. Another industry player, INTCO Medical, is part of the trend, with " conspicuous" growth in global orders from many of its clients starting in July, media reports said. Malaysia recently imposed stricter restrictions on movement, businesses and factories in its capital Kuala Lumpur, as well as neighboring Selangor state, until Friday to fight a spike in new COVID-19 infections, Reuters reported on July 8. " Malaysian glove manufacturers contribute up to 67 percent of the global supply or 320 billion pieces a year out of 480 billion pieces," The Malaysian Reserve, a business news provider, said in a report earlier in July. China contributes about 10 percent while Vietnam accounts for 3 percent of the global glove supply, the report said, citing Supramaniam Shanmugam, president of the Malaysian Rubber Gloves Manufacturers Association. Chinese glove production capacity used to be inadequate, but there have emerged more rubber glove plants since the epidemic outbreak, industry insiders said. There are 5,384 disposable glove-related companies in China at the moment, after 2,779 companies registered last year and 235 others registered from January to Thursday, data from market information online platform Qichacha showed. In addition to the newcomers, like the mask industry, some companies produced and stockpiled gloves during the outbreak and they are still in the process of releasing the stockpiles, meaning capacity is sufficient for now, Chen Hongyan, secretary-general of the Medical Appliances Branch of the China Medical Pharmaceutical Material Association, told the Global Times on Thursday. While the supply chain disruption in Malaysia is driving more orders to China, industry insiders said that the supply chain transformation is increasingly tilting toward China, with or without the outbreak. " Malaysia is mainly producing natural latex gloves, but the clinical and ordinary gloves used in all walks of life are not latex gloves, but nitrile and other synthetic gloves," Chen said. The sources of natural rubber are mostly located in Southeast Asian countries including Malaysia, making China heavily reliant on imports for natural rubber, which saw a jump in prices lately. In order to reduce reliance on natural rubber, Chinese companies have focused their development and production efforts on gloves made of nitrile. This chemical compound is not only less likely to cause allergic reactions and more likely to offer better tensile properties and protection. " The epidemic caused an increase of raw material prices, so we began to develop raw materials independently, and the production line and ingredients of nitrile gloves were independently developed. The yield is adequate," the person with Blue Sail Group said. |

||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

08-Jul-2021 22:32

|

||

|

x 0

x 0 Alert Admin |

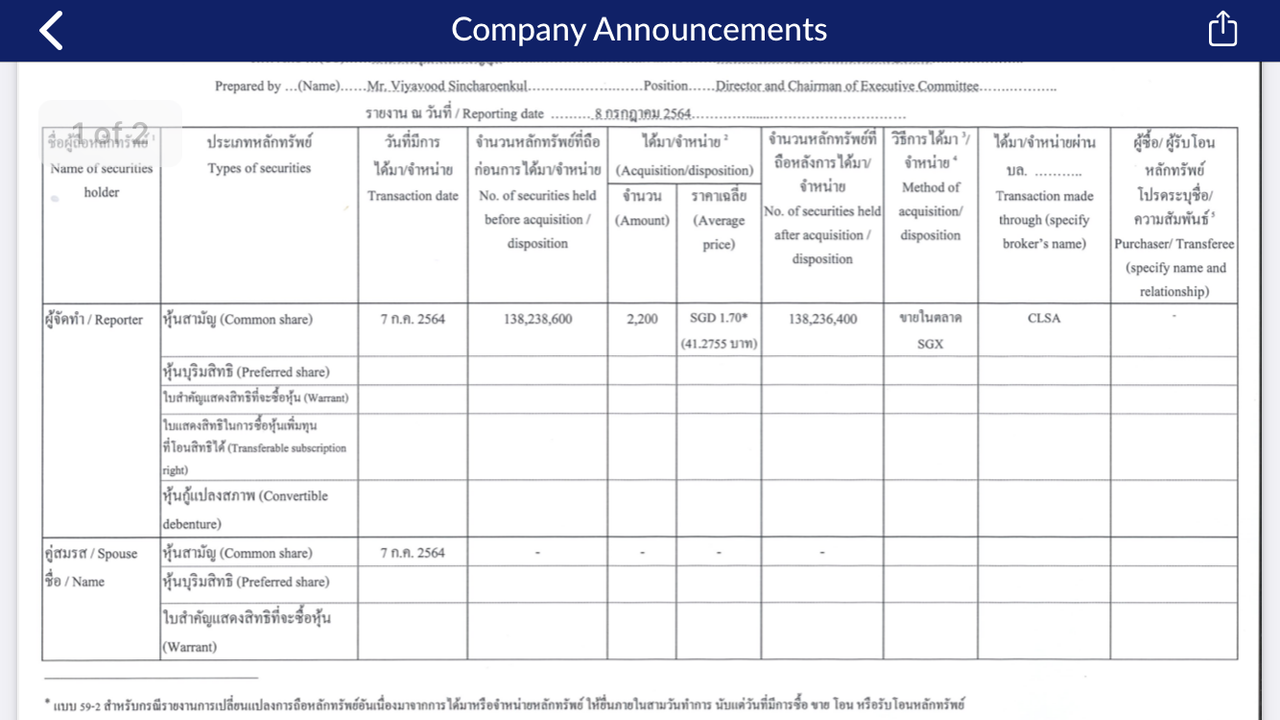

Dr Viyawood sell Shares to create liquidity

|

||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

07-Jul-2021 13:26

|

||

|

x 0

x 0 Alert Admin |

EMCO: Suspension of glove factories' operations affect earnings, overseas interests, says Maybank IBWednesday, 07 Jul 2021 11:45 AM MYT  Maybank IB said that the suspension of the glove factories in Selangor is expected to affect about 55 per cent of Top Glove&rsquo s and 100 per cent of Hartalega and Kossan&rsquo s total production capacity. &mdash Reuters pic KUALA LUMPUR, July 7 &mdash The temporary shutdown of glove factories will not only affect companies&rsquo earnings but could also jeopardise their relationships with overseas buyers, especially when Malaysian glovemakers are facing escalating competition from China&rsquo s glovemakers. In a research note today, Maybank Investment Bank (Maybank IB) noted that Top Glove, Hartalega and Kossan had suspended the operations of their respective glove manufacturing facilities in Selangor yesterday due to the enforcement of the Enhanced movement control order (EMCO). The investment bank said it was taken aback by the latest development as the glove is one of the personal protective equipment (PPE) essential items, and the factories had been allowed to operate during the first MCO. &ldquo Assuming a two-week suspension of glove factories in Selangor under EMCO, we expect our financial year 2021 (FY21) core net profit forecasts for Top Glove and Kossan to decline by 7.4 per cent and 16 per cent, respectively,&rdquo it said. Maybank IB forecasts that Hartalega&rsquo s net profit could drop by 16 per cent in FY22 due to the suspension of operations. It added that the suspension of the glove factories in Selangor is expected to affect about 55 per cent of Top Glove&rsquo s and 100 per cent of Hartalega and Kossan&rsquo s total production capacity. The investment bank noted that while the impact on the glove companies&rsquo earnings is still manageable and temporary, investor&rsquo s sentiment towards the glove counters could be further eroded by the latest development. The sector&rsquo s outlook is currently clouded by ongoing negative news such as declining average selling price (ASP) due to intensifying competition among the new and existing glove players, as well as environmental, social and governance risks. In a separate note, AmInvestment Bank said the shutdown will likely decelerate the slide in the glove&rsquo s ASP, as supply is temporarily capped. &ldquo We believe that the EMCO will be implemented for at least one month, before a return to MCO conditions. &ldquo We do not discount the possibility that these companies will be granted approvals to resume production, given the importance of gloves in managing the spread of Covid-19,&rdquo it added. The investment bank adjusted its fair values of glove companies to incorporate the EMCO and MCO disruptions, slower declines in glove&rsquo s ASP and a sharp drop in post-pandemic glove demand. It had also lowered its price-to-earnings ratios to factor in the factory closure-induced negative investor sentiment. &ldquo We urge investors to look past supernormal profits brought about by the spike in cases due to the Delta variant. &ldquo The variant may result in gentler drops in quarterly earnings, but we doubt it will affect post-pandemic glove demand in a significant way, even if the virus becomes endemic,&rdquo said AmInvestment Bank. It noted that the Delta variant would slow the fall in glove&rsquo s ASP, as glove urgency is buoyed by the rise in cases, and the smaller decline in the ASP would help support earnings of the glove companies in the next 12 months. As at 10.45am, Hartalega rose three sen to RM7.09, Top Glove fell two sen to RM3,92, and Supermax was flat at RM3.14. &mdash Bernama |

||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

06-Jul-2021 23:36

|

||

|

x 0

x 0 Alert Admin |

Tradeview - Retail Investors Are Not Lambs To Slaughter, They Have Families Too For many years, our local stock market had subdued retail investors participation. There are many reason why but mainly it has to do with the past financial crises. Whilst writing my book, I did substantial research sifting through past news reports and academic papers. For every cycle between 1987, 1997/98, 2008/09 and 2020, the stock market rally was always precipitated by influx of retail investors pushing it to new highs. However, they are always the last to leave ending up the biggest loser when the market collapse or selloff. This will then cause a period where retail investors participation dwindles to record low before normalising. This is why brokerage houses or investment bank often focus on institutions / large funds as their key clients. This means they will get good insights from analysts, access to corporate management which help them invest better. Retail investors on the other hand will always be disadvantaged. This caused a vacuum and who fills the void? Fake Gurus Retail investors influx in 2020 reach levels unseen since the 1993 bull run. Similarly, fake gurus started propping up everywhere. Countless Facebook & Youtube Ads of Fake Gurus flooded my social media. No matter how many times I hide or report ads, just like cockroach, they will find a way to come back. Now imagine, with many new retail investors, this makes them easy target for the Fake Gurus. Especially in a time of pandemic, where people are locked up at home, businesses are closed, income reduced, job loss, even boredom kicks in. Many invest in stocks hoping to pass time or simply to make ends meet. When those Fake Gurus keep appearing in your screen, showing you his expensive watch, car, house dressed in suit, you start wondering, maybe you should try investing too. With no knowledge in the stock market, your only reliance is the Fake Guru and his " philosophy" . You dont even know whether what he is teaching you is real because the Fake Guru gets celebrity endorsements and pictures with VIPs. When you ask question, they brush you off. You end up blindly following. Sadly, these bunch of flamboyant and ostentatious people are indeed Fake Gurus who know NOTHING about investments, risk management or valuation. They only know simple theories. Needless to say, tragedy strikes when the market is no longer in a bull run like in 2020. These Fake Gurus had no idea about macroeconomics hence they would not know the intricacies of global landscape, politics or social issues which would necessitate retail investors to conserve cash entering 2021. They would also would not know cashflow importance and missed out Serba Dinamik' s glaring issue. As of today, KLCI is at 1531 which is 9% down from 2020' s peak which is close to a 10% correction. Why am I writing this? After the FM988 live call suicide incident, I felt very empathetic towards the caller' s predicament. What I didn' t know was there are in fact so many victims like him out there who have paid RM 15k per person to these bunch of Fake Gurus and lost almost everything they invested in the stock market. Retail investors are crucial towards the healthy development and vibrancy of Malaysia' s stock market. The fact that their record participation in 2020 have filled the void by foreign funds who have been selling our Malaysia stocks for the past 13 consecutive quarters shows how precious they are. If our retail investors are burnt by your actions and never to return to the market, it would lead to a huge void in future just like the Singapore Penny Stock Scandal in 2013. So, I would like to put this on record, to those Fake Gurus, if you still have conscience and a heart, REFUND every single sen to these poor people. After that, close down your website, social media accounts and do not ever promote yourself as a GURU again. It is not their fault that they are misled by intentional and systemic misrepresentation. They are not lambs for you to slaughter. They have family too. Full article source : www.tradeview.my |

||

| Useful To Me Not Useful To Me | |||

|

Sgvale

Supreme |

06-Jul-2021 10:26

|

||

|

x 0

x 0 Alert Admin |

Program buy-in of Gloves counters after recent big correction | ||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

06-Jul-2021 09:49

|

||

|

x 0

x 0 Alert Admin |

|

||

| Useful To Me Not Useful To Me | |||

|

tonyja

Elite |

04-Jul-2021 15:25

|

||

|

x 0

x 0 Alert Admin |

Maybank says best is over for glove sector as ASP peaks/

July 02, 2021 14:25 pm +08 KUALA LUMPUR (July 2): Maybank Investment Bank Bhd (Maybank IB) said today the best is over for the Malaysian rubber glove manufacturing sector as average selling prices (ASPs) had peaked in the first half of 2021 (1H21) amid moderating demand for gloves on rising Covid-19 vaccination rates. Maybank IB analyst Wong Wei Sum wrote in a note today that the glove sector& rsquo s earnings upcycle seems to have been cut short in anticipation of a faster-than-expected decline in glove ASPs in 2H21. " The glove sector is entering a phase of declining ASP (and hence profit) trend on increased supply and rising vaccination rates. Competition is intensifying among both existing and new entrants. & ldquo ESG (environmental, social, and governance) risk adds further pressure on glove companies& rsquo earnings and valuation outlook. We are switching our valuation method from DCF (discounted cash flow) to PE (price-earnings) multiple, and downgrading the sector to ' neutral' . Hartalega (Holdings Bhd) is our preferred pick,& rdquo she said. Besides Hartalega, Malaysia& rsquo s major rubber glove manufacturers include Top Glove Corp Bhd, Supermax Corp Bhd and Kossan Rubber Industries Bhd. In recent conference calls with analysts, both Hartalega and Top Glove had guided for lower ASPs in the coming months, Wong said today. " Intensifying competition among the existing and new players (especially the rapidly-expanding China glove producers) could further pressure ASP. " According to a Frost & Sulivan report, ASPs for nitrile/latex gloves are expected to decline by -59%/-52% to US$35 /US$20.40 per 1,000 gloves by 2023, from the current US$85/US$42.70 per 1,000 gloves, respectively,& rdquo Wong said. " We downgrade Kossan (shares) to ' hold' while maintaining our ' buy' (call) on Hartalega and ' hold' (call) on Top Glove,& rdquo Wong said. Maybank IB lowered its Hartalega share target price (TP) to RM9.80 from RM13.10 while Kossan& rsquo s TP was revised down to RM3.20 from RM5.25, according to her. On Top Glove, she said Maybank IB lowered its TP for the stock to RM3.98 from RM4.51. According to Wong, Maybank IB lowered its Hartalega TP to RM9.80 from RM13.10 in tandem with an earnings downgrade on the company for the financial year ending March 31, 2022 (FY22), FY23 and FY24. " We lower our FY22/FY23/FY24 earnings forecasts for Hartalega by -21%/-19%/-6% after assuming lower blended ASPs for FY22/FY23/FY24 of US$65/US$44/US$29 per 1,000 gloves, while maintaining our earnings forecasts for Kossan and Top Glove as we have already assumed lower ASPs during last results season,& rdquo she said. Meanwhile, TA Securities Holdings Bhd analyst Tan Kong Jin wrote in a note today that based on the current expansion plans of existing glove manufacturers, entry of new players and aggressive glove production capacity expansion by China, TA Securities believes that there is a possibility of glove oversupply in 2022. " In our forecast, we expect a surplus of 40.3 billion gloves in 2022 (assuming no delays/changes to the targeted expansion plans),& rdquo Tan said. For 2021, he said TA Securities and glove manufacturers, however, project glove supply shortage as the Covid-19 pandemic generates demand for gloves, which is seen as a crucial personal protective equipment. " Based on our channel checks, 2021 capacity will be fully sold. We project a shortage of 27.5 billion gloves while MARGMA (Malaysian Rubber Glove Manufacturers Association) has projected a shortage of 80 billion gloves in 2021. " We expect future demand for gloves to continue growing by 9% over the next three years on the back of: i) rising hygiene awareness, ii) increasing incidence of chronic communicable diseases, iii) ageing population, iv) wider applications across industries and v) growing usage of gloves,& rdquo he said. Tan said that as Covid-19 vaccination continues to gather pace, daily new cases and deaths linked to the pandemic globally are expected to decrease in the future. As such, the lead time for gloves has fallen to about 70 days compared to above 250 days at its peak, he said. Lead time refers to the number of days taken to deliver products to buyers from the day the orders were placed. Hence, Tan said: " We expect (glove) ASP to continue to trend lower and move towards normalisation gradually by end-2023." Overall, glove ASP is still expected to remain above pre-Covid-19 levels due to the increase in cost and structural change in glove usage, according to him. He said the key risk to TA Securities' glove ASP assumptions is a price war initiated by Chinese players to gain market share. " Following the revision in our earnings forecast and rolling forward our valuations to CY23, we downgrade Big 4& rsquo s (Malaysian glove manufacturers) TP accordingly. " We maintain our ' buy' recommendation on Hartalega and Kossan with a lower TP of RM10.50 (previously RM12.16) and RM3.98 (previously RM4.90) [respectively]. " We downgrade Top Glove to ' hold' from ' buy' with a lower TP of RM4.02 (previously RM5.30). Meanwhile, we downgrade Supermax to ' sell' from ' buy' with a lower TP of RM2.76 (previously RM6.07). Downgrade rubber glove sector to ' neutral' from ' overweight' ,& rdquo Tan said. These glove manufacturers& rsquo share prices settled lower during Bursa Malaysia& rsquo s 12:30pm break today. Top Glove fell four sen or 0.98% to RM4.03, Hartalega slipped 12 sen or 1.68% to RM7.02, Supermax slid five sen or 1.51% to RM3.26 while Kossan lost eight sen or 2.51% to RM3.11. |

||

| Useful To Me Not Useful To Me | |||