| Latest Forum Topics / Sri Trang Agro Last:0.705 -- |

|

|

SRI TRANG GLOVES, A NEW BEGINNING ON 10 MAY 2021

|

|

|

tonyja

Elite |

16-Jun-2021 20:25

|

|

x 0

x 0 Alert Admin |

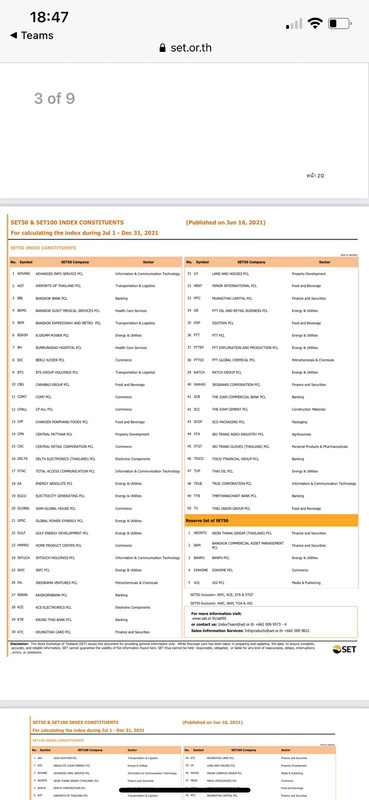

STA STGT is officially SET 50

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

16-Jun-2021 15:49

|

|

x 0

x 0 Alert Admin |

No excessive downward pressure on ASP, says Hartalega KUALA LUMPUR: Hartalega Holdings Bhd

' s product average selling price (ASP) could continue to show improvement quarter-on-quarter although this is expected to taper in 2QFY22, its management has guided. ' s product average selling price (ASP) could continue to show improvement quarter-on-quarter although this is expected to taper in 2QFY22, its management has guided." Due to the over ordering over the past 15 months since the pandemic started, the market is currently undergoing through a phase of inventory adjustment. " However, management expect orders to creep up from Aug 2021 and hence do not expect excessive downwards pricing pressure," said Kenanga Research following a conference call with Hartalega' s management. However, Hartalega' s management guided that ASP is expected to taper 20% in 2QFY22. The ASP trend is expected to soften albeit at a slower pace going forward as lead times have been reduced to 90 to 120 days from 150 days previously. Post-Covid, the inventory restocking cycle is expected to spur demand, coupled with increased usage arising from new users and inreased hygiene awareness, said Kenanga. According to the Malaysian Rubber Glove Manufacturers Association, the demand surge for rubber gloves will last beyond 1Q 2022 with growth rate averaging between 15% and 20% going forward. Kenanga lowered its FY22 net profit projection on Hartalega by 6.5% to account for the lower utilisation rate. It reiterated " outperform" on the counter but downgraded its target price to RM13.80 from RM15.76 previously based on 15x 2022 forecast earnings per share of 92 sen. |

| Useful To Me Not Useful To Me | |

|

|

|

|

tonyja

Elite |

15-Jun-2021 23:26

|

|

x 0

x 0 Alert Admin |

Fear grows that Delta variant will become dominant COVID strain worldwide as WHO says it&rsquo s now in 74 countriesCiara LinnaneLast Updated: June 15, 2021 at 10:54 a.m. ET

Coronavirus UpdateFirst Published: June 15, 2021 at 10:42 a.m. ETBy

AstraZeneca COVID antibody fails in trial, while Novavax says it can safely vaccinate against coronavirus and flu at the same time Listen to Article 6 minutes The Delta variant of COVID-19 has now been detected in 74 countries, prompting fears it will become the dominant strain around the world, as it continues to spread rapidly including in Southern U.S. states that have lagged on vaccination. The highly infectious variant that was first detected in India has been found in countries including China, the U.S. and the U.K., according to the World Health Organization, where it accounted for more than 90% of new cases in the past week. That prompted Prime Minister Boris Johnson to delay the U.K.&rsquo s planned reopening for another four weeks in an announcement at a news briefing on Monday. In the U.S., cases are roughly doubling every two weeks, according to former Food and Drug Administration Commissioner Scott Gottlieb and now account for at least 10% of new cases, he told CBS&rsquo &ldquo Face the Nation&rdquo on Sunday. Advertisement

&ldquo That doesn&rsquo t mean that we&rsquo re going to see a sharp uptick in infections, but it does mean that this is going to take over,&rdquo said Gottlieb. &ldquo And I think the risk is really to the fall that this could spike a new epidemic heading into the fall.&rdquo Concerns about the Delta variant come as California lifts most of its COVID-19 restrictions and ushers in what it is calling the Golden State&rsquo s &ldquo Grand Reopening,&rdquo as the Associated Press reported. Starting Tuesday, there will be no more state rules on social distancing, and no more limits on capacity at restaurants, bars, supermarkets, gyms, stadiums or anywhere else. And masks &mdash one of the most symbolic and fraught symbols of the pandemic &mdash will no longer be mandated for vaccinated people in most settings, though businesses and counties can still require them. The U.S. has now fully vaccinated almost 145 million people, or 43.7% of its overall population, according to a tracker created by the Centers for Disease Control and Prevention. That means those people have received two shots of the two-dose vaccines developed by Pfizer Inc. PFE,-0.29% and German partner BioNTech SE BNTX, -1.68% and Moderna Inc. MRNA, -1.38%, or one shot of the Johnson & Johnson JNJ, -0.27% single-shot vaccine. The AstraZeneca AZN,-0.14% AZN, -0.08% vaccine has not been authorized for use in the U.S. Among Americans 18 years and older, 54.4% are fully vaccinated and 64.5% have received at least one dose. Among those 65 years-and -older, about 42 million people are fully vaccinated, equal to 76% of that group. More than 47 million people in that age bracket have received a first jab, covering 86.8% of that population. But as the map below illustrates, vaccination rates vary widely from state to state, and Southern states, including Louisiana, Alabama and Mississippi showing the lowest rates. Advertisement

Only Maine, Vermont, Massachusetts, Connecticut and Rhode Island have managed to fully inoculate more than 50% of their populations so far.  Elsewhere, France is opening its vaccination drive to those over 12 years old. In Russia, some regions are again tightening restrictions and Ireland is doubling the quarantine period for unvaccinated or partially vaccinated travelers from mainland Britain to 10 days, according to transport minister Eamon Ryan. There was disappointing news for AstraZeneca, which said a Phase 3 trial to assess the safety and efficacy of a long-acting antibody combination, called AZD7442, for the prevention of symptomatic COVID-19 after exposure didn&rsquo t meet the primary goal, as the Wall Street Journal reported. Advertisement

However, the drug reduced the risk of developing symptomatic Covid-19 by 73% in participants who tested negative in a polymerase chain reaction, or PCR, test at time of dosing, AstraZeneca said. In patients who were PCR negative, AZD7442 reduced the risk of developing symptomatic Covid-19 by 92% compared to a placebo more than seven days after dosing, and by 51% up to seven days after dosing, the company said. Novavax NVAX, -7.94% said a study evaluating co-vaccination against COVID-19 and the flu demonstrated similar efficacy to administering Novavax&rsquo s experimental COVID-19 shot alone. &ldquo Separate healthcare visits to cover both COVID-19 and influenza vaccinations will be burdensome,&rdquo a Novavax executive said in a news release. The news comes a day after Novavax said its coronavirus vaccine had an efficacy rate of 90.4% when it comes to preventing symptomatic infection in roughly 30,000 participants enrolled in the Phase 3 clinical trial in the U.S. Advertisement

See now: Disney World and Disneyland won&rsquo t require fully vaccinated visitors to wear masks anymore Don&rsquo t miss: Is it time for Americans to drop their infatuation with the PCR test? That&rsquo s what this COVID-19 testing expert thinks Latest talliesThe global tally of confirmed cases of COVID-19 climbed above 176.2 million on Tuesday, according to data aggregated by Johns Hopkins University, while deaths climbed above 3.8 million. The U.S. continues to lead the world in total cases at 33.47 million, while deaths total 599,963. India is second in total cases at 29.6 million and third by fatalities at 377,031, although those numbers are expected to be undercounted given a shortage of tests. Brazil has the third-highest caseload at 17.5 million, according to JHU data, and is second in deaths at 488,288. Advertisement

Mexico has fourth-highest death toll at 230,187 and 2.5 million cases. The U.K. has 128,171 fatalities and 4.6 million cases, the highest number of deaths in Europe and fifth-highest in the world. China, where the virus was first discovered late in 2019, has had 103,403 confirmed cases and 4,846 deaths, according to its official numbers, which are widely held to be massively underreported. |

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

14-Jun-2021 22:16

|

|

x 0

x 0 Alert Admin |

Malaysia' s Glove Sector & Medline Industries Inc. Blockbuster US$34 Billion DealTradeviewWednesday, 09 June 2021

The glove sector is a remarkable industry which have captured the imagination of many investors for the past 1.5 years. As we are now approaching the point of resolution of Covid-19, many of the glove stocks share price have retraced significantly from its peak in 2020. In fact, so much so that most glove stocks currently hover around 50-60% lower from its peak level. I have heard all kinds of doom and gloom statements on the glove sector for the past 10 months from its peak all the way down to where it is today. What I find most fascinating is the ever evolving valuation given by research houses throughout the past 1.5 years. As swiftly as the research houses hike the target price of glove stocks, the downgrade came just as quickly. Apart from that, the ever changing rationale used to justify their reports (whether you agree or not, doesn' t matter in this context) is by far the most complete and holistic in comparison to any other sectors ever covered by the research houses. Usually, in reports by research houses, they cover some grounds here and there but largely there is a central theme behind it. For example : for semiconductor stocks, it is about the global chip shortage or 5G / AI adoption rate for the steel sector, it is about the commodity super cycle, for the banking sector, it is usually about the interest rate or overall economic health. However, if we compile all the research houses report for the glove sector in the past 1.5 years, the sheer amount of volume would easily be double that of the next sector and the grounds for justifying an upgrade or a downgrade or revision of TP would be far ranging. Essentially, what it means is that the glove sector is the most widely and deeply scrutinized sector in the whole of Bursa. I believe no one can deny that. The biggest debate or challenge is always how do you value a company and specifically, a glove company? This is because of the extraordinary profits from the sector due to once in a century global pandemic that totally distorted the ordinary course of business. The point I am trying to focus on is no one actually knows how to value the glove sector objectively due to the lack of historical precedent in terms of proportion and impact. This is why from the research houses reports, you can see midway through their analysis they can change valuation method from PER based on historical standard deviation to Discounted Cashflow model. On top of that, the valuation multiple attached also changed especially when there is the rollover to reflect the next or following year. Interestingly, there are some research house using year 2024 to forecast the valuation of glove companies. In all my years investing in the stock market, I have not come across anyone who can accurately look beyond 2-3 years (considering the volatility, uncertainty in global business, political and social landscape today it is even harder). So for investors in glove sector, what is the most important question to ask yourself at this juncture as you start to witness ASP decline reflected in Supermax and Top Glove' s results? I believe it is necessary for investors to grasp the concept of valuation and then look at glove companies from the angle of a valuation standpoint. This is where I have been coming from all this while. When I first decided to invest in glove stocks in 2020 amidst the confusion and frenzy, I was not looking at the short term sentiment but their earnings visibility and exponential cashflow growth. Overnight glove companies became a different animal after toiling for 20-30 years. In the span of 1.5 years, their earning potential exploded and they made more money than they ever did from the past 20-30 years. They are no longer the same type of company as what they once were. Apart from unbelievable retained earnings which is what I mentioned in the earlier article, glove companies which are well managed have shown they are like a " cash printing machine" during times of pandemic or healthcare crisis. They actually showed the world how much money they can make. From the Covid-19 pandemic, glove companies are not the only beneficiaries. Tech companies for instance were big winners. If we were to compare, I believe tech stocks were even a larger beneficiary due to valuation expansion. However, if we look at actual earnings, none can come close to glove companies, not even tech stocks. Hence, when I saw the Private Equity (PE) funds consortium [Blackstone, Carlyle Group, Hellman & Friedman, Government of Singapore Investment Corporation (GIC)] coming together to make anacquisition offer of Medline for close to USD $ 34 billion including debt, it validated what I have believed all this while which is the true intrinsic value of healthcare PPE players are worth a huge premium. Although glove is only one part of PPE and only a segment of Medline, the valuation itself shows how valuable the PE Funds value companies along the healthcare supply chain. It is very simple, the healthcare business especially one like Medline which is US largest privately owned medical supplier / distributor & manufacturer has strong cashflow generation ability, healthy balance sheet and cater to the essential need of mankind. It is not a business that will go out of fashion or face dwindling demands. If anything, the need will grow consistently over time with a growing population and increasing hygiene awareness. If the future of healthcare supply chain companies are bleak or there is an oversupply with falling ASP impacting the earnings (PPE, glove and others), why would these 4 large PE funds make a mega offer for Medline at this juncture and not wait for the earnings to plunge? Wouldn' t they get a better offer later than now? The logic is very simple - These 4 PE funds witness the explosive earning potential of Medline, the importance of the business in this sector and promising future due to the increasing hygiene awareness globally following this global pandemic. They saw earnings visibility and sustainability in the years to come. This Medline M& A deal is the largest Leveraged Buyout (LBO) deal since 2008 financial crisis. Coming back to Malaysia context, when PE funds want to buy over glove companies, do you think the owners will sell the company for the current lousy valuation that a foreign bank and some research houses is giving towards the glove companies today? Do you think Top Glove is worth RM 3.50, Hartalega RM 8, Kossan RM 3.80? It doesn' t make sense right? We must understand, that these research houses and IB are short term in nature, they change their reports based on market sentiment or what funds are doing in a span of 12 months. However, when considering a company' s valuation, it is imperative to take into account of their long term fair value. This is among the market inefficiencies that long term fundamentalist investor can take advantage of to build wealth over time. Hartalega is one of my favourite glove companies. With regards to Medline acquisition, an important point to note is that Medline is Hartalega' s substantial shareholder apart from being their major client (also for other glove companies too). If Hartalega' s substantial shareholder is being valued at a premium, what does that mean for Hartalega? Many have argued that glove companies are just commodity stocks which have their cycle or OEM manufacturer that faces large capex cost hence it is not worth much in terms of valuation. I would not want to waste time and effort dispelling such comments because these are inaccurate descriptions. I would want to just point out that Malaysian glove companies have build themselves up to become entrenched within the global healthcare supply chain which is not easily replaceable, not even by China manufacturers. Recent Intco Medical failure in book building and management disposal of shares as shared by Ben Tan have clearly shown that Maybank' s earlier research on glove sector oversupply was flawed. Maybank gave too much credit to Chinese manufacturers and downplayed the abilities of local glove player which proved to be a simplistic view as it failed to consider exaggeration and promotion by Intco Medical. This is why I am especially confident in Hartalega or Riverstone to some extent Kossan and Comfort. Top Glove problem since last year has been because of CBP Ban. Factors beyond our control, like politics, policies etc are tough to assess. Actually what happened to Top Glove is essentially that. Top Glove is damaged by CBP policy (political or not, I do not want to comment). Otherwise, Top Glove would have performed more sustainably instead of erratically. I believe coming out of this experience with the CBP, Top Glove would become a better corporation in future and as long as they do not give up, eventually they will get their fair dues. As far as I know, the glove companies are severely undervalued and investors should take a leaf from the Medline acquisition to give them comfort that the glove stocks are valuable companies. It is not all doom and gloom. At most, patience is required that' s all. The glove sector is an integral part of medical supply which will only be more crucial in future as the population grows whether as strategic PPE stockpile or essential medical equipment. I shall leave it to your discretion. |

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

14-Jun-2021 21:56

|

|

x 0

x 0 Alert Admin |

Trang operation could be start on Wednesday |

| Useful To Me Not Useful To Me | |

|

|

|

|

tonyja

Elite |

11-Jun-2021 19:44

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

11-Jun-2021 15:34

|

|

x 0

x 0 Alert Admin |

Trang operation will resume next mid week |

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

08-Jun-2021 19:42

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

|

|

|

limjoeseph

Supreme |

07-Jun-2021 11:44

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

07-Jun-2021 11:26

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

06-Jun-2021 22:16

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

06-Jun-2021 20:42

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

|

|

|

limjoeseph

Supreme |

06-Jun-2021 13:39

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

limjoeseph

Supreme |

06-Jun-2021 13:36

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

limjoeseph

Supreme |

06-Jun-2021 13:29

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

05-Jun-2021 23:57

|

|

x 0

x 0 Alert Admin |

Tradeview Commentaries - Cashflow Is The Lifeline Of A Company I have had many opportunities over the years to meet many businessmen. Be it big or small, whenever I ask them what is most important thing when running their business, without hesitation they will tell me - cashflow. Cashflow is the reason why a company can remain a going concern. It is also the reason why a company can sustain, grow and expand. A company with a healthy cashflow is a stable company. Almost every major company that collapsed can be attributed to cashflow problems. Thus, I find it perplexing when some quarters of retail investors choose to ignore or overlook this important metric. Some would focus on solely on rumours yet I seldom hear people saying, &ldquo I invest in this company for the strong consistent cashflow&rdquo . Looking at Serba Dinamik ongoing saga, the vast amount of comments and scrutiny over the past weeks have been drilling into their high debt, high receivables and negative cashflow. I remembered how Serba Dinamik along with KPower SCIB were darlings of the stock market up until their most recent quarterly report. Why didn&rsquo t those research analysts or fund managers who promoted the stock pick this up? Why only on hindsight everything is surfacing? In fact, many readers have repeatedly asked me about these stocks and why did I not invest or write about them. To me there were many red flags but one of the main issue was the cashflow. You can refer to the pictures in order of the dates as proof that what I am saying isn&rsquo t a matter of hindsight. In all honesty, it would be great if Serba Dinamik issue is just one big misunderstanding, that way there will be no domino effect to the banks who loan them money, bond holders, suppliers and most importantly, retail investors. I take no comfort or joy seeing this happening. It serves no one any good. Cashflow specifically operating cashflow is very important to me so much so it forms part of the key metrics in The Money Equation approach which I devised towards stock picking. Retail investors must be cognisant just because a stock has a very low PE ratio or EP ratio doesn&rsquo t make it the most underrated or undervalued stock in Bursa. One must understand there is more to investing than just a singular data point. Coming to a decision must be based upon a coherent set of metrics forming a parameters before a well informed investment decision can be made. Operating cashflow is definitely one of it. Source : www.tradeview.my |

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

05-Jun-2021 21:21

|

|

x 0

x 0 Alert Admin |

China Is Losing Its Power to Rein In Commodity-Price Surges May 28 2021, 10:26 AM (Bloomberg) -- China&rsquo s efforts to rein in surging commodities prices are likely to be in vain as it&rsquo s lost the ability to boss the market around, according to two of Wall Street&rsquo s biggest firms. The speed of the rebound in demand in advanced economies, particularly the U.S., means China is no longer the buyer dictating pricing, Goldman Sachs Group Inc. analysts led by Jeff Currie, the bank&rsquo s global head of commodities research, said in a note. That view was echoed by his equivalent at Citigroup Inc., Ed Morse, who said in a Bloomberg Television interview Friday that despite China&rsquo s efforts to curb price gains, the real supply-demand balance prevails. The largest buyer of many commodities, China has been trying to temper the rally due to fears over inflation. Its actions have had some success, with local iron ore prices down more than 20% since May 12. But other raw materials have been more difficult to manage. The Bloomberg Commodity Spot Index is only down around 1% over the same period. The price dip after warnings from Beijing about speculation is a &ldquo clear buying opportunity,&rdquo as raw materials such as copper and soybeans remain on an upward path on tight supply, Goldman said. What Beijing is doing is similar to what Washington did in the mid-2000&rsquo s, according to Goldman. &ldquo When commentators are unable to understand what is driving such a paradigm shift in prices, they attribute it to speculators - a common pattern throughout history, which has never solved fundamental tightness.&rdquo Freeport-McMoRan Inc., the world&rsquo s biggest publicly traded producer of copper, said scarcity of the metal will trump any cooling efforts. &ldquo In the short-run, actions can have an impact, commodity trading can have an impact,&rdquo Freeport-McMoRan Inc. Chief Executive Officer Richard Adkerson said in a Bloomberg Television interview Thursday. &ldquo But the commodity market for copper today is extraordinarily strong. Both on the demand side, we&rsquo ve got new sources of demand, and supply scarcity is a real factor in the marketplace.&rdquo Bets on tight supplies have pushed up copper prices to records as major economies emerge from the pandemic and the energy transition boosts the outlook for the metal used in electric installations. &ldquo It&rsquo s hard to find another commodity that has the supply side support that copper has,&rdquo Adkerson said. &ldquo And now we&rsquo ve got a new era of copper demand where we&rsquo re not just relying on China&rsquo s growth for new demand but lots of things for growth outside of China.&rdquo There&rsquo s &ldquo mounting evidence that commodities are no longer China-centric,&rdquo Goldman said. The main reason for the U.S.&rsquo s greater power in the market is Washington&rsquo s fiscal stimulus, but there are also structural factors -- China no longer benefits as much from low-cost labor or from its previous indifference to environmental concerns -- that make this a paradigm shift, they said. |

| Useful To Me Not Useful To Me | |

|

limjoeseph

Supreme |

04-Jun-2021 23:06

|

|

x 0

x 0 Alert Admin |

I presume it must come as a big surprise to Readers that even a 3.82 billIon bahts (US$123 Million) total full year net profit for 2010 STA's earnings result with big rally in rubber price after WHO declared Virus Free Global Day in August 2010 and yet with oversupply in global gloves resulting in lower ASP can still send STA to hit previous all time of high 41.20 bahts in Feb 2011.

Therefore with 2020 total full year earnings of 9.51 bln bahts (US$307 million) sending STA to rally to 56.75 bahts in March 2021 all time high without big rally in rubber prices but just on earnings only. What then if with 1st and 2nd quarters combined STA earnings of 12.91 billion bahts (US$416 million) even without rubber rallying? On this score, I shall leave it to readers to make their own judgemental call to STA's market direction after 2nd quarters earnings on 10th August barring any unsuspecting negative news event before or after the results release. As always due diligence is warranted. |

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

04-Jun-2021 22:34

|

|

x 0

x 0 Alert Admin |

|

| Useful To Me Not Useful To Me | |

|

tonyja

Elite |

04-Jun-2021 19:57

|

|

x 0

x 0 Alert Admin |

Top banker warns slow vaccine rollout could &lsquo devastate&rsquo manufacturing") As a series of new Covid-19 clusters prompt factory shutdowns and losses to business and the economy, a top banker has warned the shambolic vaccine rollout could cripple Thailand' s manufacturing industry. &ldquo We need quick vaccination before the coronavirus outbreak devastates our manufacturing sector,&rdquo said Payong Srivanich, chairman of the Thai Bankers&rsquo Association. &ldquo Our economy can&rsquo t take another hit to the industrial sector, with exports being the only key growth driver now.&rdquo From the biggest food conglomerate to the largest rubber producer, new infections among workers have forced companies to temporarily halt production for testing and disinfection. Charoen Pokphand Foods Plc closed one of its plants after hundreds of workers tested positive for the virus, while Sri Trang Gloves Thailand Plc shut two factories that account for about half of its daily production capacity. These factory clusters are spread among several provinces, and have become the latest sources of new infections as the government, private businesses and ordinary citizens struggle to curb Thailand&rsquo s worst virus wave since the pandemic began. Since the resurgence began in early April, infections have spread from Bangkok&rsquo s night-entertainment venues into the capital city&rsquo s crowded communities, prisons and construction-worker camps. With Thailand&rsquo s current pace of vaccine rollout restricted by limited supplies, it could take until at least the end of this year for 70% of the population to be fully inoculated. Some 3.6 million doses of vaccines have been administered, only enough to cover 2.5% of the population. The slow deployment risks leading to more infections, threatening the government&rsquo s plan for economic recovery and tourism reopening. &ldquo If many more factories are forced to be closed with more outbreak, exports will ultimately be affected,&rdquo Mr Payong said, adding that demand for Thai products is rising as economies of many trade partners are recovering. |

| Useful To Me Not Useful To Me | |